The Greatest Risk to Investment Success: Emotional Reactions

In the midst of the recent market volatility related to the global shutdown due...

In the midst of the recent market volatility related to the global shutdown due...

https://russellinvestments.com/-/media/files/us/insights/corporate/q2-2020-global-market-outlook-full-report.pdf?la=en&hash=2F93B39927C5900DAE28BC9D51EA4628215F23CB

https://amgfunds.com/content/dam/amgfunds/LandingPages/KeepCalm/per_keepcalm_per029.pdf

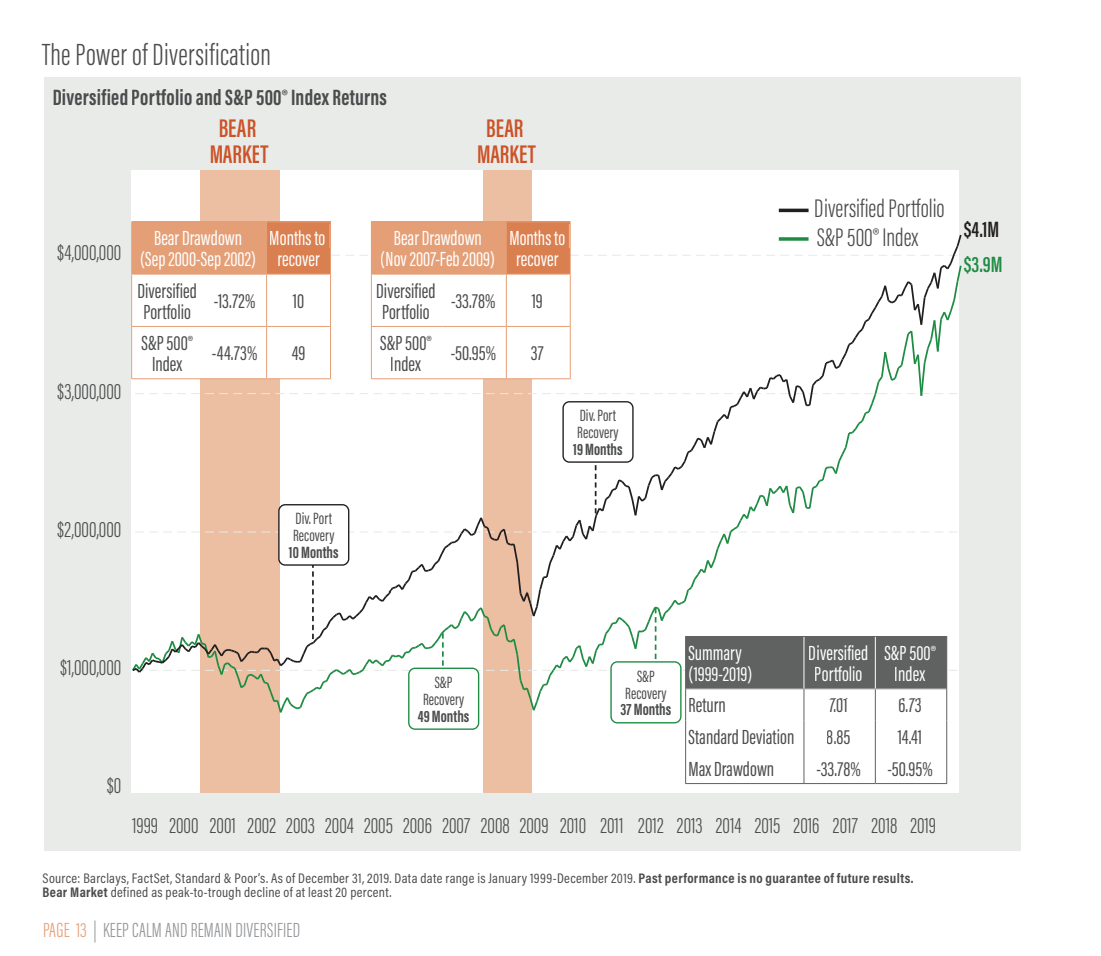

As investors work their way through the latest round of market volatility, this time...