Foreign Stocks: Do They Still Make Sense?

The importance of diversification has been well established across the investment research literature over many decades. It is a relatively easy principle for most investors to accept. The words “don’t keep all of your eggs in one basket” is one of the most common phrases repeated over time.

However, asset allocation is just as important. The concept of asset allocation is based on the notion that not only do you not want to own just a few companies, but you also want to own assets that demonstrate a lower correlation to each other. A lower correlation simply means that multiple assets may increase over time, but at different times, for different reasons, in different environments.

As an example, the use of owning stocks across various market capitalizations, (Large, Mid & Small Cap stocks), and different regions of the world help diversify a portfolio. Additionally, the use of other assets such as fixed income, real estate, and commodities further lower correlations in an investment portfolio.

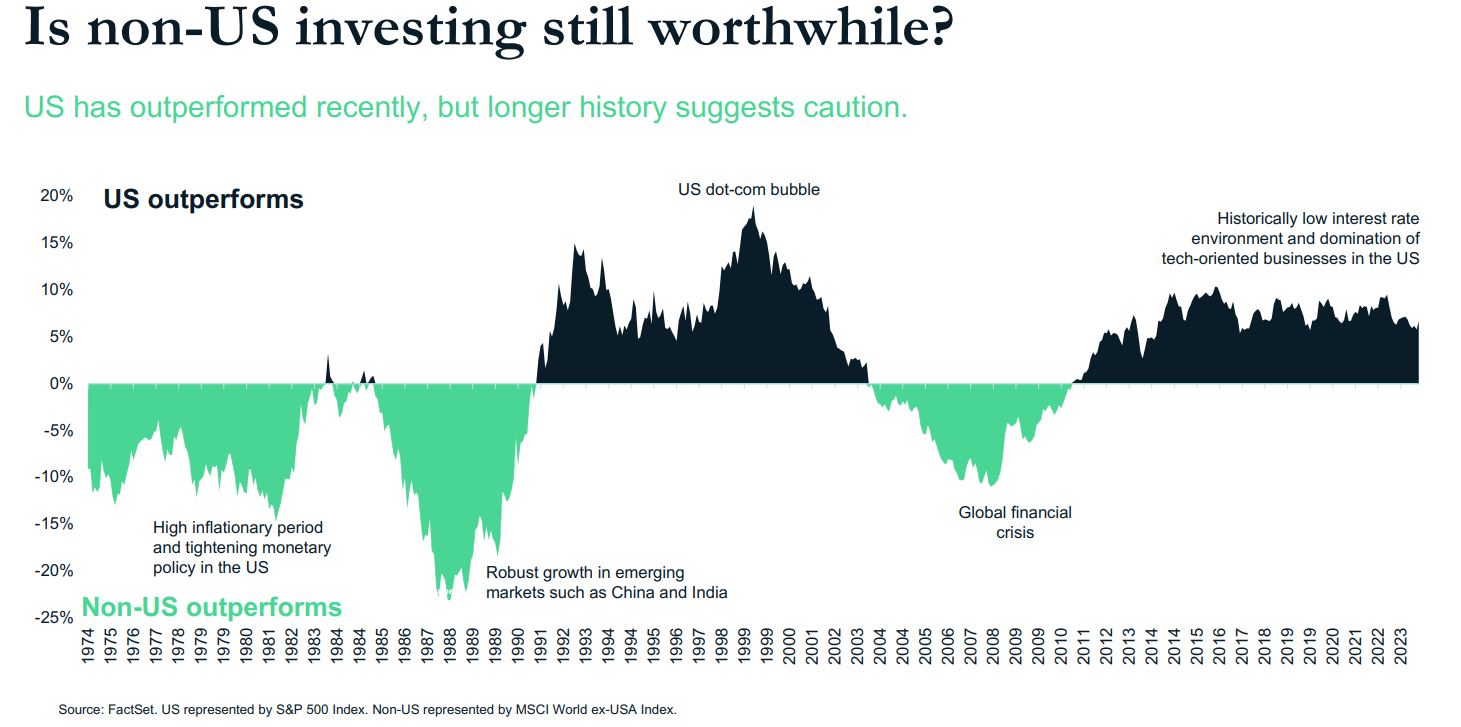

The use of international investments is one of the areas that has recently come under scrutiny as the US stock market, particularly the S&P 500 index has significantly outperformed international stocks for the better part of the last 15 years. However, as the chart above courtesy of Diamond Hill Investments shows, it is not necessarily unusual for US or foreign equities to lead for significant periods of time.

During the seven years from 2004-2011, international stocks had a more favorable performance. During the seventeen years between 1974-1991 international stocks also outperformed. This is often overlooked because during periods like the 1980’s US stocks did exceptionally well. Yet, for most of that period, international stocks did even better.

When looking at recent history, not only do we see that the US has had an extended period of recent outperformance but is also trading at relatively high prices by comparison. As an example, as of January 31st, 2024, the MSCI USA Index was trading at a price to earnings ratio (PE ratio) of 25.4. While the MSCI ACWI ex USA index (which is a foreign stock index) was trading at a PE ratio of 14.9, making it comparatively cheap.

This data suggests that foreign stocks are substantially undervalued and more attractive when compared to the US stock market. Does this mean that foreign stocks will outperform in the near future? Not necessarily, or at least not right away. However, it does make a strong case for owning foreign stocks. History suggests there will be a reversion to the mean, and at some point, foreign stocks will lead the markets again. Timing such a reversal is just as futile as timing markets in general. The more important lesson is that foreign stocks play a role in a portfolio over time.

As a result, we believe there should always be some degree of exposure in foreign stocks as part of an overall asset allocation to aid in the diversification of a sound long-term investment strategy.