Retirement savings options have expanded dramatically over the last four decades. Defined contribution plans such as 401ks have progressively become the primary source of private sector savings since the early 1980s. Unfortunately, for those in a higher income range, annual dollar value caps associated with contributions are imposed. In 2014, the maximum annual salary deferral for an employee is $17,500.00 ($23,000.00 if over age 50). One alternative solution to help mitigate current tax liability is the use of the Non-Qualified Deferred Compensation Plan (NQDC).

An NQDC plan can be established by a small business owner or by a large Fortune 500 company, and falls outside the regulatory scope of the Employee Retirement Income Security Act (ERISA). Under an NQDC plan, contributions made to the plan by an employee are deferred income, which may include salary, bonus and commissions. These contributions can be as much as 50% of an individual’s compensation. In making the salary deferral contribution, the employee reduces his or her adjusted gross income (AGI). This not only lowers taxable wages, but also may reduce an individual’s exposure to the Alternative Minimum Tax (AMT). Reducing AMT exposure may create additional tax benefits such as increasing the availability of itemized deductions like mortgage interest and property taxes.

These plans are typically either account based or non-account based plans. Contributions to account based plans may be met with a company match, and earn a fixed or variable interest rate. Some plans will opt to offer various investment options not unlike a 401k plan. Under a non-account based plan, the benefits function similar to a defined benefit plan…which is similar to a pension plan that provides an annual lifetime income at the commencement of benefits.

In the case of a small business owner, due to the greater flexibility of plan participation resulting from operating outside of ERISA laws, plans can be offered only to key employees. This can greatly reduce the administrative and funding costs, while offering significant tax advantages to the business owner. However, since the plan is not income to the employee, the plan does not become a deduction for the business until benefits commence. Due to the lack of an immediate tax benefit to the employer, many of these plans are unfunded future obligations.

While there can be substantial immediate tax benefits to an employee contributing dollars to a NQDC plan, there are inherent disadvantages. Among those disadvantages would be that the plan is a liability of the corporation and subject to the general creditors of the company. This is in contrast to a qualified plan in which vested plan assets belong exclusively to the employee. As a result of this liability, some employers have purchased insurance to help cover the liabilities of the plan should a company be liquidated. However, this benefit is the same as that of a general creditor and does not guarantee that the insurance will be sufficient to meet the unfunded liability. So when an employee opts to contribute deferred income, they should seriously consider the long term fiscal health of their employer. This becomes difficult for a younger employee who may be affiliated with a prosperous company, but couldn’t possibly forecast the fiscal health of an organization in 20 years with any certainty. It is possible that some or all of your salary deferral saved over many years could be confiscated by creditors of the company.

Some plans are established as funded plans, such as a Rabbi Trust. Under this type of trust, the plan assets are segregated in a separate trust for the purpose of satisfying future plan benefits. Ordinarily, this would make the income taxable to the employee, however, the IRS allows this as a funded NQDC plan, presuming that the trust is subject to substantial risk of forfeiture by including the trust as an asset that can be claimed by the general creditors of the corporation.

Another issue to be concerned with as a possible participant in a NQDC plan is that of the timing of distributions. NQDC plans are not eligible to be rolled into an IRA/401k or any other qualified plan at retirement or separation from service. This lack of portability means more restrictions on benefit distributions. These restrictions have been increased substantially since 2005. These rules were designed to prevent key employees from accelerating benefits and liquidating plan assets in advance of a financial liquidation of a company in fiscal trouble. Any failure to comply with these rules would result in substantial IRS penalties. The rules restrict distributions to several categories. Among them are: separation from service, death, disability, fixed time frame and change in ownership of the company.

It is important as the employee to understand these restrictions. As an example, if the plan was designed to be paid out over a five year period following separation from service, this could become problematic if you just resigned your position in order to accept a better job with a higher salary at a new company. In theory, you may have deferred income for only a few years only to realize it long before retirement while still in a high/higher tax bracket. This would have totally negated the tax benefit. As such, it is important to consider these variables when determining whether or not you wish to participate in or create a NQDC plan. It is best to discuss this with both your financial and tax advisors to ensure proper planning and suitability.

Filed under: Articles

Comments: Comments Off on The Pros And Cons Of Non-qualified Deferred Compensation

In the course of building a long term investment portfolio, the focus should be based on not just returns…but risk-adjusted returns. The premise behind a multi-asset portfolio is combining multiple asset classes in which each produces a positive long-term return, without being highly correlated. This can produce more consistent longer-term returns…while offering a lower overall degree of portfolio volatility. One of these asset classes is the commodities market.

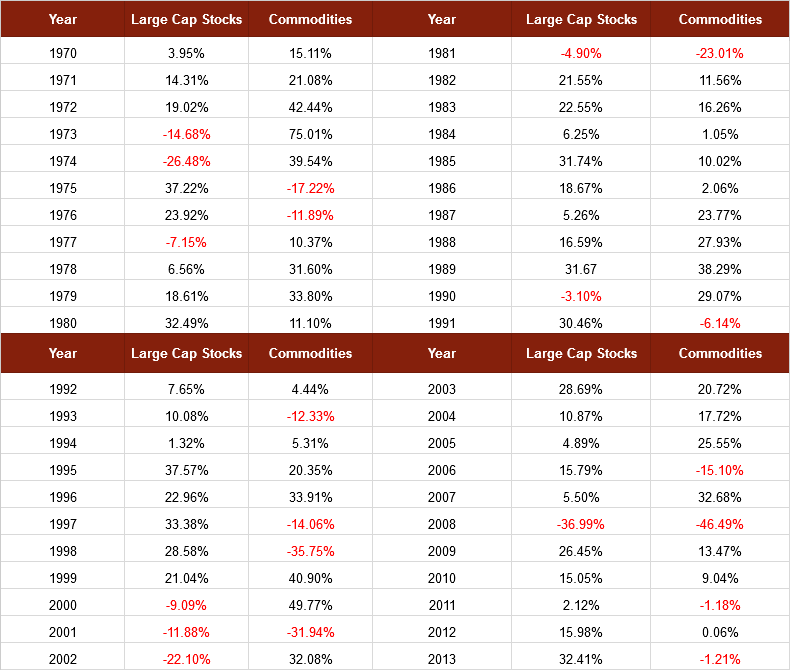

Commodities independently have historically been more volatile than stocks with a higher standard deviation of returns over the last 40 plus years. Since 1970, US large cap equities have posted a standard deviation of 17.63 versus 24.29 in the GSCI commodity index. However, when combined as a component in an overall asset allocation…they can serve an important role. All too often investors chase after the most recent top performing assets. Using commodities as an example, the last five years have been less favorable as the US and most of the developed world has seen a somewhat anemic economic recovery from the 2008 recession. Yet, if we were to examine average returns of the broad based commodities market in comparison to the US large cap stock market, we find that the average returns are not much different. During the period of 1970 thru 2013…US large cap equities posted average annual returns of 10.41%, while commodities posted average annual returns of 9.21%.

What is important to note by looking at the following chart is the individual year-over-year returns. What we find is that in many years in which stocks suffered…commodities offered a cushion to portfolio returns. In many years the inverse was also true. During periods of extraordinary deflationary panics such as 1929 or 2008, asset classes often become highly correlated. However, we also find that in years like 2002 as the tech bubble had imploded and the US was recovering from the events of Sept 11th…commodities offered a substantial reduction in overall portfolio volatility.

It is also important to recognize that a proper investment asset allocation is defined by multiple asset classes and sub-asset classes of satellite investments to compliment core holdings like US large cap stocks. Commodity holdings are just one part of such a strategy. As a result of the high volatility that accompanies a broad basket of commodity holdings, investors should likely limit exposure in the commodities markets to a reasonable percentage of their portfolio. Investors who use the aid of a financial advisor should consult with them before incorporating new holdings into their longer term investment strategy.

Commodities as an asset class can be a bit more difficult to own outright. It is unadvisable for investors to trade in futures contracts around the commodity complex, unless this is something with which they have had significant experience. In most cases it is much more suitable to use a mutual fund or an ETF which diversifies across a broad range of futures contracts. Unfortunately, due to the structure of many commodity products in the ETF product space, they often report tax liabilities on a K-1 rather than a 1099. This is irrelevant for retirement accounts, and does not increase liability…but may delay income tax returns for non-retirement accounts, as K1’s tend to be issued later and often close to the tax deadline. In the event that an investor wishes to avoid the K1 filings, there are a number of open-ended traditional mutual funds that have broadly diversified commodity holdings. As in any mutual fund, expenses should be monitored in addition to portfolio holdings to ensure the fund achieves a truly diversified set of commodity holdings consistent with the benchmark.

Filed under: Articles

Comments: Comments Off on What Role Should Commodities Play In A Portfolio?

People can find themselves under a pile of debt for a variety of reasons. Sometimes we fall upon hard times due to a set of unfortunate circumstances beyond our control. Other times we may have simply lived irresponsibly for periods in our life and not given enough consideration to the long-term implications of our actions. Debt can come in many forms. While it’s easy to understand the importance of getting out of debt, sometimes we don’t prioritize how we eliminate these liabilities in the most effective way.

Home Loans

When eliminating debt it is important to consider not only the interest rate you are paying, but also the tax implications. Eliminating the primary mortgage on your home is typically a great idea that is easily accomplished with extra principal payments. Yet keep in mind that the interest paid on your primary residence is most often tax deductible. So making extra payments towards the home may not be the smartest first priority if you have other debts. In cases where one is subject to a substantial Alternative Minimum Tax (AMT) liability, this deduction, along with others, may be reduced or excluded, and the priority of which debts should be paid down first would have to be revisited.

In the case of home equity lines of credit (HELOC’s), the first 100k is usually deductible only if it were used for the purpose of home improvement. If you took out a home equity loan to pay off other debts, then the deductibility of the interest is depends on when the loan was issued and the loan-to-value ratio of the loan. Loans issued prior to Oct. 13, 1987 are subject to different criteria. If the funds were used for home improvement, then the limit on deductible interest is a collective total of $1 million ($500k for a single filer) in debt service in total taken against the home.

Deductions on a HELOC for a second home are more stringent. You can typically deduct the interest if you do not rent the property. If you do rent the property then you must live in it for at least 14 days per year, or 10% of the days you choose to rent it, whichever is the greater. The interest rates on many HELOCs are variable and therefore you should place a larger priority on this type of loan, when compared to the primary mortgage. While many variable-rate HELOC’s have limits on the number of interest rate increases per year, we are currently in a period of historically low interest rates, which means rates are almost certain to rise.

Auto Loans

In such a low interest rate environment someone with good credit can often negotiate very low financing rates on an auto loan, sometimes as low as 0%. However, for most individuals, auto purchases aren’t tax deductible. If you’re buried in debt, you may not have a great degree of flexibility or the best credit. In cases where there is sufficient equity in the home, debt consolidation through refinancing may be advisable to pay off auto loans by pulling the equity from the residence to lock in low rates. If it is a cash-out refinance, you may be transferring a non-deductible interest expense into a deductible interest expense. Most often an auto loan by itself is not enough to warrant a home refinancing opportunity, but it may be attractive in conjunction with other debt consolidation and lower available rates. People who are self-employed and have a car that is used exclusively for business purposes can deduct the cost of the auto as a business expense, as they can with other transportation expenses, including leased vehicles. If you opt to purchase a car, the tax benefit will be realized later. In such cases, this type of debt consolidation may not be advisable. As your company eventually grows and earnings increase, an auto lease will remain deductible and can be used to reduce business income. Yet home mortgage interest deductibility can be partially phased out should the alternative minimum tax begin with a higher adjusted gross income.

401k/Pension Loans

As important as it is to reduce debt over time, it should not be done at the expense and sacrifice of your retirement, with the exception of desperate circumstances. In fact, we should all target a minimum savings rate in our retirement plans of at least 10% of our income while employed. Your creditors will always be there, and the first rule of financial planning is “the first bill you pay is yourself.” Loans against retirement plans are not a good idea in general. They are designed to be a last resort in a desperate situation. However, if you have already taken one or are in need of one…they are often a better solution in an emergency than adding to credit card debt. Although the interest on a 401k loan is not deductible, you are paying that interest to yourself…not to a financial institution. The interest rate is typically fixed, and the loans are most often five years in duration, although they can be ten years if it is for a first-time home purchase. The true cost is the time that the principal from the plan is not invested towards your retirement. Additionally, should you default on the loan, your credit would not be impaired since you borrowed from yourself. However, you would be subject to ordinary income tax rates on any amount not repaid. Additionally, if you are below the minimum retirement age of 55, you would be subject to an additional 10% penalty on the amount not repaid.

Credit Cards

The most dangerous of all debt to create is credit-card debt. The reason is the extreme interest rates that are frequently charged on credit card borrowings. While credit cards often offer wonderful rewards programs, it is important to pay them off immediately. They can go a long way towards establishing credit for those who cover their expenses at the end of the monthly billing cycle, but if you spend beyond your means, you may find yourself paying financing charges in excess of 20 or even 25% annually…with no tax deduction available. This is generally the first place you want to begin to reduce debt if you are already in over your head. In some cases, it may be advantageous to consolidate debt into your home mentioned above. Sometimes there are promotional opportunities to consolidate credit cards into another card that offers you a 0% percent interest rate for a period of time. While this may not be a bad idea in the short term, continuously opening new cards for balance transfers will negatively impact your credit.

School Loans

Assuming you are reaping the rewards of a useful education, this may be debt well worth creating. The tax benefits of student loan interest can make prepaying such loans lower on the priority scale when compared to reducing things like credit card liability. The rates are typically much lower, and the interest is often a reduction to your adjusted gross income. Those individuals who are responsible with credit cards can often use programs like the UPROMISE program in New York. Such programs offer the ability for the points accumulated on credit cards to be applied to paying down principal on student loans.

While there are various forms of debt that one can find themselves in, it is important to prioritize the extra payments or cash flow towards the most logical areas. When doing so, you want to look at both the interest rate paid as well as the after-tax interest rate paid on deductible loans. Even when an individual has the cash available, it should be weighed against what that cash would earn if not used for debt reduction. Consulting with your tax advisor on your tax status in connection to these issues can be helpful. It is important to try to avoid bankruptcy proceedings. While a bankruptcy can alleviate some short-term issues, it will greatly impair your credit for years to come. Additionally, bankruptcy is about asset protection. If you are someone with no significant assets…it can be wasteful, time-consuming process.

Lastly, it is a good idea to take control of these issues on your own and educate yourself. There are numerous companies that advertise their ability to get you out of debt. Most of them time they are simply negotiating things like lowering the balance that a creditor is willing to accept. This is something you can easily do on your own without retaining costly debt-reduction services. Such negotiations, even when you are successful, can still impair your credit. For example, any unpaid balance owed on a credit card that is deemed settled by creditors is taxable income to you in that year.

It’s always advisable to live responsibly and avoid these issues. Yet, if you find yourself in a situation with a sizeable debt burden, be sure to prioritize the liabilities as discussed above. Itemize a budget by essential and discretionary spending so you can properly categorize what can be reduced or eliminated monthly. Sit down and put a plan of attack to paper, and follow it the best you can. Debt comes from many sources…and sometimes due to circumstances beyond our control. When we prioritize how we eliminate debt…like all financial decisions, weigh the entirety of the circumstance and alternatives.

Filed under: Articles

Comments: Comments Off on Things To Consider When Prioritizing Your Debts