State Street Global Advisors: Election Chart Pack

State Street Global Advisors Election Chart Pack

State Street Global Advisors Election Chart Pack

Russell Investments: Global Market Outlook Q4 Update

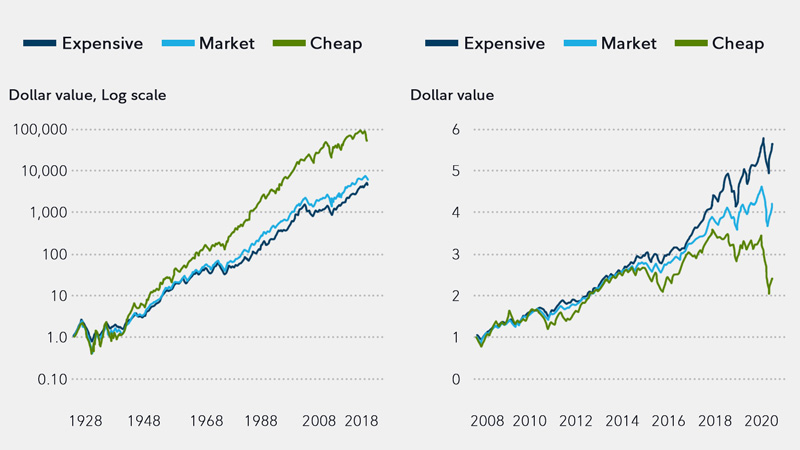

Value stocks vs Growth stocks, which is the better investment? The debate between value...