Over the last decade much has been made of the cryptocurrency space, more specifically Bitcoin. While some have embraced it, others still shun it as either an asset or a currency. To date, it is not something we are comfortable investing in. However, we remain open to the possibility as Bitcoin and other such cryptocurrencies evolve.

The blockchain technology that Bitcoin was built on has many possible benefits across various industries. However, beyond the technology that it sits on, the first challenge with Bitcoin is that calling it an asset is questionable. Clearly it is not a tangible asset. That cannot be questioned. However, can it be called an intangible asset?

The Financial Accounting Standards Board defines an intangible asset as: “An asset, other than a financial asset, that lacks physical substance”.

The International Accounting Standards Board defines an intangible asset as: “An identifiable non-monetary asset without physical substance.”

The first question would be, is Bitcoin a monetary asset?

It certainly seems to be used as one in recent years by a large number of people. One of the arguments in favor of Bitcoin is that as a monetary alternative it has a theoretical finite supply, whereas dollars, or any other monetary system established is now infinite thanks to central banks globally. It’s easy to see why some may find this attractive.

Let’s first look at the US Dollar.

When the United States left the gold standard in August of 1971 an ounce of gold was $35.00.

According to the US Census Bureau the average cost to buy a gallon of Milk in 1971 was about $0.356. In other words, in 1971 it would have cost you approximately 0.01 ounces of gold to buy a gallon of milk.

If we fast forward to 2024, gold is approximately $2,140 an ounce. According to the St. Louis Federal Reserve, as of February 2024, the average price of a gallon of milk in the United States is about $3.94.

That means that it would now cost you only 0.001 ounces of gold to buy that same gallon of milk. Milk is now 11 times more expensive since 1971. Yet, in terms of real purchasing power, you need only 1/10th the amount of gold to buy the exact same item.

What this shows is that gold has mostly kept up with the price changes. Obviously, this would vary somewhat depending on which purchased item we were examining, as some products have grown in price faster than others.

But what about income?

According to the US CensusBureau, the median income in 1971 was $10,290. In 2024, the median income is estimated at about $75,000 based on the most recent census data.

In other words, you would need a median national income of $102,900 (ten times the wages of 1971) for wages to have kept up with the price of gold to buy that same gallon of milk. Alternatively, you would need a $113,190 median income to see a zero loss of purchasing power in US dollars.

What this tells us is that while the average American is making substantially more than they were making in 1971, the U.S. dollar has lost a substantial amount of its purchasing power, and the increase in wages are nowhere near enough to keep up. More plainly stated, the median income has lost more than 33% of its real purchasing power since the US left the gold standard in 1971.

Considering that one of the two primary mandates of the Federal Reserve is that of price stability, it seems fair to say that they have failed terribly.

With this data, it’s easy to see why one would look for an alternative to the US dollar. After all, there is a long global history of fiat currencies self-destructing due to the hubris of policy makers.

The benefit of the gold standard is that it offered the ability to convert your dollars to physical gold. Gold on its own has intrinsic value. It has various applications, from jewelry, to electronics, to aerospace, and even some medical applications, making it a true asset. The past convertibility of currency to gold served as a potential check on policy makers from runaway spending, as they would fear a run on their currency. This limiting factor added greater price stability.

What about Bitcoin?

Does the limiting factor of a finite number of coins serve as a check on inflation? In theory the limiting aspect is a positive. However, the question of intrinsic value still persists. As an example, what if large numbers of people choose to adopt a different cryptocurrency for use in the exchange of goods and services. Perhaps one is developed that is more technologically efficient and easier to use. Then what is the intrinsic value of Bitcoin as it becomes a secondary or even peripheral option?

Bitcoin has no earnings, it has no cashflow, and it is backed by no tangible assets. While the US dollar is also no longer backed by any tangible assets for which you can convert to, it is still backed by the taxing power over the US economy. That alone is not enough stability, as there is clearly nothing that stops the political class from printing more money than the US government takes in from tax revenue. In fact, currently the US is setting records for the highest tax revenue in history, and still manages to create another trillion in deficits every 100 days.

Ultimately, a currency should serve as a store of value. Just the price movement alone on Bitcoin alone should demonstrate it is not a store of value. Recent history saw Bitcoin fall from more than $67,000 per coin in November of 2021, to $16,000 per coin in November of 2022, before climbing back to more than $70,000 per coin recently.

To put that into perspective, that’s a -77% drop in one year. Imagine if you had $1,000 in the bank and one year later it had dropped to $230, yet you had taken no withdrawals. It’s probably fair to say most people would be quite upset. While the same can happen in the stock market, we don’t treat the stock market as a store of value. It is not a currency, but rather a long-term investment designed to grow.

Based on this information, it is fair to say that Bitcoin is not really a currency. At least it does not behave like one would hope and expect.

If Bitcoin is not a currency, but some other form of a non-monetary asset, then where does it derive its value. When thinking about the stock market, what makes a stock go up in value? In the short term a stock may go up or down for all kinds of speculative reasons. However, in the long term the only thing that matters is earnings. When we buy a stock, we are buying a business in the hopes that its profits will grow.

But Bitcoin has no earnings. It has no cash flow. It sells no product. One can argue it provides a service, as many businesses do. But when a business provides a service, its goal is to grow its customer base that utilizes this service to grow its market share so the business will grow its earnings. If the number of people that utilize Bitcoin were to increase tenfold, how much would its earnings grow by? The answer is zero, because it has no earnings.

Based on all available data, it seems that Bitcoin is built on nothing more than a lack of trust in monetary policy. While we share that same lack of trust, we don’t think Bitcoin is the answer. Perhaps a return to the gold standard or some other form of a monetary standard is the answer. In fact, many nations around the world have already begun such a coalition to return to the gold standard in an attempt to limit their exposure to the US dollar. While that is more of a geopolitical discussion for another time, the question of whether Bitcoin is the solution, or a viable investment is the issue at hand.

In many ways, Bitcoin seems to resemble the “Tulip Mania” period of the Dutch golden age of the 17th century than it does a real currency.

At this point, it seems nothing has changed that would alter our views on avoiding Bitcoin or any other cryptocurrency. Perhaps one day Bitcoin, or some other Crypto will be built with the direct backing of some form of a monetary standard, such as gold, silver or a basket of commodities that can be audited for authenticity, converted on demand, and enforced. Until that time, we remain skeptical.

Filed under: Articles

Comments: Comments Off on Bitcoin: Currency or Asset?

Market volatility is not something that investors enjoy, as none of us like to see our assets decline, even if it is for just a brief period of time. However, volatility is inevitable and must be dealt with to be a successful investor.

When investing for the future, most investors use some form of retirement plan for tax advantages, while others save independently in after tax accounts. However, while we save for the future, most often we are consistently peeling off a percentage of our earnings to allocate towards future goals. Since most Americans are paid either weekly or bi-weekly, we slowly allocate a percentage of this in what is known as dollar cost averaging.

Dollar cost averaging is a strategy whereby an investor contributes a set dollar amount or percentage over a time frame to their investments. Most of the time, dollar cost averaging happens because you are simply not in a position to invest all of the money at one time, as your employer is not going to pay you your compensation for the next 30 years in advance. However, in some cases investors do come into a large lump sum of money for various reasons, and they have a choice to make. Should they invest all of the cash at one time, or dollar cost average over a period of time. After all, committing a large amount of money at once just to see it immediately decline, in some cases substantially, can be rather distressing.

Fortunately, there is some data on which works better. Vanguard completed a study on this very topic which revealed that 2/3rds of the time the lump sum investment outperforms, while 1/3rd of the time dollar cost averaging yielded better results. The same study demonstrated that the longer the period of dollar cost averaging, the more it favored the lump sum. The reason for this is because historically markets are positive roughly 75% of the time, so the longer you wait, the more likely you are to be paying more for the same investments in the future.

Nevertheless, in the case of the typical 401k investor that is consistently deferring money from their paycheck for their future retirement, dollar cost averaging is the only choice. Yet, during periods of volatility, you may benefit from the market chaos.

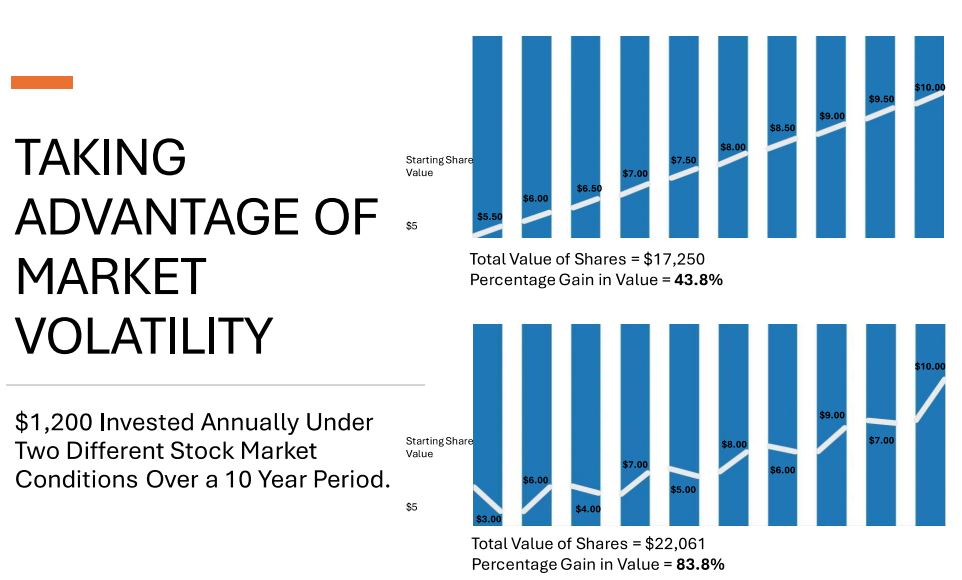

As illustrated in the image above, when we look at two contrasting scenarios in which each investor invests $1,200 annually starting at $5 per share and finishing at $10 per share over a 10-year period, we see different results.

The first investor saw a steady increase annually in their investment, and likely realized much less stress as their investment consistently increased with no volatility whatsoever, yet the paid more for each subsequent investment.

While the second investor saw choppier markets with periodic volatility causing annual investments to take place in both positive and negative years. This helped to bring their average cost down.

The results demonstrate the following:

Investor 1-Initial Investment – $12,000

$17,250 final market value and a cumulative return of 43.80%.

Investor 2-Initial Investment – $12,000

$22,061 final market value and a cumulative return of 83.80%.

It’s important to keep in mind that the first scenario of markets consistently rising with no downturns is almost certain not to happen. While volatility can be mild or extreme at different points in time, a good investor will stay the course. What this demonstrates is that while markets decline and volatility is not enjoyable in the moment that they happen, if you are disciplined and consistent investor, you can use this to your advantage.

Filed under: Articles

Comments: Comments Off on Market Volatility: Friend or Foe?

The importance of diversification has been well established across the investment research literature over many decades. It is a relatively easy principle for most investors to accept. The words “don’t keep all of your eggs in one basket” is one of the most common phrases repeated over time.

However, asset allocation is just as important. The concept of asset allocation is based on the notion that not only do you not want to own just a few companies, but you also want to own assets that demonstrate a lower correlation to each other. A lower correlation simply means that multiple assets may increase over time, but at different times, for different reasons, in different environments.

As an example, the use of owning stocks across various market capitalizations, (Large, Mid & Small Cap stocks), and different regions of the world help diversify a portfolio. Additionally, the use of other assets such as fixed income, real estate, and commodities further lower correlations in an investment portfolio.

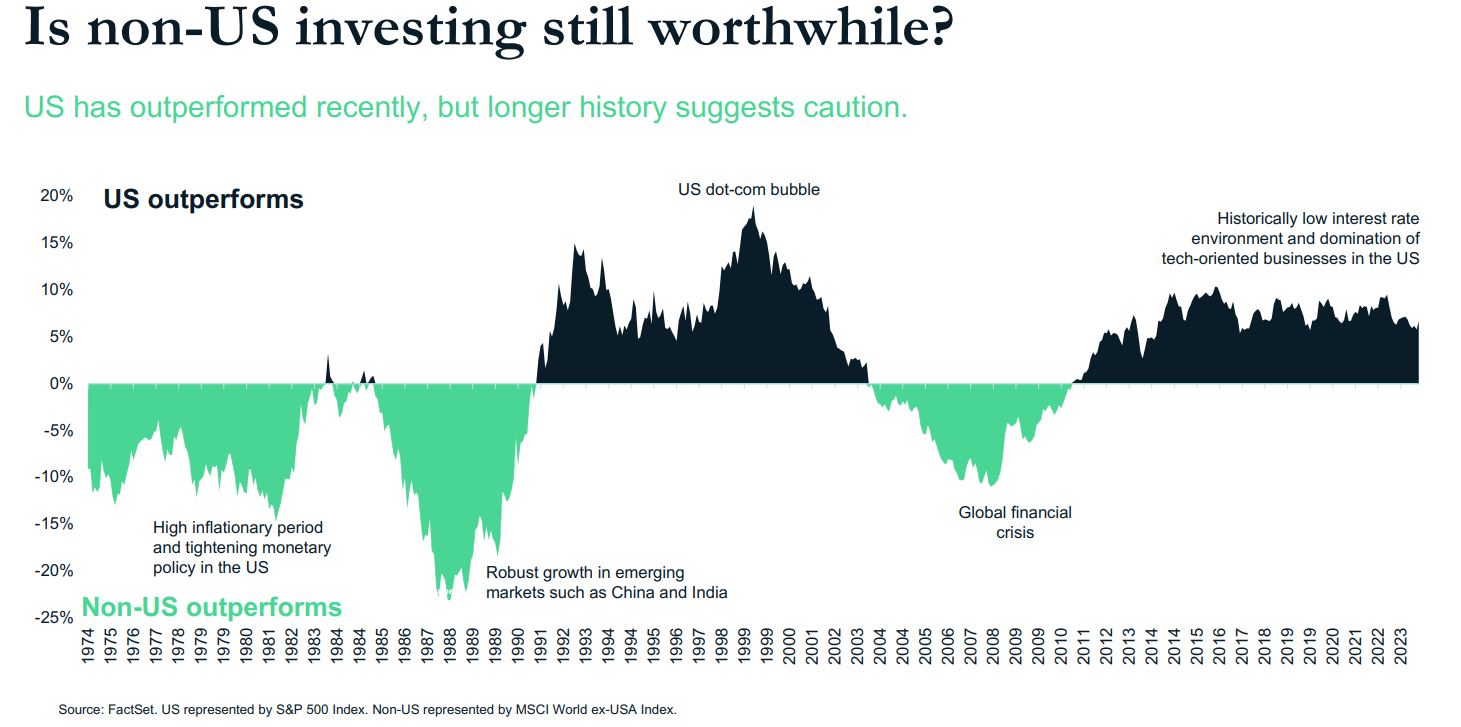

The use of international investments is one of the areas that has recently come under scrutiny as the US stock market, particularly the S&P 500 index has significantly outperformed international stocks for the better part of the last 15 years. However, as the chart above courtesy of Diamond Hill Investments shows, it is not necessarily unusual for US or foreign equities to lead for significant periods of time.

During the seven years from 2004-2011, international stocks had a more favorable performance. During the seventeen years between 1974-1991 international stocks also outperformed. This is often overlooked because during periods like the 1980’s US stocks did exceptionally well. Yet, for most of that period, international stocks did even better.

When looking at recent history, not only do we see that the US has had an extended period of recent outperformance but is also trading at relatively high prices by comparison. As an example, as of January 31st, 2024, the MSCI USA Index was trading at a price to earnings ratio (PE ratio) of 25.4. While the MSCI ACWI ex USA index (which is a foreign stock index) was trading at a PE ratio of 14.9, making it comparatively cheap.

This data suggests that foreign stocks are substantially undervalued and more attractive when compared to the US stock market. Does this mean that foreign stocks will outperform in the near future? Not necessarily, or at least not right away. However, it does make a strong case for owning foreign stocks. History suggests there will be a reversion to the mean, and at some point, foreign stocks will lead the markets again. Timing such a reversal is just as futile as timing markets in general. The more important lesson is that foreign stocks play a role in a portfolio over time.

As a result, we believe there should always be some degree of exposure in foreign stocks as part of an overall asset allocation to aid in the diversification of a sound long-term investment strategy.

Filed under: Articles

Comments: Comments Off on Foreign Stocks: Do They Still Make Sense?