Vanguard Economic & Market Outlook for 2024

Vanguard Economic & Market Outlook for 2024

Vanguard Economic & Market Outlook for 2024

Franklin Templeton: 2024 Capital Market Assumptions

Russell Investments – Global Market Outlook 2024

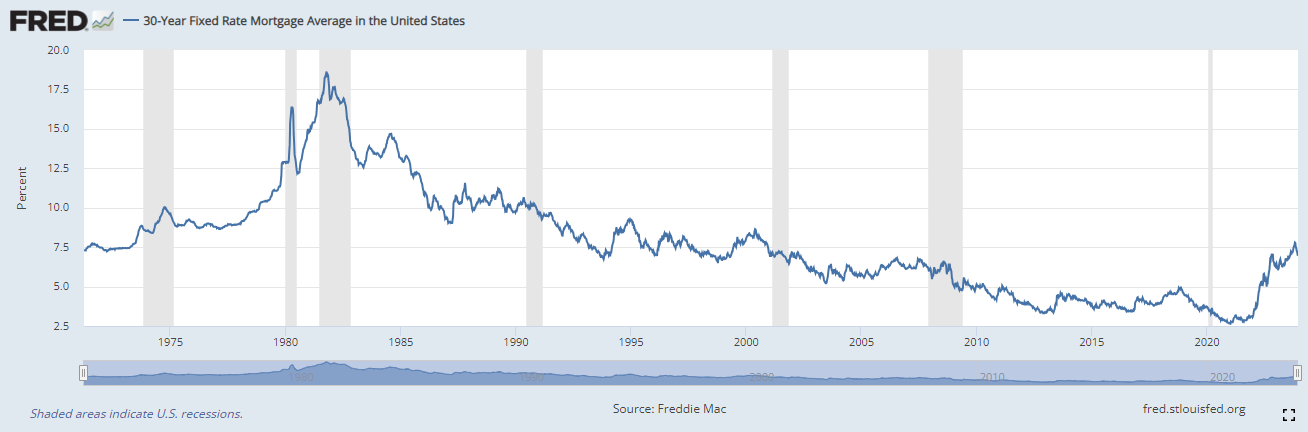

Recently we’ve seen signs of softening in the housing market due to the increase...