As the calendar turns to the new year, things rarely stay the same, and that applies to financial planning, as tax laws and retirement plan changes evolve. This year there will be some impactful retirement plan changes from the Secure Act 2.0, which was passed in late 2022. Also, there are increased limits and thresholds for retirement accounts along with other notable changes. This is a highlight of some of the upcoming changes.

The Secure Act 2.0 is still providing benefits to retirement savers. Starting this year retirement plans will allow for a “Super Catch-Up”. This Enhanced Catch-Up allows savers that are aged 60 to 63, to add an additional amount to their 401k, 403b, 457 or SIMPLE IRA.

In the case of the 401k, 403b & 457 plans the catch-up amount will increase from $7,500 to $11,250 for those ages 60-63 and will be indexed for inflation beginning in 2026.

In the case of the SIMPLE IRA, the limit increases to $16,500 and the catch up is $3,500 for those 50 and older. However, the “Super Catch Up” further increases the contribution from $3,500 to $5,250 for those ages 60-63.

Other notable changes to new 401k and 403b plans are automatic enrollment and automatic portability. If a new 401k or 403b is established, employees must automatically be enrolled and started with a 3% minimum enrollment contribution.

Standard plan limits have also increased for qualified retirement plans. Employee contribution limits have increased to $23,500. The catch up for 50 or older is $7,500 unless the employee is eligible for the “Super Catch Up” referenced earlier.

The Section 415 limit, which is the maximum total contribution for qualified plans for 2025 is $70,000 plus your catch up.

Individual Retirement Account (IRA’s) limits remain the same at $7,000 and the Catch-Up contribution for those 50 and older remains at $1,000.

Health Savings Account limits increase to $4,300 for an Individual and $8,550 for a Family. The Catch-Up contribution for ages 55 or older is an additional $1,000.

The Qualified Charitable Distribution limit in 2025 is $108,000. A Qualified Charitable Distribution is the maximum annual amount that someone 70.5 or older can distribute out of an IRA to charity and avoid income taxes.

Medicare Part B Premium will increase to $185 per month per person. The first IRMAA (Income Related Monthly Adjustment Amount) will start when your Modified Adjusted Gross Income (MAGI) exceeds $106,000 for single filers and $212,000 for married filing jointly.

Medicare Part D outlays are now capped at $2,000.

The Social Security cost of living increase for 2025 is 2.5%. The average increase for recipients is $45.

The annual gift exclusion increases this year to $19,000 per person.

The Federal Estate Exclusion increases to $13,990,000.

The Standard Deduction in 2025 will be $15,000 for Single filers and $30,000 for Married Filing Joint. The additional deduction for ages 65 or older is $1,600 ($2,000 for those unmarried who are not a surviving spouse).

The Child Tax Credit remains at $2,000, with $1,700 being refundable.

This provides just a brief overview of some of the more notable changes to 2025. It’s important to remember that with a new administration, as well as a new congress set to take office, there will likely be some additional changes to the tax code moving forward into 2025. As always, we would suggest that individuals speak not only to their financial planner, but also contact your tax professional to see how these changes may impact you.

Filed under: Articles

Comments: Comments Off on 2025: Important Retirement Plan and Tax Law Changes

Most investors have heard of market indices such as the S&P 500 or the Dow Jones Industrials, but not all know exactly what that means. Market indices can be constructed differently. But in the case of the S&P 500 index it is a mathematical formula of the top 500 public companies in the United States weighted by market capitalization (cap).

The market cap is determined by multiplying the price of a stock by the number of shares outstanding. This produces market cap numbers in the billions and in some cases trillions when it comes to the S&P 500.

The way in which the S&P 500 is built, the larger the market cap of a particular company, the more proportionate representation they receive in the index. As an example, Microsoft makes up more than 7% of the S&P 500, while a company like Caterpillar makes up less than 0.50% of the index. This means that the more a stock gains in price above the rest of the market, the more it will gain representation in the index. This formula has proven very successful over time, as beating the overall index has been proven to be nearly an impossible feat over any significant length of time.

However, at different points in time, this has led to significant concentrations in a few stocks that have significantly outperformed the overall markets. While that might be a fun ride up, it can lead to some increased risk in a less diversified portfolio.

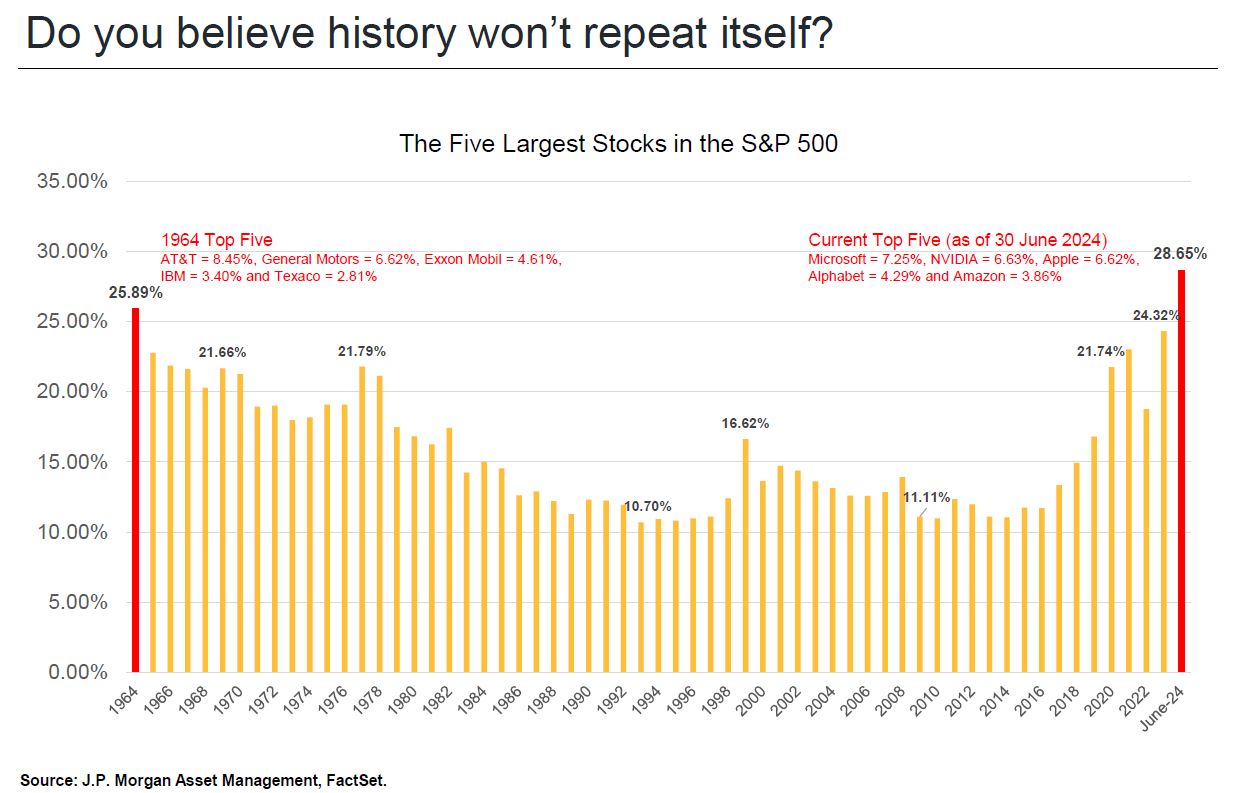

At the moment, we are living through just such a period. As the data provided by JP Morgan demonstrates, the top 5 companies in the S&P 500 make up about 28% of the overall index. That means if you invested $100 dollars in an S&P 500 index fund, $28 dollars would be invested in just those 5 companies, which is less diversified than most might imagine.

This level of concentration has not been seen since the mid-1960’s as we can see from the chart above. The last time this happened, the degree of concentration steadily declined over the next three decades.

In order for this concentration to decline, this means that either those top stocks have to decline, or they grow slower than the remaining companies in the index over time, or some combination of the two. In the long run, typically what happens is the rest of the market begins to catch up. However, in the short term, it could mean that there is an actual price decline in such concentrated holdings.

It’s difficult to predict what the short term will mean for the markets, and even more difficult when evaluating a group of just 5 companies. What we can do is look back at history and see that when a small group of names lead the market in such a significant way, this tends not to be sustainable.

Such data reinforces the need for a well-diversified portfolio that maintains exposure to numerous areas of the markets, including other asset classes. This doesn’t mean that there must be an immediate reversion back to a more balanced index. However, if history is any reliable indicator of what is to eventually come, that seems inevitable, and diversification will become even more important as markets begin to broaden out, and the biggest names do not necessarily continue to remain the leaders.

Filed under: Articles

Comments: Comments Off on S&P Stock Concentration: What Does History Tell Us?

It’s not uncommon to hear many young people suggest that home ownership is now unaffordable compared to generations past. In some of the more expensive areas of the country, this may very well be true. What about those that can afford a home, is it even worth it?

One of the reasons for home ownership is the need and desire for more space and more freedom to do what you want with a piece of property. That is impossible to quantify with a dollar amount, as we may all place a different value on that benefit. Others may see the maintenance of a home as an added responsibility that isn’t worth their time and further reduces its value in their eyes.

According to Economist Robert Shiller, from 1928-2021 the price of the housing market in the USA averaged 4.20% annually. Now this can be misleading. In order to calculate the true return, one would have to reduce the return by the carrying cost, such as property taxes and home maintenance. Then increase the return by the added tax benefits of deductions for mortgage interest and property taxes. These items are all specific to the individual, and to the specific property. Additionally, the increasing cost of a home can diminish over time as the mortgage is paid off and the carrying cost are reduced. However, according to Schiller, during that same time frame, when you adjust for inflation, the average return for the housing market is a little better than 1% per year.

Looking at that data one could draw the conclusion that you are better off investing your money where your historical returns in stocks have been closer to 10% per year. However, things are not necessarily that simple. If you don’t own a home, you need to rent. According to the Bureau of Labor and Statistics, the average rate of rental increase is about 3.5%-4% per year. However, in some periods that can be just as volatile as home prices. Over the last four years, the average cost of a rental is up more than 25% cumulatively. If one’s wages have not kept up, and nationally they haven’t, the cost of renting becomes more prohibitive.

Another consideration is the inherently volatile nature of the stock market. Just because someone opts to rent and redirect their capital to stocks doesn’t mean that they will stick with the stock market in the face of a substantial downturn. Because the stock market is far more liquid, the ability to panic and sell quickly is often the result for the retail investor. Year after year Dalbar produces research that says that the retail investor dramatically underperforms the stock market for just that reason.

An excellent example of this is the 2008 financial crisis, which was precipitated by a major downturn in housing. While many people were forced to sell homes due to losing a job or having excess leverage, those that didn’t sell saw their home prices rebound. Because of the inherent illiquid nature of real estate and the time it takes to list a property for sale, and then complete the sale, it is much less likely that someone will panic. When you don’t get a monthly statement showing the declining value of your home, you’re less likely to do something out of fear and panic as long as you can pay for the home.

The distinction between stocks and real estate in terms of the ability to liquidate them is an important one, because the national average return of either asset class is not always going to be realized depending on who the investor is, and their discipline to follow through on their investment strategy.

Ultimately, we can say that based on the historical returns of an investment portfolio you should be better off with stocks over real estate. However, that does not mean that owning a home is inherently the worse choice. We would argue that for most Americans, home ownership at some point in their life is the logical decision for a variety of reasons.

It is important to point out that for most Americans, there are also points in which renting makes much more sense. It’s not a good idea to overleverage yourself with mortgage debt. Renting while you are younger is not inherently bad as long as you are saving money and have a positive cash flow. It’s a good idea to save as much as you can for a down payment. The goal should be at least 20% to avoid mortgage insurance.

If you can’t commit to keeping a property for more than a decade, then renting probably makes more sense, as housing prices can decline and not recover for many years to come. If you’re in a job that may require you to relocate, or some other driving force may make it difficult for you to stay in one spot that long, it probably makes more sense to rent and save money.

We can also say the same for retirees. Many people retire and look to downsize. Buying another smaller home is not always the answer. There are more and more 55 and up rental communities popping up around the country. While many people look at renting as a negative, in some cases it makes perfect sense. If you are cash flow positive, there is nothing wrong with renting. You can still grow your nest egg for your heirs if that is a concern. The added liquidity and reduced responsibility from that home you sold may support increased travel in retirement beyond what you may have otherwise been able to do.

Ultimately, whether owning or renting makes more sense is case specific. Yet, it’s important to point out that renting isn’t always so bad. You don’t want to be forced to rent in retirement because you don’t have the resources to own. But for those with resources, sometimes it can be the better option.

Filed under: Articles

Comments: Comments Off on Real Estate: Should I Rent or Own?

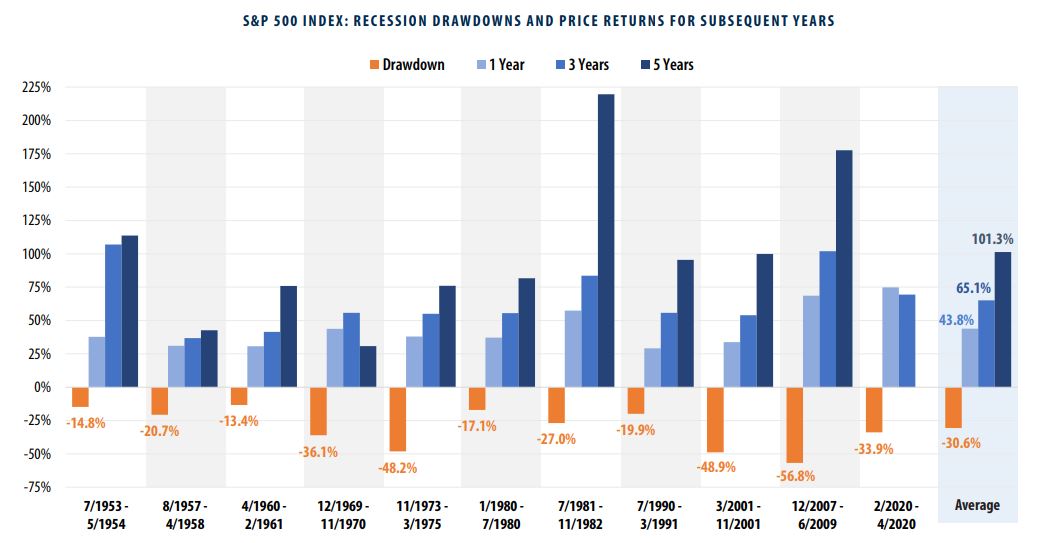

A common theme of concern among investors that most financial planners will hear just before a client is about to retire, or possibly already retired is that “I don’t have time to recover from a big market downturn”. The assumption is that you’re too far along in your life to be able to hold your investments long enough to see them rebound. While nothing is guaranteed, if history is any kind of indicator, that seems unlikely for most people.

What we can see from the chart above provided by First Trust is that on average, a market downturn during a recession is approximately -33%, and the average bear market lasts approximately 11 months. However, just 12 months following that market downturn, the average subsequent return for the S&P 500 since 1953 is about 44%. It just happens to be that a 44% return is roughly what you need to achieve to nearly a full recover from a -33% decline.

When we look a bit further into the future, the 3-year return on the S&P 500 is 65%, and 5-years out it’s a little better than 101%.

Let’s put this into perspective. If your timing was terrible, and you invested $100,000 the day before the market selloff began, and assumed the average downturn lasted 11-12 months, this is what your portfolio would look like:

12-months later – $67,000

24-months later – $96,346

48-months later – $110,558

72-months later – $134,871

It’s also important to point out that these averages assume that you would have 100% of your investment portfolio in stocks, which is rarely appropriate. Most investors are more suited to have a well-diversified asset allocation of many different asset classes to mitigate risk. As a result, the decline should not be as substantial, and the time to recovery is even shorter. A comparative look at the impact of market downturns on a well-diversified asset allocation, versus a portfolio fully invested in stocks can be seen in the prior article from 2020:

This is not to suggest that market downturns would not have a significant impact on a retiree’s portfolio. In fact, it can be significant if it happens early in retirement when an income is needed from an investment portfolio. Selling into losses can accelerate asset depletion much faster. This is due to what is often referred to as the Sequence of Returns Risk.

This risk can be explained in more detail in this prior article:

However, it is more impactful when an investor sells out of fear and panic, which typically happens at the worst possible time, as opposed to maintaining a sound investment strategy. It is extremely important that an appropriate risk level is identified and implemented based on the cash flow needs of a particular investor. If this is done correctly, panic should never be the response. A good financial planner will help evaluate your budget and how it progresses over the years to adapt the risk level accordingly and maintain a reasonable cash flow from the portfolio.

It’s important to understand that while history doesn’t always repeat itself precisely, it tends to rhyme. Markets have had an extraordinary ability to revert back to their statistical mean over the long run. And as the evidence demonstrates, historically that isn’t a very long wait most of the time.

Filed under: Articles

Comments: Comments Off on How Long Does it Take the Market to Recover?

The democratic process of electing our leaders is fundamental to our republic of representative government. But how much do elections matter? Well, that depends on what you are asking the question about. Elections certainly matter in terms of policy changes that can impact international relations, social policy, regulatory policy, as well as economic policy. However, it is important to understand that when evaluating financial markets, that is something entirely different then evaluating economics.

We have often said that the economy and the markets are more like cousins than siblings. What is meant by this is that there is a relationship between the two, but they are not necessarily going to move in tandem with each other.

Economic data, depending on what type of data you are examining, is often a broader look at the overall business conditions across the nation, or the world at a point in time. Analysis of the financial markets is more of a look at the valuation of assets at a point in time. Common sense would dictate that in an expanding economic environment in which we see stronger growth would eventually lead to higher asset prices. That is generally true, but that doesn’t mean that asset prices can’t or won’t increase during periods of anemic growth. During the post-2008 financial crisis period, we saw a very anemic growth rate in real GDP growth or nearly a decade. Yet, markets did very well during that period. There are various reasons that this can be true.

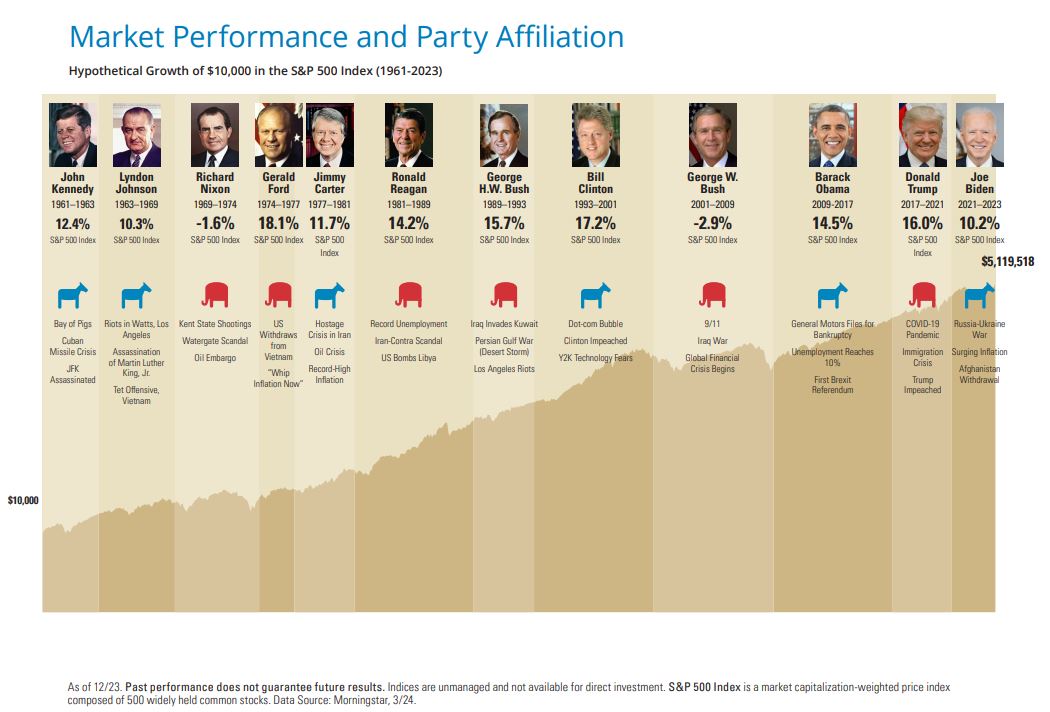

As an example, looking at the chart above provided by Hartford, we can see some data.

Since 1960, there have been only four Presidents that served a consecutive eight years in office. Looking at the last four such administrations we can see in the data the following:

During the Reagan Presidency, Real GDP grew at 3.5% annually, and the S&P 500 averaged a 14.20% annual return.

During the Clinton Presidency, Real GDP grew at about 3.9% annually, and the S&P 500 averaged a return of 17.2%

During the Bush (43) Presidency, Real GDP grew at 2.2%. and the S&P 500 averaged a -2.90% annual return.

During the Obama Presidency Real GDP averaged 1.70% annually, and the S&P 500 averaged a 14.5% annual return.

As we can see, there is a disconnect between economic growth and market growth, and no connection to any particular political party.

The lower rate of economic growth over the last two decades is concerning, and likely due to the massive rate of growth in entitlement spending. The lower growth rates are certainly not a positive for the economic conditions of the average citizen. However, although 3%-4% annualized average growth in GDP may no longer be achievable with the size of the current Federal spending levels, that does not mean that markets cannot continue to grow.

It’s important to point out that since 1960, the average rate of growth in the M2 money supply is about 4.50%-5.00% annually. As the money supply grows, those dollars must go somewhere, and many of them will chase after assets.

It’s also important to point out that we are not necessarily endorsing the Fed’s policies around money creation. However, printing money as a policy response to an economic crisis is the recent reality, and likely the future policy response the next time a crisis develops.

Remember that GDP is a measure of productivity, and the M2 money supply is a measure of new money in circulation amongst the population. If that latter grows faster than the former, the value of the dollar is declining, also known as inflation.

How do we best combat inflation?

The best answer to combating inflation is to own assets, as opposed to holding cash, which is declining in value. What this tells us is that even when the US economy is growing at a slower pace, the value of assets can still increase.

Not all of that increase will be due to inflation. There are also deflationary forces that can improve the price of an asset. Once such example is the increase in technological advancements that increase efficiency and improve the profitability of a company. Remember that what drives the price of a stock in the long run is simply the growth in profits.

What the evidence tells us is that while we may all have different preferences on who we prefer to see in office, this historically doesn’t change much in terms of the stock market. Markets continue to grow regardless of policy positions.

A simpler way to think about this is that no matter who is in the office, the business community will figure out a way to make money. Whether you have the most restrictive regulatory policies, or the most laissez-faire economic policies, Amazon will figure out a way to deliver a package to your front door and make a profit in doing so. And if they can no longer do so, someone else will. In a more business friendly policy environment where demand increases for their products, they will hire people and expand to new locations in order to achieve their target profit growth. In a less friendly business environment where demand decreases, they will lay off workers and cut costs if necessary to get to their target profit growth. Either way, they will grow profits or be replaced.

The business community simply wants to know the rules, so they know how the game will be played. This is why markets love political gridlock. The more the rules are known, the easier it is to set up a business strategy around them.

Filed under: Articles

Comments: Comments Off on Elections: How Much Do They Matter?

One of the more common estate planning mistakes we have seen over the years is the use of a trust as a beneficiary of an IRA account. This is not to say that such a strategy never makes sense. However, it rarely does make sense for most investors.

A trust can serve several purposes depending on the type of trust that is drafted. A revocable trust exists to avoid probate and simplify the settling of an estate privately outside of the surrogate court. Whereas an irrevocable trust can serve many purposes, including credit protection, minimizing estate taxes, Medicaid planning and various other strategies.

When listing an individual as a beneficiary on an IRA, you already avoid probate as the assets pass directly to the beneficiary via a beneficiary IRA, also sometimes called an inherited IRA. However, IRAs inherited by a non-spouse are required to follow distribution rules that we have outlined in previous articles that typically require assets to be liquidated over a 10-year period. More information on these rules can be found here:

In the case of a traditional IRA, these distributions are taxable events. When an individual person is listed as the beneficiary, a beneficiary IRA is created on their behalf, and they realize the income directly, which is taxed at their own ordinary income tax rates. However, when a trust realizes the income, the situation often becomes unnecessarily much more complicated.

Remember that when a person creates and funds a trust, also known as the grantor, the trust becomes irrevocable upon their death, even if it was drafted as a revocable trust. If that trust is named as the beneficiary, it doesn’t matter if the trust names an individual or group of people as the ultimate trust beneficiary. The inherited IRA must be opened in the name of the trust, not the individual. In doing so, this means that an extra step is taken, along with possible negative tax consequences.

When a trust receives income, the income is taxed at trust tax rates, which are greatly accelerated to the highest marginal tax rate. This means that the money that is distributed will often be taxed at much higher rates than they otherwise would have before the money was contributed into the retirement account years earlier. The only way to avoid this is for the trust to then distribute the money to the named individual beneficiaries in the trust, and then issue each of them a K-1 form so they can realize the income at their individual tax rate. Then the trust must use that K-1 as a deduction against the income it received from the IRA to avoid the income at trust tax rates. All of this must be done annually until the distribution of the IRA is completed at the end of the 10- year period. This creates a lot of extra work to get the money to the same people that could have been listed directly on the IRA beneficiary form and would have received the money directly.

It’s also important to point out that while a trust still may not make sense as an IRA beneficiary, when it’s a ROTH IRA, the tax impact of the distribution is irrelevant, as the ROTH distribution is tax free no matter who is the beneficiary.

Does this mean that under no circumstances should a trust be listed as a beneficiary? Not necessarily. Some trusts are designed to be a conduit trust, which simply means that the trustee distributes the assets directly to the beneficiary, and then the trust is effectively closed out. While other trusts are accumulation trusts and continue to be used after the death of the grantor that funded it.

Unfortunately, many families have extenuating circumstances with some of their beneficiaries that might be a reasonable reason to limit their access to the money that was left to them. What if a beneficiary had a drug addiction, or a gambling problem, or possibly just a spendthrift that was irresponsible with handling money. In such cases it may make sense to have the trust receive the assets and name a trustee that will limit distributions to the beneficiary even after all of the IRA funds have been distributed to the trust. While any funds the trust receives from the IRA that are not distributed to the individual beneficiaries will be taxed at trust tax rates, the tax bill may be worth the cost to avoid placing the funds in the hands of someone that may be inclined to squander the money in ways that the grantor doesn’t approve of and would like to prevent.

Other scenarios in which a trust may be named as the beneficiary could be a special needs trust. Special needs trusts are created for individuals that suffer from various physical or mental disabilities and qualify for government benefits. The money held in the trust does not impact their benefits, whereas funds in their name directly may impact their benefits. If someone with such a disability were the beneficiary of an IRA, the use of such a trust may make sense.

However, in our experience most of the time when a healthy competent individual is the ultimate beneficiary, the use of a trust as an IRA beneficiary creates more problems than it solves. Yet often times an attorney may suggest that you list your trust as the beneficiary of your IRA. Why is that?

Well, with all due respect to attorneys, our view of wealth management is that it entails investment planning, tax planning, insurance planning, estate planning, and any area that may impact an individual’s financial life. In most cases, each professional has a high degree of expertise in their area, but not necessarily in the areas that are outside of their lane. Not all attorneys are experts in the IRA distribution rules and what the tax impact would be. As a result, it is crucial that the various professionals you work with in each area of expertise communicate with each other about your personal goals. A good financial planner will help organize a strategy to identify needs in the various categories referenced and help facilitate communication with each professional.

Filed under: Articles

Comments: Comments Off on Using a Trust as an IRA Beneficiary: Does it Make Sense?

The home purchase is one of the biggest investments the average American will make. Real estate can be expensive and comes with carrying costs to maintain a property. However, many real estate investors over the years have invested in secondary properties for either personal use, such as a vacation home, or solely as an investment property. In many cases, these investors have seen significant price appreciation in these properties. When it comes to selling a piece of real estate, the tax code is different between your primary residence and a secondary property.

Primary Residence

When selling your home, the calculation as to whether or not you owe taxes is based on the capital gain, after you exclude the first $250,000 per person ($500,000 for a couple). Imagine you paid $200,000 some years ago for your home, and yet today it sells for $1,000,000. In order to determine your tax liability, you first need to figure out what you spent on the home in capital improvements, such as new windows, new roof, new driveway, or kitchen and bathroom renovations. These are common examples of what homeowners spend money on to improve and maintain their home. Those costs get added to the original purchase price, and then you have an additional $250,000 per person exemption. As an example, the tax calculation for a married couple would look like this:

$200,000 – Purchase price

+$200,000 – Possible capital improvements

+$500,000 – Exclusion for a joint filer

=$900,000 – Total amount excluded from capital gains tax.

If the property sells for $1,000,000 – $900,000 exemption = a taxable amount of $100,000 subject to capital gains.

Secondary Property

When selling a property that is not your primary residence, you can still add in your capital improvements to the cost, However, there is no $250,000/$500,000 exemption. One of the other ways to reduce the cost is by applying capital losses against your real estate gains. As an example, if you lost money on a stock trade, that loss can reduce the amount of gain on the sale dollar for dollar. But what can you do if you don’t have any capital losses to use, and you still have a big taxable gain on the sale of the property?

Under the tax code there is an option known as a 1031 exchange that permits the transfer of one property into another property via a qualified intermediary without realizing a capital gain and continuing to defer the tax liability. The timing of the exchange is a challenge, as an investor has only 45 days to identify the next property and 180 days to close on the new property. Unfortunately, the IRS rules on direct 1031 exchanges have become more stringent and difficult to execute in a timely manner.

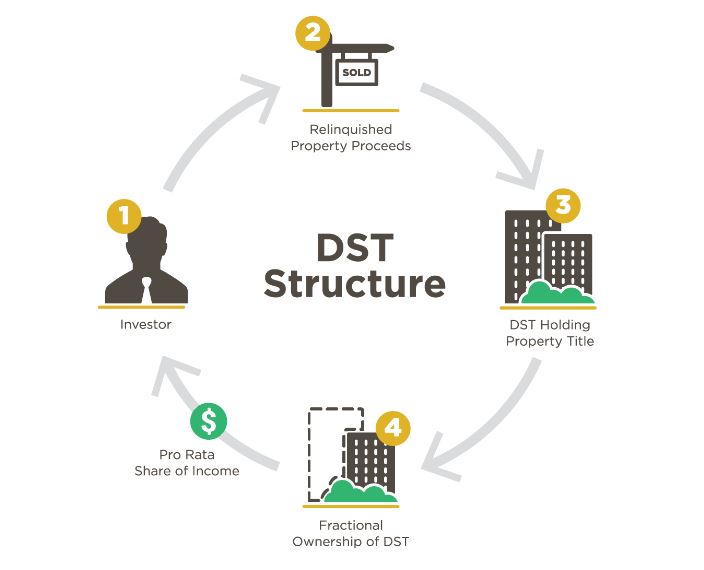

One of the other options is something called a Delaware Statutory Trust (DST). The DST was created in the late 1980’s as a special business trust to create a legally secure and clearly defined trust entity that establishes legal separation between the trust and its beneficiaries. Since the DST is a separate legal entity from its beneficiaries, creditors cannot seize or possess any assets held under trust.

DSTs are typically formed by real estate companies called sponsors, who purchase real estate assets that are placed under trust using their own funds. The DST sponsors then engage a registered broker-dealer to offer fractional shares of the trust, and individual investors purchase fractional shares of the DST. This process is another form of a 1031 exchange. However, as the individual investor, you are not required to seek out one or more properties on your own, as they are already part of what is typically a diversified real estate portfolio.

A DST may hold a series of properties related to commercial office buildings, multifamily apartment complexes, retail centers, industrial facilities, self-storage facilities, data centers or even medical facilities.

Once assets have been exchanged into the DST the investor has successfully deferred the tax liability on the gain and will now receive an income from the DST monthly that is typically in the area of 5%-9%. This income is representative of the investors’ proportionate share of the cash flow generated by the properties held in the DST after expenses. The capital gain is deferred until the investor chooses to sell the DST position, at which time they would incur the gain, as well as any gain on the property held in the DST. If the investor passes away while still invested in the DST, the assets receive the traditional step-up in basis, as with most other investments, and their heirs pay no taxes on the gains.

DSTs do not file a tax return as a trust, so as a result the investor receives their annual income at ordinary income tax rates as opposed to trust tax rates, which are less favorable.

The major benefits of the DST are:

Tax deferral

Cash flow

Instant real estate diversification

Passive approach to real estate investing

The potential drawbacks of the DST are:

There is limited liquidity

The real estate in the trust can still decline in value

Minimum investment to access

A DST may be a good option for investors sitting in a sizeable real estate position with significant capital gains. If you are concerned with generating a cash flow from the sale, don’t want to pay the taxes, and have no need for liquidity from the principal, a DST can be a possible option.

It’s important to understand that a DST is managed much like any other private Real Estate Investment Trust. As a result, it’s important to have a reputable sponsor with a successful track record of selecting and managing properties.

Filed under: Articles

Comments: Comments Off on Delaware Statutory Trust 101: How They Work

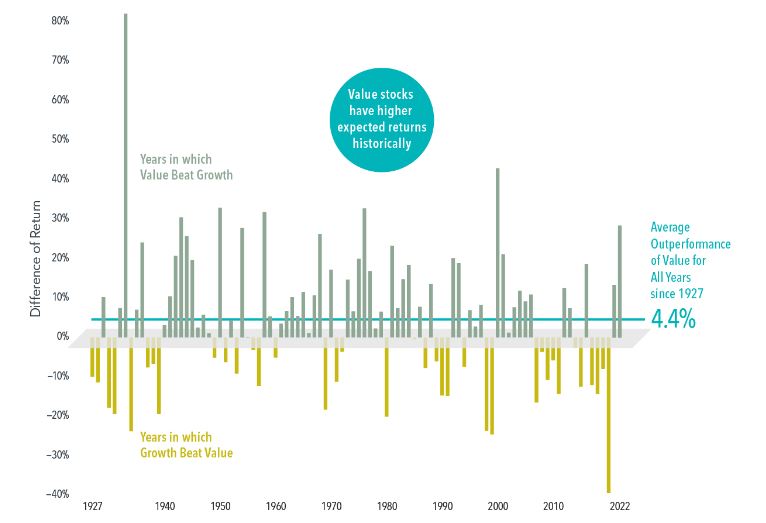

In the decade ending in 2021, the Russell Growth 1000 Index doubled the performance of the Russell 1000 Value Index. That partially reversed in 2022 when the Russell Value outperformed the Russell Growth by 22%. Then in 2023, the Russell Growth index once again outperformed the Russell Value Index by 23%, negating the outperformance of the value index in 2022. This unusually large divergence has made growth versus value a popular discussion topic.

In 1934 Benjamin Graham, a British born financial analyst wrote “Security Analysis”. Graham is often thought of as the founder of value investing, as well as laying the groundwork for index funds. Graham suggested paying such a low price for a stock that if you were only partially correct you weren’t likely to lose much money. He believed a business value was closely tied to book value, which was a relatively stable number. However, stocks generally correlate more to earnings than book value, making them more volatile. Graham believed that investors could purchase depressed shares when earnings were low and then wait for better times when the price would climb back to book value. Essentially, value investing is simply buying at a discount.

Graham once said, “The intelligent investor is a realist who sells to optimists and buys from pessimists.”

Growth investors often pay little attention to book value, instead looking for growing earnings. Companies with above-average earnings growth tend to sell at high price-to-book ratios. Investors often think of value investing as cheap stocks that didn’t grow very much, and growth stocks as high-growth businesses that were very expensive. Growth investors believe they owned “exciting” businesses poised to outperform the market, while value investors expect to outperform because their “boring” stocks usually made more money.

The chart above provided by Dimensional Fund Advisors demonstrates that since 1927 value investing has outperformed growth by about 4.4% annually. However, this isn’t true in recent history.

What we can see from this chart is that since 2014, growth investing has dominated value investing as we referenced earlier. However, investing is typically counterintuitive to the instincts of the average investor. The greatest opportunity is usually found in that which has been out of favor. We are very much of the belief that there is always a reversion to the statistical mean. Whether or not we are about to see that reversion now is unknown. If there is a reversion, and value investing once again is the more favorable place to be, how long will it last? The reality is that nobody can time this with any degree of precision anymore than we can time markets in general. What we do believe is that rather than trying to pick the precise time to change a portfolio, an equal degree of exposure to both value and growth is the more ideal approach.

Filed under: Articles

Comments: Comments Off on The Value vs Growth Rotation: When Will it Happen?

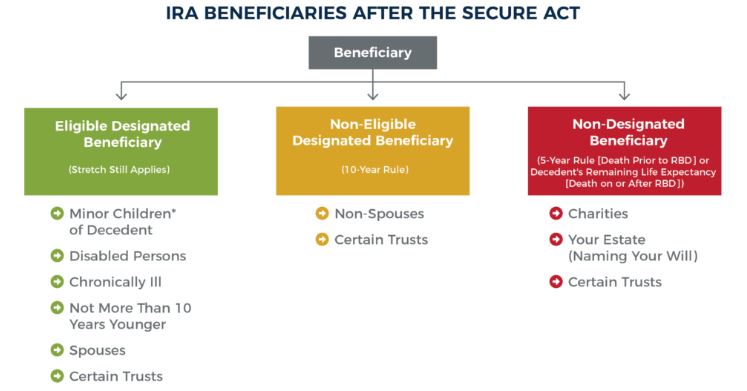

After many years of confusion, the IRS has finally clarified the rules around Inherited IRA’s. Under the old rules when a non-spouse inherited an IRA, the beneficiary was required to take a distribution every year based upon their life expectancy. As a result of the SECURE ACT 1.0, which took effect in 2020, several rules for retirement accounts changed. Among these were changing the required distribution age, establishing categories of beneficiaries such as an eligibledesignated beneficiary and non-eligible beneficiary, and changing the length of time required to deplete an account via required distributions.

Originally, Inherited IRAs were subject to a mandatory distribution based upon the life expectancy of the Inheritor. Secure Act 1.0 changed the distribution rules for non-eligible designatedbeneficiaries from a life expectancy withdrawal to having to withdraw the entire IRA balance by the 10th year after the passing of the original account holder. Non-eligible designated beneficiaries are most non-spouse beneficiaries, and some see through trusts.

An eligible designated beneficiary is a surviving spouse, a disabled or chronically ill person, person’s less than 10 years younger than the decedent, minor children and some see through trusts. Eligible designated beneficiaries have the option to stretch the IRA distribution over their lifetimes. The exception is when a minor child attains the age of majority, at which time the distribution schedule switches to the same 10-year rule.

The area under the new rules that left some ambiguity was whether a non-eligible designatedbeneficiary had to take at least some portion of the distribution annually. Over the last few years, the IRS waived the required distribution for non-eligible designated beneficiaries even when the decedent had already reached their required minimum distribution age prior to passing away. Whether the decedent had already begun taking their required distribution or not, the IRA account still needed to be withdrawn by the tenth year after the passing of the decedent.

The IRS finally clarified the rule, whereby a non-eligible designated beneficiary subject to the ten-year rule must take a required distribution each year. The account must be fully withdrawn by the end of the tenth year. This is true regardless of whether or not the decedent had reached the age of required distributions prior to passing away. What still has not been clarified is the amount of the annual distribution each year. While you must take withdrawals in each of the 10-years following the passing of the decedent, is there a minimum annual amount? At this point, that remains somewhat a question. It seems that they are implying that a minimum distribution each year must be taken equal to the life expectancy tables of the beneficiary. However, if only the minimum life expectancy withdrawal is met in the first 9 years, that would leave a sizeable lump sum in the 10th year.

As a result, some financial planning is still required, as you might have to take a rather large distribution in the 10th year if you haven’t taken relatively equitable withdrawals in the first 9 years. In many cases it may be wise to take distributions equally that are close to 1/10th of the account balance per year in order to spread out the tax liability until further clarity on the rules exists. To avoid an adverse taxable event, it would be prudent to plan so that you’re not surprised by a rather large tax bill in a single year. As always, talk with your tax advisor or financial professional to determine the best course of action.

It is also important to note, these rules do not take effect until January 1st of 2025.

Filed under: Articles

Comments: Comments Off on Inherited IRA Beneficiary Rules Clarified