The real estate market can be a great investment opportunity for the average investor, if the timing is right. Real estate, like any asset class, is cyclical in its behavior. This can present short-term as well as long-term opportunities. Many investors have opted to buy individual properties as their primary residences as well as for vacation homes. These investors may purchase with the intent of renting one or both of these properties in order to generate cash flow.

Whether the discussion is regarding a residential or vacation property, becoming a landlord can be accompanied by a number of headaches. Not all property owners are interested in getting a call that there is a plumbing problem which will require the immediate presence of a professional. In regard to vacation homes, few investors will be able to fix it themselves, due to proximity as well as experience and ability. This type of overhead can create expenses both in terms of capital as well as time, and should be considered when looking at any investment. Additionally, due to the higher overall initial minimum investment and the difficulty in obtaining financing…many potential investors are priced out of the market.

REITs

There may be an easier way. Real Estate Investment Trusts (REITs) present the opportunity for individual investors to add real estate exposure to their investment portfolio. This is possible without the time and commitment required in making a direct purchase of an individual property. REITs are securities that typically trade like a stock on an exchange that individual investors can purchase into at any time. REITs are organized in the form of a Unit Investment Trust and can be broken down into two core categories:

Equity REITs

An equity REIT will purchase and own individual properties which will generate cash flow via rentals which eventually pass thru to the shareholders in the form of a dividend. Additionally, the ownership of an equity REIT provides the shareholder the opportunity for capital appreciation in the value of the underlying real estate which may eventually be sold for a profit. Some equity REITs may have a specific concentration in certain areas of the market such as hospitality properties or shopping malls, while others can be extremely diverse in their underlying property holdings.

Mortgage REITs

A mortgage REIT is an investment which owns the underlying mortgages of the real estate owners. Rather than owning equity in a property, the mortgage REIT shareholder is a creditor of the property owner. The REIT effectively holds the note on the property the same way a bank would hold the mortgage note on a home. Because the mortgage REIT market is more of a fixed income investment, it will typically be accompanied by higher dividend payments and less opportunity for capital appreciation.

Special Tax Treatment

The dividend income received by a REIT is typically taxed as ordinary income and will be taxed at the shareholders top marginal tax rate. The advantage is that unlike the stock of an individual company which must pay tax first at the corporate level and then again at the individual level, REIT investors will only pay the tax at the individual level. The reduced layer of taxation often means a higher return to the shareholder. Additionally, a portion of the dividend payment received by the shareholder can be deemed a Return of Capital to the shareholder. This means that this portion of the payment is treated as tax-free while deferring the capital gain on the underlying assets further into the future.

Diversity

While a REIT will typically hold multiple properties in the trust, some investors may seek greater diversity. As a result, a group of REITs may be purchased as mutual funds, or exchange traded funds (ETFs) for a lower cost passive approach to investing.

What’s most important to note, is that real estate is just one of many asset classes that make up a more complete portfolio for a longer term investment strategy. However, regardless of an individual’s personal views on short term investment opportunities currently available in the real estate market, the REIT marketplace can fill the void for the average investor as a simplified solution with added tax benefits that will allow for diversified participation.

Additionally, REITs have shown an overall lower correlation to traditional equity benchmarks like the S&P 500. Today, as opposed to past decades, REITs exist in these traditional benchmarks. However, they only comprise about 2% of the S&P 500, the risk of redundancy is minimal and they can offer greater portfolio diversification.

Filed under: Articles

Comments: Comments Off on REITs: The Basics Of Real Estate Investment Trusts

Retirement savings options have expanded dramatically over the last four decades. Defined contribution plans such as 401ks have progressively become the primary source of private sector savings since the early 1980s. Unfortunately, for those in a higher income range, annual dollar value caps associated with contributions are imposed. In 2014, the maximum annual salary deferral for an employee is $17,500.00 ($23,000.00 if over age 50). One alternative solution to help mitigate current tax liability is the use of the Non-Qualified Deferred Compensation Plan (NQDC).

An NQDC plan can be established by a small business owner or by a large Fortune 500 company, and falls outside the regulatory scope of the Employee Retirement Income Security Act (ERISA). Under an NQDC plan, contributions made to the plan by an employee are deferred income, which may include salary, bonus and commissions. These contributions can be as much as 50% of an individual’s compensation. In making the salary deferral contribution, the employee reduces his or her adjusted gross income (AGI). This not only lowers taxable wages, but also may reduce an individual’s exposure to the Alternative Minimum Tax (AMT). Reducing AMT exposure may create additional tax benefits such as increasing the availability of itemized deductions like mortgage interest and property taxes.

These plans are typically either account based or non-account based plans. Contributions to account based plans may be met with a company match, and earn a fixed or variable interest rate. Some plans will opt to offer various investment options not unlike a 401k plan. Under a non-account based plan, the benefits function similar to a defined benefit plan…which is similar to a pension plan that provides an annual lifetime income at the commencement of benefits.

In the case of a small business owner, due to the greater flexibility of plan participation resulting from operating outside of ERISA laws, plans can be offered only to key employees. This can greatly reduce the administrative and funding costs, while offering significant tax advantages to the business owner. However, since the plan is not income to the employee, the plan does not become a deduction for the business until benefits commence. Due to the lack of an immediate tax benefit to the employer, many of these plans are unfunded future obligations.

While there can be substantial immediate tax benefits to an employee contributing dollars to a NQDC plan, there are inherent disadvantages. Among those disadvantages would be that the plan is a liability of the corporation and subject to the general creditors of the company. This is in contrast to a qualified plan in which vested plan assets belong exclusively to the employee. As a result of this liability, some employers have purchased insurance to help cover the liabilities of the plan should a company be liquidated. However, this benefit is the same as that of a general creditor and does not guarantee that the insurance will be sufficient to meet the unfunded liability. So when an employee opts to contribute deferred income, they should seriously consider the long term fiscal health of their employer. This becomes difficult for a younger employee who may be affiliated with a prosperous company, but couldn’t possibly forecast the fiscal health of an organization in 20 years with any certainty. It is possible that some or all of your salary deferral saved over many years could be confiscated by creditors of the company.

Some plans are established as funded plans, such as a Rabbi Trust. Under this type of trust, the plan assets are segregated in a separate trust for the purpose of satisfying future plan benefits. Ordinarily, this would make the income taxable to the employee, however, the IRS allows this as a funded NQDC plan, presuming that the trust is subject to substantial risk of forfeiture by including the trust as an asset that can be claimed by the general creditors of the corporation.

Another issue to be concerned with as a possible participant in a NQDC plan is that of the timing of distributions. NQDC plans are not eligible to be rolled into an IRA/401k or any other qualified plan at retirement or separation from service. This lack of portability means more restrictions on benefit distributions. These restrictions have been increased substantially since 2005. These rules were designed to prevent key employees from accelerating benefits and liquidating plan assets in advance of a financial liquidation of a company in fiscal trouble. Any failure to comply with these rules would result in substantial IRS penalties. The rules restrict distributions to several categories. Among them are: separation from service, death, disability, fixed time frame and change in ownership of the company.

It is important as the employee to understand these restrictions. As an example, if the plan was designed to be paid out over a five year period following separation from service, this could become problematic if you just resigned your position in order to accept a better job with a higher salary at a new company. In theory, you may have deferred income for only a few years only to realize it long before retirement while still in a high/higher tax bracket. This would have totally negated the tax benefit. As such, it is important to consider these variables when determining whether or not you wish to participate in or create a NQDC plan. It is best to discuss this with both your financial and tax advisors to ensure proper planning and suitability.

Filed under: Articles

Comments: Comments Off on The Pros And Cons Of Non-qualified Deferred Compensation

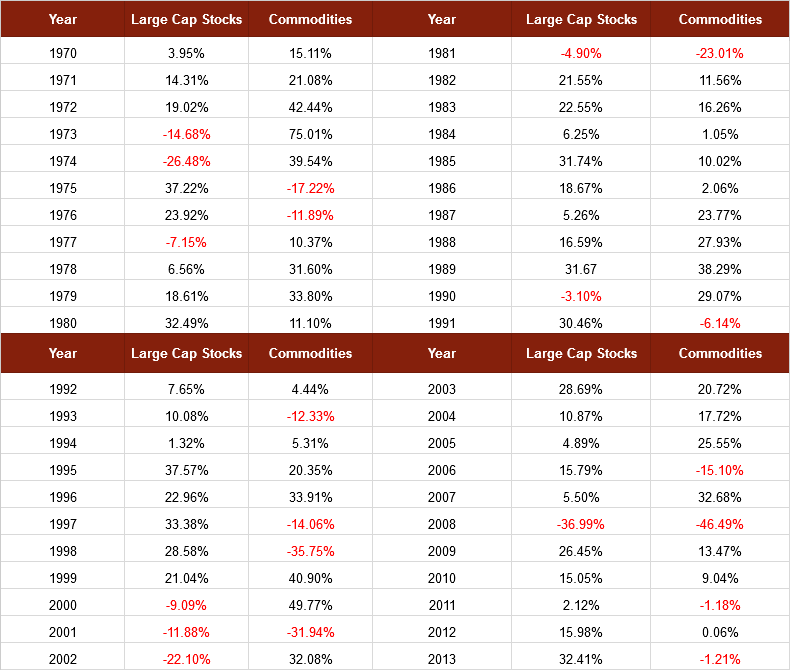

In the course of building a long term investment portfolio, the focus should be based on not just returns…but risk-adjusted returns. The premise behind a multi-asset portfolio is combining multiple asset classes in which each produces a positive long-term return, without being highly correlated. This can produce more consistent longer-term returns…while offering a lower overall degree of portfolio volatility. One of these asset classes is the commodities market.

Commodities independently have historically been more volatile than stocks with a higher standard deviation of returns over the last 40 plus years. Since 1970, US large cap equities have posted a standard deviation of 17.63 versus 24.29 in the GSCI commodity index. However, when combined as a component in an overall asset allocation…they can serve an important role. All too often investors chase after the most recent top performing assets. Using commodities as an example, the last five years have been less favorable as the US and most of the developed world has seen a somewhat anemic economic recovery from the 2008 recession. Yet, if we were to examine average returns of the broad based commodities market in comparison to the US large cap stock market, we find that the average returns are not much different. During the period of 1970 thru 2013…US large cap equities posted average annual returns of 10.41%, while commodities posted average annual returns of 9.21%.

What is important to note by looking at the following chart is the individual year-over-year returns. What we find is that in many years in which stocks suffered…commodities offered a cushion to portfolio returns. In many years the inverse was also true. During periods of extraordinary deflationary panics such as 1929 or 2008, asset classes often become highly correlated. However, we also find that in years like 2002 as the tech bubble had imploded and the US was recovering from the events of Sept 11th…commodities offered a substantial reduction in overall portfolio volatility.

It is also important to recognize that a proper investment asset allocation is defined by multiple asset classes and sub-asset classes of satellite investments to compliment core holdings like US large cap stocks. Commodity holdings are just one part of such a strategy. As a result of the high volatility that accompanies a broad basket of commodity holdings, investors should likely limit exposure in the commodities markets to a reasonable percentage of their portfolio. Investors who use the aid of a financial advisor should consult with them before incorporating new holdings into their longer term investment strategy.

Commodities as an asset class can be a bit more difficult to own outright. It is unadvisable for investors to trade in futures contracts around the commodity complex, unless this is something with which they have had significant experience. In most cases it is much more suitable to use a mutual fund or an ETF which diversifies across a broad range of futures contracts. Unfortunately, due to the structure of many commodity products in the ETF product space, they often report tax liabilities on a K-1 rather than a 1099. This is irrelevant for retirement accounts, and does not increase liability…but may delay income tax returns for non-retirement accounts, as K1’s tend to be issued later and often close to the tax deadline. In the event that an investor wishes to avoid the K1 filings, there are a number of open-ended traditional mutual funds that have broadly diversified commodity holdings. As in any mutual fund, expenses should be monitored in addition to portfolio holdings to ensure the fund achieves a truly diversified set of commodity holdings consistent with the benchmark.

Filed under: Articles

Comments: Comments Off on What Role Should Commodities Play In A Portfolio?

People can find themselves under a pile of debt for a variety of reasons. Sometimes we fall upon hard times due to a set of unfortunate circumstances beyond our control. Other times we may have simply lived irresponsibly for periods in our life and not given enough consideration to the long-term implications of our actions. Debt can come in many forms. While it’s easy to understand the importance of getting out of debt, sometimes we don’t prioritize how we eliminate these liabilities in the most effective way.

Home Loans

When eliminating debt it is important to consider not only the interest rate you are paying, but also the tax implications. Eliminating the primary mortgage on your home is typically a great idea that is easily accomplished with extra principal payments. Yet keep in mind that the interest paid on your primary residence is most often tax deductible. So making extra payments towards the home may not be the smartest first priority if you have other debts. In cases where one is subject to a substantial Alternative Minimum Tax (AMT) liability, this deduction, along with others, may be reduced or excluded, and the priority of which debts should be paid down first would have to be revisited.

In the case of home equity lines of credit (HELOC’s), the first 100k is usually deductible only if it were used for the purpose of home improvement. If you took out a home equity loan to pay off other debts, then the deductibility of the interest is depends on when the loan was issued and the loan-to-value ratio of the loan. Loans issued prior to Oct. 13, 1987 are subject to different criteria. If the funds were used for home improvement, then the limit on deductible interest is a collective total of $1 million ($500k for a single filer) in debt service in total taken against the home.

Deductions on a HELOC for a second home are more stringent. You can typically deduct the interest if you do not rent the property. If you do rent the property then you must live in it for at least 14 days per year, or 10% of the days you choose to rent it, whichever is the greater. The interest rates on many HELOCs are variable and therefore you should place a larger priority on this type of loan, when compared to the primary mortgage. While many variable-rate HELOC’s have limits on the number of interest rate increases per year, we are currently in a period of historically low interest rates, which means rates are almost certain to rise.

Auto Loans

In such a low interest rate environment someone with good credit can often negotiate very low financing rates on an auto loan, sometimes as low as 0%. However, for most individuals, auto purchases aren’t tax deductible. If you’re buried in debt, you may not have a great degree of flexibility or the best credit. In cases where there is sufficient equity in the home, debt consolidation through refinancing may be advisable to pay off auto loans by pulling the equity from the residence to lock in low rates. If it is a cash-out refinance, you may be transferring a non-deductible interest expense into a deductible interest expense. Most often an auto loan by itself is not enough to warrant a home refinancing opportunity, but it may be attractive in conjunction with other debt consolidation and lower available rates. People who are self-employed and have a car that is used exclusively for business purposes can deduct the cost of the auto as a business expense, as they can with other transportation expenses, including leased vehicles. If you opt to purchase a car, the tax benefit will be realized later. In such cases, this type of debt consolidation may not be advisable. As your company eventually grows and earnings increase, an auto lease will remain deductible and can be used to reduce business income. Yet home mortgage interest deductibility can be partially phased out should the alternative minimum tax begin with a higher adjusted gross income.

401k/Pension Loans

As important as it is to reduce debt over time, it should not be done at the expense and sacrifice of your retirement, with the exception of desperate circumstances. In fact, we should all target a minimum savings rate in our retirement plans of at least 10% of our income while employed. Your creditors will always be there, and the first rule of financial planning is “the first bill you pay is yourself.” Loans against retirement plans are not a good idea in general. They are designed to be a last resort in a desperate situation. However, if you have already taken one or are in need of one…they are often a better solution in an emergency than adding to credit card debt. Although the interest on a 401k loan is not deductible, you are paying that interest to yourself…not to a financial institution. The interest rate is typically fixed, and the loans are most often five years in duration, although they can be ten years if it is for a first-time home purchase. The true cost is the time that the principal from the plan is not invested towards your retirement. Additionally, should you default on the loan, your credit would not be impaired since you borrowed from yourself. However, you would be subject to ordinary income tax rates on any amount not repaid. Additionally, if you are below the minimum retirement age of 55, you would be subject to an additional 10% penalty on the amount not repaid.

Credit Cards

The most dangerous of all debt to create is credit-card debt. The reason is the extreme interest rates that are frequently charged on credit card borrowings. While credit cards often offer wonderful rewards programs, it is important to pay them off immediately. They can go a long way towards establishing credit for those who cover their expenses at the end of the monthly billing cycle, but if you spend beyond your means, you may find yourself paying financing charges in excess of 20 or even 25% annually…with no tax deduction available. This is generally the first place you want to begin to reduce debt if you are already in over your head. In some cases, it may be advantageous to consolidate debt into your home mentioned above. Sometimes there are promotional opportunities to consolidate credit cards into another card that offers you a 0% percent interest rate for a period of time. While this may not be a bad idea in the short term, continuously opening new cards for balance transfers will negatively impact your credit.

School Loans

Assuming you are reaping the rewards of a useful education, this may be debt well worth creating. The tax benefits of student loan interest can make prepaying such loans lower on the priority scale when compared to reducing things like credit card liability. The rates are typically much lower, and the interest is often a reduction to your adjusted gross income. Those individuals who are responsible with credit cards can often use programs like the UPROMISE program in New York. Such programs offer the ability for the points accumulated on credit cards to be applied to paying down principal on student loans.

While there are various forms of debt that one can find themselves in, it is important to prioritize the extra payments or cash flow towards the most logical areas. When doing so, you want to look at both the interest rate paid as well as the after-tax interest rate paid on deductible loans. Even when an individual has the cash available, it should be weighed against what that cash would earn if not used for debt reduction. Consulting with your tax advisor on your tax status in connection to these issues can be helpful. It is important to try to avoid bankruptcy proceedings. While a bankruptcy can alleviate some short-term issues, it will greatly impair your credit for years to come. Additionally, bankruptcy is about asset protection. If you are someone with no significant assets…it can be wasteful, time-consuming process.

Lastly, it is a good idea to take control of these issues on your own and educate yourself. There are numerous companies that advertise their ability to get you out of debt. Most of them time they are simply negotiating things like lowering the balance that a creditor is willing to accept. This is something you can easily do on your own without retaining costly debt-reduction services. Such negotiations, even when you are successful, can still impair your credit. For example, any unpaid balance owed on a credit card that is deemed settled by creditors is taxable income to you in that year.

It’s always advisable to live responsibly and avoid these issues. Yet, if you find yourself in a situation with a sizeable debt burden, be sure to prioritize the liabilities as discussed above. Itemize a budget by essential and discretionary spending so you can properly categorize what can be reduced or eliminated monthly. Sit down and put a plan of attack to paper, and follow it the best you can. Debt comes from many sources…and sometimes due to circumstances beyond our control. When we prioritize how we eliminate debt…like all financial decisions, weigh the entirety of the circumstance and alternatives.

Filed under: Articles

Comments: Comments Off on Things To Consider When Prioritizing Your Debts

In 1980 an amendment to the Investment Company Act of 1940 permitted publicly traded investment companies to register as Business Development Companies (BDC). BDCs are similar to Private Equity Companies and Venture Capital funds in that they invest in startup entities as well as established small and mid-sized businesses. The key difference with a BDC is they allow average investors to make investments that have historically only been available to very wealthy investors.

BDCs are given preferential tax treatment and registered as pass-thru entities similar to REITs, allowing them to avoid double taxation. In order to qualify as a BDC, the company must pass on 90% of its taxable income to shareholders as dividends, although most pass thru nearly 98% to avoid any form of corporate tax. As a result of this incentive, the average dividend rate across the publicly traded BDC market is in excess of 7% annually.

BDC’s primarily serve as a financing resource for privately held small and mid-size companies. They offer debt financing and often take a partial equity stake in the company. They may even serve in a consultative role in the management of the company, not unlike a private equity firm. BDCs are typically structured similarly to closed end funds where investors exchange shares on an exchange with each other rather than directly with a fund manager. This allows the management team access to a permanent source of capital rather as opposed to having to constantly redeem shares back to shareholders every time they sell securities. Simultaneously this allows investors the liquidity to sell shares on an exchange with daily intra-day liquidity that does not disrupt the management team’s investment strategy.

There are numerous BDCs that have been trading on public exchanges for several decades with a high degree of success. Historically they have served as a component in several of the major market indices. Yet, a 2014 legislative change has required that market indices and mutual funds holding BDC’s report the internal cost of the management of the BDC as an additional expense calculated in the expense ratio of the index or actively managed mutual fund. In reality this is not an expense borne directly by the shareholder, and would be similar to a mutual fund holding stock in IBM and reporting that company’s operating expenses as part of the expense ratio of the fund. As a result of this accounting change, organizations like S&P opted to remove all BDCs from all of their U.S. indices. When interviewed about the decision, S&P made it clear that this was not a reflection on the investment benefits of BDCs…but rather that they simply grew tired of explaining why the internal expense ratios appeared to suddenly increase. Since these holdings made up a small percentage of the index itself, it was simply easier to remove the holdings than comply with the new accounting requirements.

BDCs still however may present a strong investment opportunity for a number of investors seeking higher dividends for cash flow. Yet it should be noted that BDCs are by nature volatile and should be only be placed in a portfolio with the expectation of considerable risk and allocated on a percentage basis accordingly. The cash flow is not the only component of a BDC that may appear attractive to an investor. The BDC marketplace has had an overall degree of volatility higher than that of the S&P 500 Index, yet has had correlated price movements with the S&P only approximately 0.80% of the time. Their failure to move in lockstep with the broad market may offer some benefits for a number of investment portfolios by reducing overall volatility. As a result of the recent legislative changes forcing BDCs out of most major market indices, both Wells Fargo and Van Eck Global have recently created ETFs that incorporate various BDCs into a diversified index fund designed to track the marketplace. While they are still subject to the same accounting requirements that artificially inflate the cost of the index, investors who wish to gain widespread diversified access may continue to do so. Alternatively, they can still buy various BDCs individually.

As with all investments, it is important to evaluate an investment in BDCs based not just on the merits of the holding…but also how it is likely to impact overall portfolio volatility and work in conjunction with the additional investments across a comprehensive investment strategy.

Filed under: Articles

Comments: Comments Off on Finding Opportunities To Invest In Business Development Companies

Many of us do not always recognize the potential danger of becoming permanently disabled. The U.S. Census says that you have about a 1 out of 5 chance of becoming disabled for at least some period of time. The average duration for a long term disability (LTD) is about a two-and-a-half-year absence from employment. Long Term Disability is a vital component in a financial plan to help mitigate that risk. It is also important to understand some of the basic features of long term disability insurance before purchasing a policy.

What is Long Term Disability Insurance?

This type of insurance is fairly basic to understand. LTD picks up where your short-term coverage ends. Short term coverage will typically cover you for a period of about 3-6 months. If you are deemed to be long term disabled, most policies will typically cover replacing up to 50-60% of your prior income, with certain limitations. While 60% seems like a substantial reduction in income and insufficient to maintain most people’s current lifestyle, it is certainly better than no income. Benefits, when approved from a LTD policy, will typically not be paid beyond the age of 65.

How do you buy Long-Term Disability Insurance?

One of the most common ways is through a group plan with your employer. In fact a large number of employers provide LTD insurance for free as benefit for their employees. In such cases, it may make sense to buy additional supplemental insurance policy to bring the replacement value of your income closer to 100%. The cost of LTD insurance as part of a group plan is, like most group policies, often less expensive than purchasing this coverage privately.

However, there are some serious considerations that you should think about before buying a policy as part of a group plan. One such consideration is qualifying for benefits. Assuming that you are legitimately disabled and file for benefits, this does not mean the insurance company will approve the claim. Unlike life insurance where death is not debatable, a disability can be, and often is, disputed. In an event where you end up in a dispute over eligibility with an insurance company, this can be a long exhausting process with an employer-provided plan. The reason is that group insurance is regulated under the Employee Retirement Income Savings Act (ERISA). If you feel you are not receiving the benefits that you are entitled to, you may wish you take legal action against the insurer. In such an event under a group plan, this is a matter of federal law. According to ERISA, before there can be a federal lawsuit you must first “exhaust all administrative remedies”. This means you have 180 days to appeal a denial and then the insurance company can wait another 90 days to respond. While this process plays out, you are potentially without income as you’re unable to work. Furthermore under ERISA, the insurance company has what is known as discretion to administer their own policies. This means you must be able to demonstrate that the insurer abused their discretion. Most attorneys with expertise in the field of disability claims will tell you that this is a fairly tough standard to meet.

After this whole process is played out, your last option is to file a federal lawsuit in United States District Court. But under ERISA, the laws do not work the way many might expect. The cases are ruled on by a judge, not a jury. Testimony by the disabled is typically NOT permitted. This can make it difficult for your attorney to make their case on your behalf. Rather the judge makes a decision based on briefings with the attorneys involved. All of this is a long, difficult, and cumbersome process to fight a denied claim. At a time when you are battling a disability, it is easy to imagine how hard it might be for you to be successful. Additionally, this can be quite a bit of added stress. Clearly not all claims for LTD are denied by insurers, however if you are purchasing LTD insurance through a group policy it is important to understand what the risks are should your claim get denied.

Should you purchase LTD insurance as an individual, you will almost certainly pay a higher premium for such coverage. However, should a claim get denied and you end up having to take legal action, you would end up in state court. In such a circumstance, the legal process is a much more favorable for the insured. Most attorneys who represent clients in such cases will tell you that they will have much more latitude to make a case on your behalf, and a greater chance of a successful appeal. When weighing the increased cost in premiums, you should consider the risk of a potential dispute.

Tax Benefits…Typically if you paid for the policy on an after-tax basis, when benefits are paid they would be paid to you tax free. In most cases the opposite is also true. If you paid for the benefits on a pre-tax basis you should expect the income to be taxable. Part of the reason for the taxation is that you are receiving income. Benefits could potentially be paid over years few years, or potentially up to the traditional retirement age. With most other forms of insurance, like auto or homeowners coverage, you are not receiving income, but rather replacing a loss, also referred to as “making you whole.” In fact, in most other insurance claims, you are still incurring some type of loss even after the benefit is paid since there is typically a deductible to be met.

In the field of financial planning, LTD insurance is a vital component of any insurance package. Anyone who is not already retired should own such coverage. It’s important to understand what your policy’s features and benefits are and what possible restrictions exist. You should check with your insurance agent or your employer’s benefits office to find out what coverage is available so you can make an educated decision about the best course of action. Additionally, it should be noted that there are additional resources for those who become long-term disabled. Those include Social Security Disability (SSDI), but it should be noted that applying for SSDI is another time-consuming process that typically requires you to be disabled for some time before you qualify and receive approval. Should you qualify for SSDI, you can be almost assured that your claim against a long-term disability policy will be approved. Yet the inverse is not always true. It has historically been more difficult to get an SSDI claim approved. Lastly, SSDI on its own is not likely to be enough to be a suitable income replacement. Should you receive approval for SSDI, the benefit will be coordinated with any accompanying LTD insurance coverage. The combined benefit amount cannot exceed your income prior to the disability.

LTD insurance is just one part of a complete financial plan. Yet, an important aspect that is all too often overlooked as many individuals presume they will not be affected. While a disability may be a lower probability event for many younger individuals, the risk of a fire destroying your home is also pretty remote, yet we all maintain homeowner’s coverage on our residences.

Filed under: Articles

Comments: Comments Off on A Guide To Understanding Long-term Disability Insurance

Employee stock purchase plans (ESPP) are a common benefit that many publicly traded companies offer to their employees as an additional savings option to supplement their other defined contribution plans. There can be a number of benefits associated with these plans, as well as some potential disadvantages.

Under a qualified ESPP, the employer permits the employee to defer some of their income, via payroll deductions, to purchase company stock, commonly at a discount to current market value. This discount is often as much as 15%. Most companies will permit you to use between one and 15% of your wages for the purchase of company stock. The price paid per share is usually based on an offering period. So as the funds are set aside during each period, the price is fluctuating each day. The actual purchase price will be at a discount based on the price at the beginning or end of the offering period. Some employers offer an option known as a “look back” which permits you to use the better of the two prices during the offering period.

While the income received from wages that were deferred towards the purchase of the stock is still subject to income tax, the bargain element…the discounted portion of the stock purchase is exempt from income taxes until liquidated, and not included as an AMT liability. Generally speaking, the tax is realized at the sale of the stock.

As an example, if you acquired $100 worth of company stock for $85 (a 15% discount), the $85 dollars you earned before the investment was taxed as ordinary income. The 15% discount, or $15 dollars, is not taxed until the shares are sold. If the shares rose to $150 and the shares were subsequently sold, the $15 would be taxed as compensation income and taxed at ordinary income tax rates. The gain from $100 to $150 would be treated as a long-term capital gain.

However, in the case of a qualified ESPP, in order to qualify for long-term capital gains treatment the stock must be sold in a “qualifying disposition.” This means that the shares must be held at least two years from the offering period and at least one year from the purchase period. If you liquidate the shares too soon, the sale is considered a disqualifying disposition and loses the favorable tax treatment. Additionally, the transfer of shares as a gift within the qualifying period is also classified as a disqualifying disposition…with the exception of shares transferred as a Qualified Domestic Relations Order as the result of a divorce.

In the case of a disqualified disposition, the gains from the discounted purchase price are treated as compensation income (ordinary income tax rates), while any capital gains from market appreciation are taxed at the capital gains rate. For example, the difference between the fair-market value at the time of the purchase and the actual purchase price is ordinary income, even if the stock declined and was sold for less than the purchase price. So if you purchased the stock for $85 while it was valued at $100, then subsequently sold it at $80 in a disqualified disposition, you would still be subject to the $15 (difference between the $85 discount and $100 market value) taxed as ordinary income.

Some of the obvious benefits of an ESPP, in addition to potential tax benefits, would the discounted purchase price, as well as the ability to automate a savings plan through payroll deduction. Yet, there are some potential downsides, because there is ordinary income tax treatment on at least the bargain element, that portion is subject to payroll taxes. But employers do not withhold payroll taxes on the bargain element for a qualified ESPP. So the employee will have to pay that tax at the time of disposition.

Another major consideration is the risk of stock concentration. It is never a good idea to concentrate too much of your wealth in any one individual security. Furthermore, while we would all like to assume our jobs are secure, that is not always the case. Considering that a good degree of your financial stability is based on your earning power, it is not always wise to concentrate too large a portion of your wealth in the same entity which you also depend on for your wages. In the event of the organization experiencing a turbulent period, you may be at risk of losing both your job and a substantial amount of savings simultaneously…as the company’s stock price may be highly correlated to the company’s ability to pay you. Even if you don’t see a substantial decline, it is not uncommon for these concentrations to present a tax problem later in life when you are trying to implement a more conservative strategy.

While using an ESPP plan that an employer offers may make sense to a certain degree, it should not be done at the expense of sacrificing contributions to more traditional retirement savings plans such as a 401k. These more traditional retirement plans offer more of an immediate tax benefit by reducing your adjusted gross income. They also offer a much greater degree of investment flexibility.

Filed under: Articles

Comments: Comments Off on A Guide To Understanding Employee Stock Purchase Plans

As a result of two major market panics in the last two decades, the use of variable annuities as a solution to the financial needs of the consumer has increased. These products have been marketed and re-marketed in various different formats with numerous bells and whistles. In some cases a variable annuity may make a great deal of sense. Many individuals who are young enough and in a higher income range may have already maximized their employer-driven tax shelters. With enough time on their side until retirement, the tax shelter of a variable annuity may provide substantial benefits. There are in fact a number of circumstances where such a long-term tax shelter may be advantageous. Tax sheltering dollars is the key to a deferred annuity. However, all too often variable annuities are marketed towards individual investors as a solution for 401ks and/or IRA’s because of the additional living benefits they offer, but those accounts are already tax-sheltered. So what is a living benefit really and do you need one?

What is a living benefit?

A living benefit is an insurance benefit that is connected to the account value of your funds. Historically, variable annuities offered a death benefit that would insure at least a portion of the value of your account for your heirs at death. Living benefits developed to offer coverage that can be applied in various ways. One way is the insurance of an income stream. For example: the insurance company may guarantee you a withdrawal rate on the funds in your IRA for the duration of your life. The percentage withdrawal rate would typically be based on the age at which you begin to draw a cash flow. So a 62 year old with $100,000 in an IRA who wished to supplement his or her income stream from that account could buy a variable annuity with a guaranteed withdrawal rate of 4% annually for the duration of his or her life, or $4,000 per year. Even if the portfolio were to decline to zero at some point in the future, the insurance company will continue to pay this 4% cash flow. While this might sound great to some…let’s take a closer look.

The first thing to look at is the 4% cash flow. The 4% in a guaranteed withdrawal benefit is typically NOT a guaranteed rate of return. It is simply the maximum amount of your own money that you are permitted to withdraw annually. The rate of return is dictated by the underlying investments which can go higher or lower on any given day, no different than any investment account. Since the insurance company is on the hook for the cash flow should your investments decline to zero, they typically put some constraints on the investment flexibility within the contract. They may for example mandate an allocation that has at least 70% stock-market exposure. Various studies in the financial planning field have taught us that someone who maintains an asset allocation of 60% equities and 40% in fixed income and draws 4% of their assets proportionately each year has an excellent chance of stretching their portfolio at least 30 years. For that same 62 year old, that brings you to age 92…past your statistical life expectancy. So as we can see, the insurance company is simply limiting your cash flow for you, and it is highly unlikely that they will ever have to pay you from their own funds.

Mortality & Expense Fees

Expenses are another major issue to consider when examining a variable annuity with living benefits. Every contract has what is a called a Mortality and Expense Fee (M&E Fee) which has to be paid each year. The average M&E fee is around 1.25% of the value of the contract although it can range as high as 2%. This is a separate and distinctly different fee than the mutual fund expenses that will also come out of your account. The first thing to note is that had you built your portfolio outside of the annuity contract with the exact same investments, you would have rate of return in excess of the annuity product offered by exactly the amount of the M&E fee. So if the contract guaranteed you the ability to draw 4% annually from your own account, which is highly probable anyway…the cost to get that 4% guarantee is that you must pay the insurance company 1.25% per year.

Another important component is what value the M&E fee is accessed upon. If your contract started at 100k, but then declined to 80k after several years of making withdrawals…the 1.25% may still be based upon the original investment. Some annuity contracts have been written in such a way that the M&E is based on either the original investment or any increase in value to the investments. However, if your account goes down due to a market decline, withdrawals or some combination thereof, you might be stuck paying 1.25% of 100k even though your account is only worth 80k. This makes many of these contracts much less attractive and substantially more expensive upon a closer look.

Fund Expenses

Fund expenses are another factor to consider. Once again are separate and distinctly differently than the M&E fees. While many investors wish to use mutual funds as a way to diversify a portfolio, they should pay close attention to the fees charged by various funds. Mutual funds in a retail account are sold in shares, while mutual funds in an annuity contract are sold in units. It is quite possible to have the same style fund with the same fund manager but see an entirely different expense ratio. In many cases, the fund offerings available in a variable annuity have substantially higher fees than what you would pay to buy the same fund or something similar in a regular retail investment account. More often than not, the annuity version is more costly by 1% or more.

Surrender Charges

Surrender charges are another substantial consideration. Because these contracts are designed to offer these benefits by pooling risk, they need to guarantee control of your assets for a period of time. So they commonly apply surrender periods that can mean you are prevented from closing or transferring your account for 5-7 years without paying a penalty. Depending on the contract, the surrender fee can be a substantial portion of your account value.

The term “annuity” refers to many different types of products. Some of them offer valuable benefits when applied properly in the right circumstances. Some companies offer some very low-cost versions of these contracts. However, investors should look very closely at the fine print before committing to any contract. In the case of living-benefit variable annuities, you could end up paying 3% or more of the account value in fees just to obtain a guaranteed cash flow of 4% to 5%. The word “guarantee” can sound very attractive to many investors, bet in the case of living benefits…more often than not, the guarantee isn’t really worth the cost.

Filed under: Articles

Comments: Comments Off on Buyer Beware: Living Benefit Annuities

Life insurance planning is a topic that is often very confusing for the average individual. There are various different types of insurance products available, and it is not always clear which solution is the most suitable for an individual to select. In order to make an educated decision, it is imperative to obtain at least a basic understanding of how life insurance products work and what form they are issued in. There are two basic forms of life insurance, term coverage and permanent coverage. While often times financial professionals will advocate convincingly for one or the other, neither is always correct.

Term Insurance is a type of coverage that is issued for a specific term, as the name would imply. Coverage will typically range from 10 to 30 years in duration. At the end of the policy period, the policy simply expires leaving you without any coverage and with no accumulated cash value. The premiums which are paid directly to the insurance company are substantially less than that of a similarly issued permanent insurance coverage.

Permanent Insurance itself comes in multiple forms. They are Variable, Universal and Whole Life policies. Each of these policies are designed to accumulate a cash-value component that can be viewed as an investment towards retirement, as well as a source of funds to pay for the policy premiums later in life. The policy premiums are typically significantly more than those for a term policy with an equal amount of corresponding insurance coverage.

The younger the age of the insured at issuance, the stronger the argument for term coverage will be. The principal behind this argument is that there is no need for life insurance unless you have a financial dependent. Insurance is a contract of indemnity. There is little reason to buy any life insurance if you are not married, have no children or any other dependents. However, it is imperative that a younger couple with minor children carry adequate insurance to care for their dependents. The cost of insurance has a much greater effect on their budget in their early years of accumulating wealth. In the event that they have excess cash flow above the cost of insurance premiums, the case for using life insurance as a savings mechanism is not very strong. More often than not, it will pay to redirect any additional cash flow towards increasing 401k or other employer-sponsored retirement-savings plan. If those features have been maximized, then other tax-sheltered savings options, such as an IRA or Roth IRA, should be explored. If an individual should pass away at a younger than traditional age, their dependents would inherit both the death benefit of the insurance policy as well as the the additional retirement savings.

As you get further on in years, there may be a number of circumstances when the benefit of a term-life policy is not as clear. In the case of an individual or couple who may still have dependents, a term policy may not offer a long enough coverage period. Term insurance most often does not extend past 80 years of age. In the event that a pension benefit stops with the death of a spouse, leaving the other spouse without a sufficient, permanent coverage should be considered. While ideally it would be preferable to use the extra cash flow to have money saved for such an event, this isn’t done and in many cases it is too late and the clock cannot be rewound. It is not uncommon for Americans to live into their 90’s today, what if the spouse with a pension benefit passes away at age 81, just after his term-insurance coverage expired. If the surviving spouse were to reach age 95, they would be forced to deal with a significant period of time in which they may not have a sufficient income. As you age, the amount of coverage needed to replace a pension declines as a person’s life expectancy shortens. In such a case, a permanent policy can be tailored with a decreasing death benefit as the years go by to keep policy premiums under control.

Small business planning is another area in which permanent insurance policies can be a benefit. When business partners enter into an agreement to form a partnership, it is fairly common to create what can be known as a Buy/Sell Agreement, or for multiple partners a Cross-Purchase Agreement. These are agreements in which two or more partners establish an agreement to buy out the other’s interest in the business upon death, disability or some other circumstance in which one party can no longer contribute to the business. In most cases, the surviving partners do not wish to bring their deceased partners heirs to the estate as a new partner. The insurance allows them the funding to buy out the deceased party’s interest from their beneficiaries. While term insurance can theoretically suffice for this need, in the case of an older partner who remains active, the limitation on time with a term policy can be problematic. Additionally, the economic value of the business entity may be growing, which requires additional insurance coverage over time. In order to avoid underwriting risks in future years, a universal policy can be structured with an increasing amount of insurance to compensate for this concern.

Tax benefits can often be cited as a reason to use permanent insurance. This is certainly true in the case of the minimization of estate taxes through what is known as an Irrevocable Life Insurance Trust. This is an estate-planning technique which typically requires insurance to continue in perpetuity. Considering the recent increases in the estate-tax thresholds, this technique has become much less common.

Another tax benefit is the ability to shelter money for the purpose of college planning and retain eligibility for financial aid by hiding money outside the view of FAFSA applications for federal student aid. This is not the most economical method to shelter money as insurance is much more expensive than other forms of tax shelters such as some low-expense versions of variable annuities that are issued without a sales charge by some prominent mutual-fund companies.

More recently, a number of hybrid-type life insurance products have been developed. One example is a term insurance policy that offers a convertibility feature to a permanent policy at the end of the term. This is extremely attractive to younger individuals. It permits you to buy 30 years of term coverage at only a nominally higher premium over traditional term, with the ability to convert it to permanent insurance if, for example, you should be diagnosed with a serious or terminal condition just before the end of the term. In the case of my example, such a diagnosis could make it difficult, if not impossible, to get a new policy. This convertibility allows the insured to continue the policy without evidence of insurability as a new permanent policy. The insured would be subject to the higher premiums associated with permanent insurance if they opted to convert, or they could simply let the term expire if there was no need for the additional coverage.

One of the more interesting new coverage options available for those approaching retirement is hybrid universal insurance coverage coupled with a long-term care policy. They can offer the ability to pay for a long-term care benefit, that if needed will simply be a draw against what would otherwise have been a death benefit. Most often these policies should be purchased for the LTC benefit itself, with the life insurance coverage being a secondary benefit to make sure the policy premiums are not simply wasted…which can be a concern with traditional long-term care policies. While this approach is more expensive than buying a traditional LTC policy, there is at least a guarantee of some form of a return on the insured’s money, whereas traditional LTC coverage can be very expensive that is never used and pays nothing back to the policy holder or their beneficiaries.

Ultimately, insurance planning, not unlike all forms of financial planning, is specific to the individual circumstance. There are no absolute product solutions which apply to us all. It is important to educate yourself on the topic before committing to a contract, because most insurance professionals are compensated on a commission basis. The more expensive product they sell you, the more money they will make. In some cases, the more expensive product may be necessary, but that is not always the case, and it is not the case in the majority of circumstances.

Filed under: Articles

Comments: Comments Off on Term Vs Permanent: Which Life Insurance Policy Is Right For You?

Charitable donations are something that Americans are inclined to do more so than citizens of virtually every nation on earth. This is in part a result of the fact that the US is the wealthiest nation on earth and has the largest per capita GDP of any of the large industrialized nations of the world. Being charitably inclined can mean volunteering one’s time or their financial resources. In the case of monetary contributions, charitable donations can offer some financial planning benefits that can impact an individual’s estate and tax planning in positive ways. In order to qualify for these benefits, the contribution must be made to a registered 501(c)(3) organization, which is a qualifying status the IRS gives to non-profit organizations.

One common benefit of donating to a charity is the tax deduction that can be used against an individual’s income-tax liability. In order to take the deduction you must itemize deductions on your IRS Form 1040 rather than take the standard deduction. However, there are limits to this deduction. As a general rule, you can deduct a donation of cash up to 50% of your Adjusted Gross Income (AGI). In the case of property, the limit is typically 30% of your AGI. In the case of a donation of stock, mutual funds or property, the amount donated will be based on the fair market value of the asset at the time of the contribution.

In some cases, the main motivating driver of the charitable contribution is not necessarily the immediate reduction in income tax liability, but rather the reduction in the size of an individual’s taxable estate. This is particularly common in the case of individuals who may have no direct heirs or have an estate large enough that they have little concern for the heirs being left in good financial condition upon their passing. Estate planning to limit the exposure to estate taxes has become substantially easier in recent years for the average American when evaluating their federal estate tax liability. The Applicable Exemption amount for 2014 is $5.34 million. Because of the new rules permitting portability, that is a joint credit of more than $10 million for a couple if an IRS 706 form is filed within nine months of the deceased’s passing. However, when looking at the individual state laws, the thresholds are not always so forgiving. As an example, in New York any estate in excess of $1 million will have an estate tax levied that can range as high as 16%. Additionally, portability rules which allow you to claim a credit for your deceased spouse’s Applicable Exemption do not apply in New York. Each state has their own tax law pertaining to estates and/or an inheritance.

Those individuals who are charitably inclined and would prefer to see their assets pass on to what they may deem to be a worthy cause rather than the state or federal government should consider a number of potential estate planning strategies. Among them would be a Charitable Remainder Trust. These types of trusts are drafted in more than one form.

One such form is called a Charitable Remainder Unit Trust (CRUT). Under this type of trust, the assets that are placed into the trust will eventually go to the eligible charitable organizations upon the termination of the trust, which is commonly the death of the grantor of the assets. The trust is then required to pay back to a non-charitable beneficiary (also commonly the grantor) a fixed percentage of the trust’s assets annually until it is terminated. The termination of the trust can be triggered by the death of the grantor or be based on a specific number of years. This is a technique that permits the grantor to continue to receive income from the trust while removing the principal assets from their taxable estate to later be paid to a charity. The payments are typically required to be between 5-50% of the trust’s assets.

Another strategy is the Charitable Remainder Annuity Trust (CRAT). This trust operates in a similar manner, but rather than pay back a fixed percentage of the trust assets annually, it makes a fixed-annuity payment of a specific dollar amount each year.

Yet another option is what is called a Net Income with Makeup Charitable Remainder Unit Trust (NIM-CRUT). In the case of the NIM-CRUT, the trust also pays a fixed percentage of the trust assets not to be less than 5% back to the stated income beneficiary. In the event that the trust assets generate less income in a given year than the stated minimum percentage of the trust payement, then the payment is made in the amount of the trust’s income. The reason for this is that a NIM-CRUT does not permit the trust to invade the principal value of the investments for the purpose paying the non-charitable beneficiary the annual income payments.

Another option available is a Charitable Pooled Income Fund. In the case of this type of charitable contribution, the grantor pools his or her donation with that of other investors. These types of funds are commonly created by large financial institutions who manage the assets for you, or directly by a charity themselves. The disadvantages are that the investment options are limited to those available in the fund and high minimum investments may be required. Additionally, while you may be saving on the expense of having to obtain an attorney to draft a trust for you, you will incur the annual expense of the financial institution managing the pooled income fund on your behalf with very limited investment options.

Another benefit associated with each of these strategies is that assets donated to any of these forms of charitable trusts will eliminate capital gains assessed on appreciated assets. Unlike a gift to a relative, friend or some other non-charitable organization, the capital gain will not be levied because the asset was donated in kind without having been sold until it was part of the trust. Since the charities which must be registered as 501(c)(4) non-profit organizations are the ultimate beneficiary of the donated assets, they are not subject to capital gains tax.

These are a few of the commonly used estate planning techniques that can help you minimize both their current and future tax liabilities, while still donating to a worthy cause of your choosing. Estate planning can be a very complex topic, and should be taken seriously. It is something that each individual should address with a competent estate planning attorney who is willing to work in conjunction with a tax advisor and a financial planner.

Filed under: Articles

Comments: Comments Off on Using Charitable Trusts For Tax And Estate Planning