Russell Investments: Global Market Outlook Q2 2024

Russel Investments: Global Market Outlook Q2 2024

Russel Investments: Global Market Outlook Q2 2024

Over the last decade much has been made of the cryptocurrency space, more specifically...

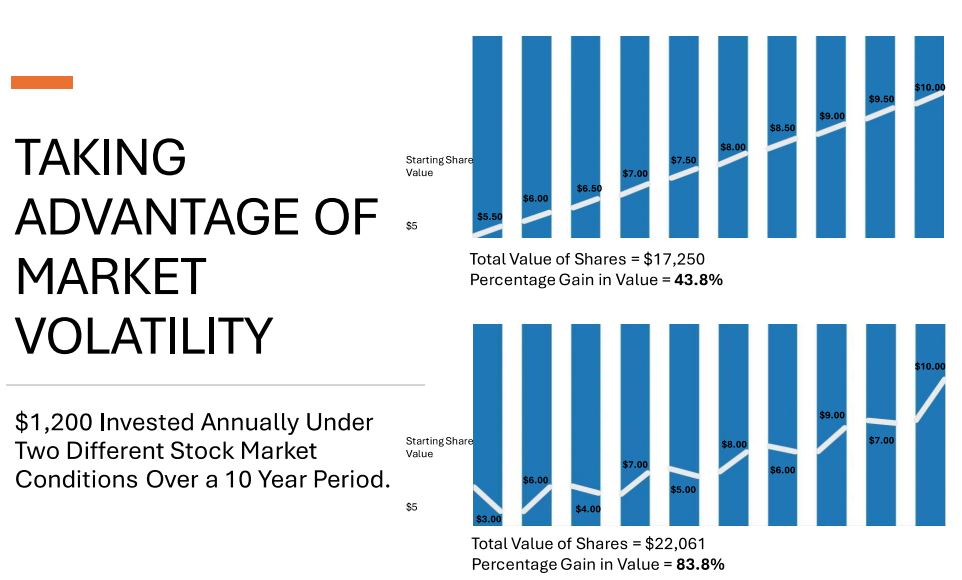

Market volatility is not something that investors enjoy, as none of us like to...

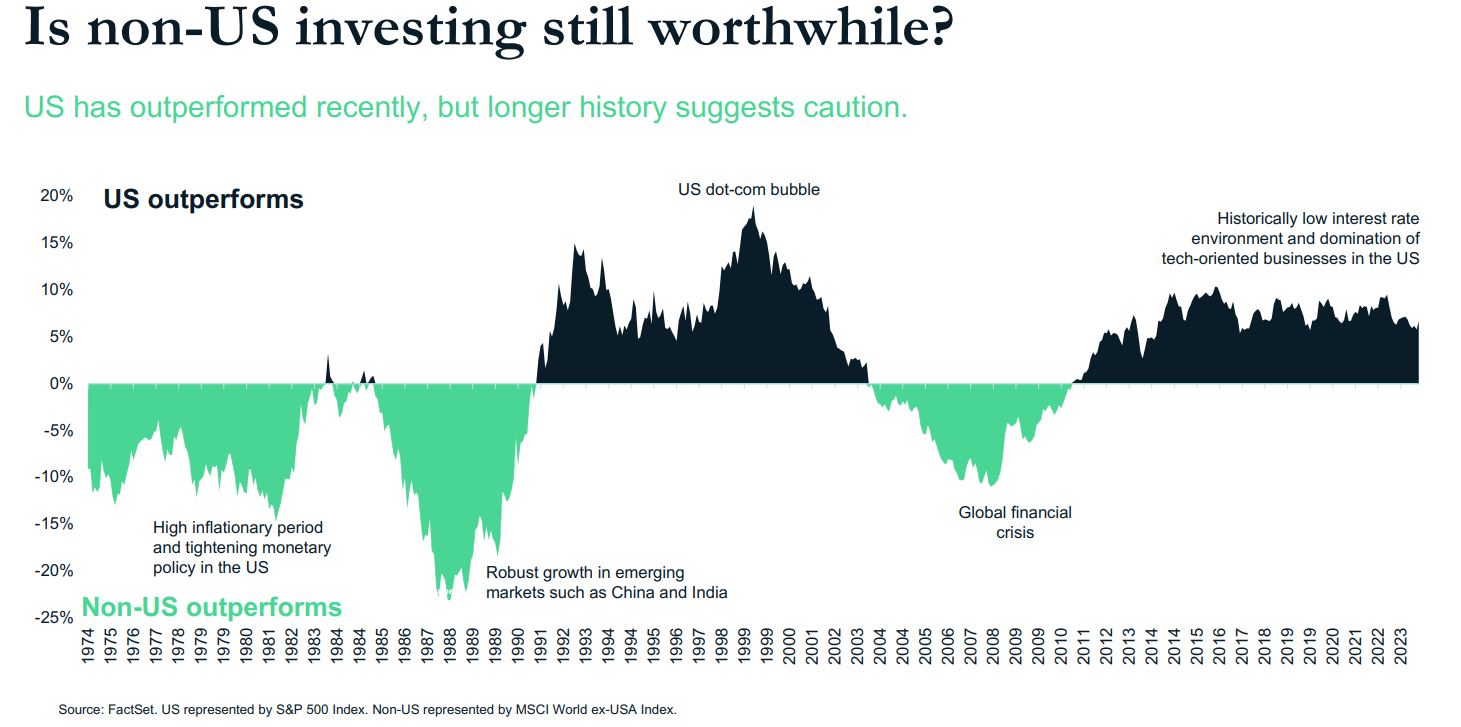

The importance of diversification has been well established across the investment research literature over...