The Bond Market: How Attractive is Fixed Income Today?

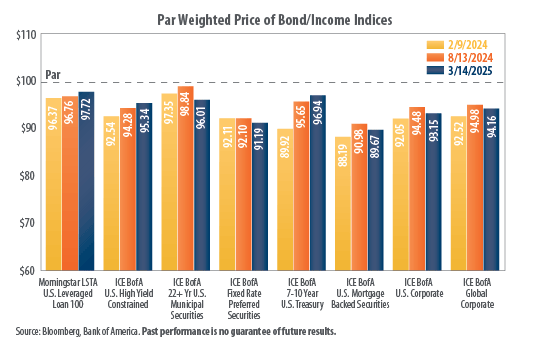

Looking at the bond market today, we can see that bond prices still haven’t...

Looking at the bond market today, we can see that bond prices still haven’t...

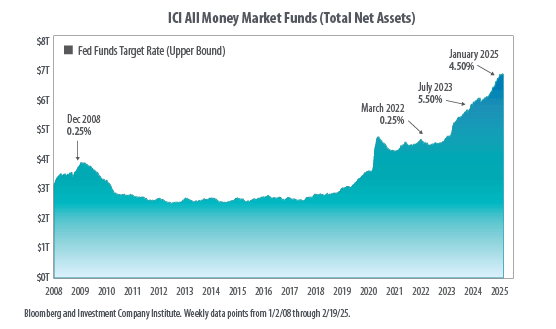

A review of money market balances has at times been looked at as a...

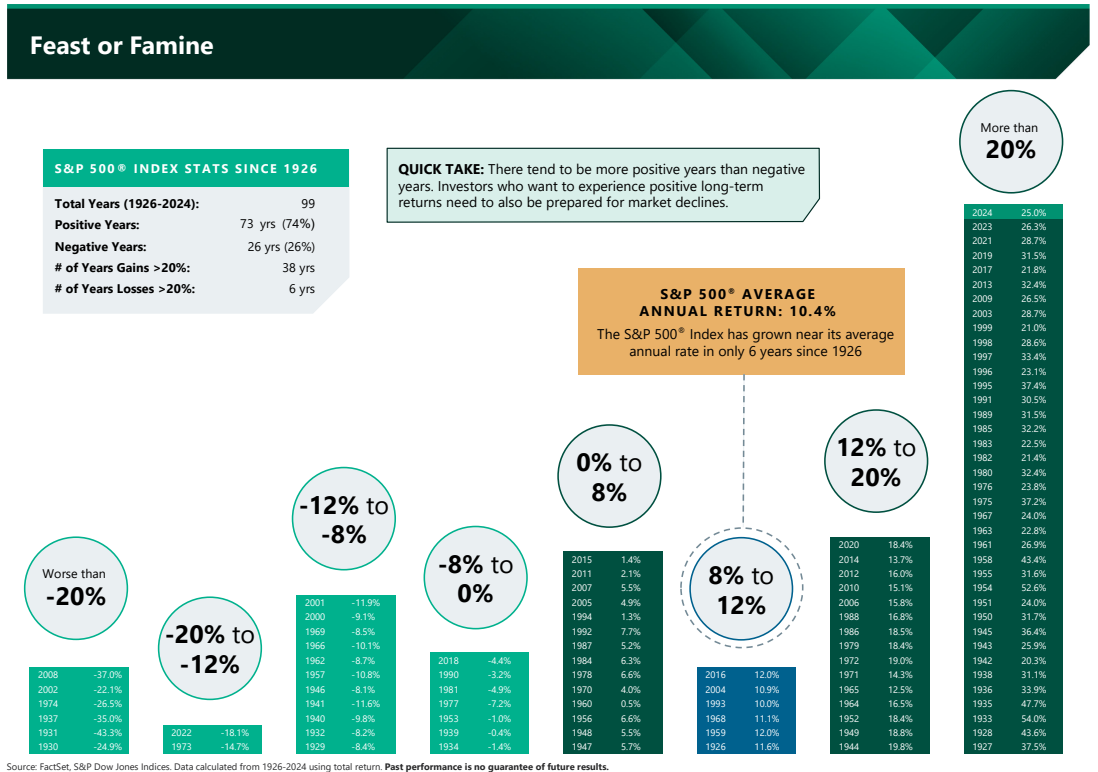

Investors often refer to the stock market as gambling, no different than that of...

Over the years we have referred to various sources to demonstrate data points on...