2025: Important Retirement Plan and Tax Law Changes

As the calendar turns to the new year, things rarely stay the same, and...

As the calendar turns to the new year, things rarely stay the same, and...

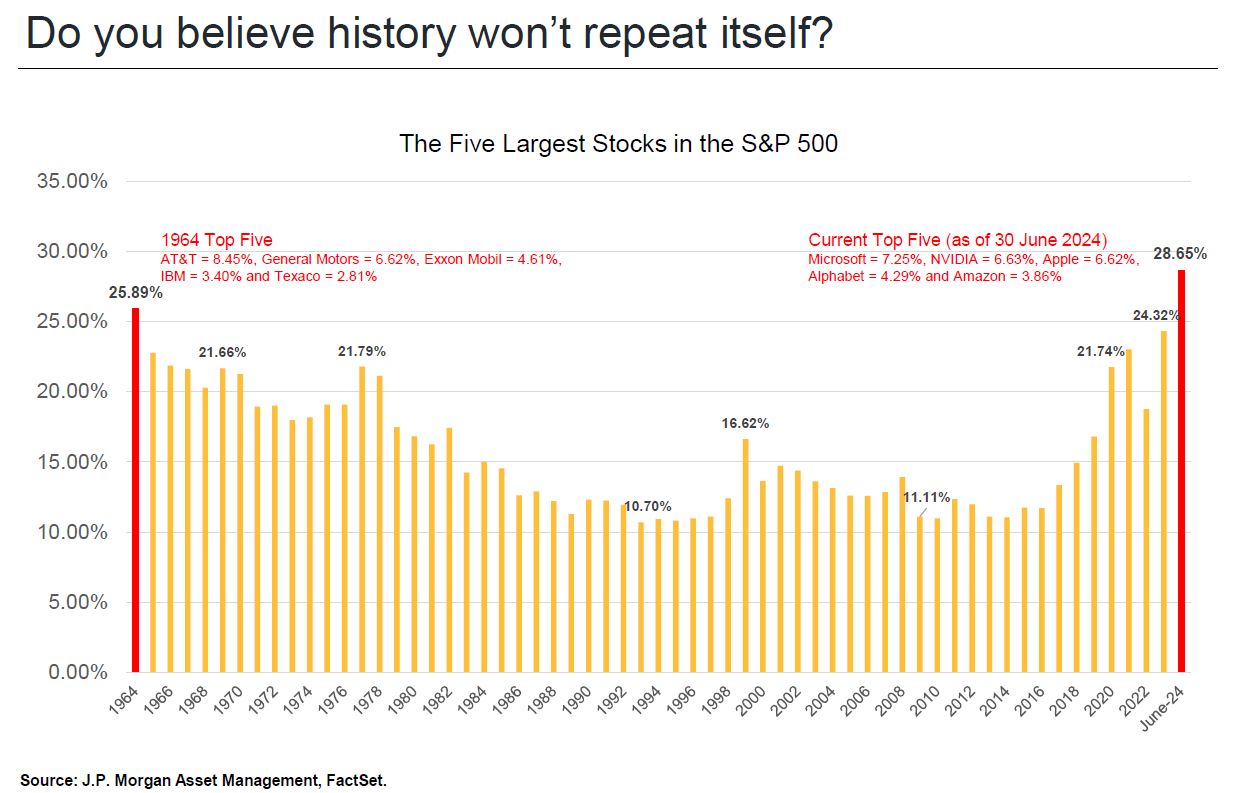

Most investors have heard of market indices such as the S&P 500 or the...