Using a Trust as an IRA Beneficiary: Does it Make Sense?

One of the more common estate planning mistakes we have seen over the years...

One of the more common estate planning mistakes we have seen over the years...

The home purchase is one of the biggest investments the average American will make. ...

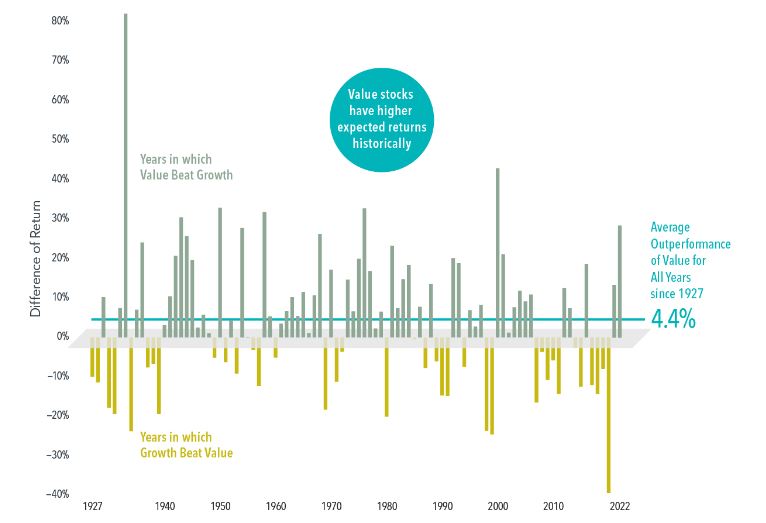

In the decade ending in 2021, the Russell Growth 1000 Index doubled the performance...