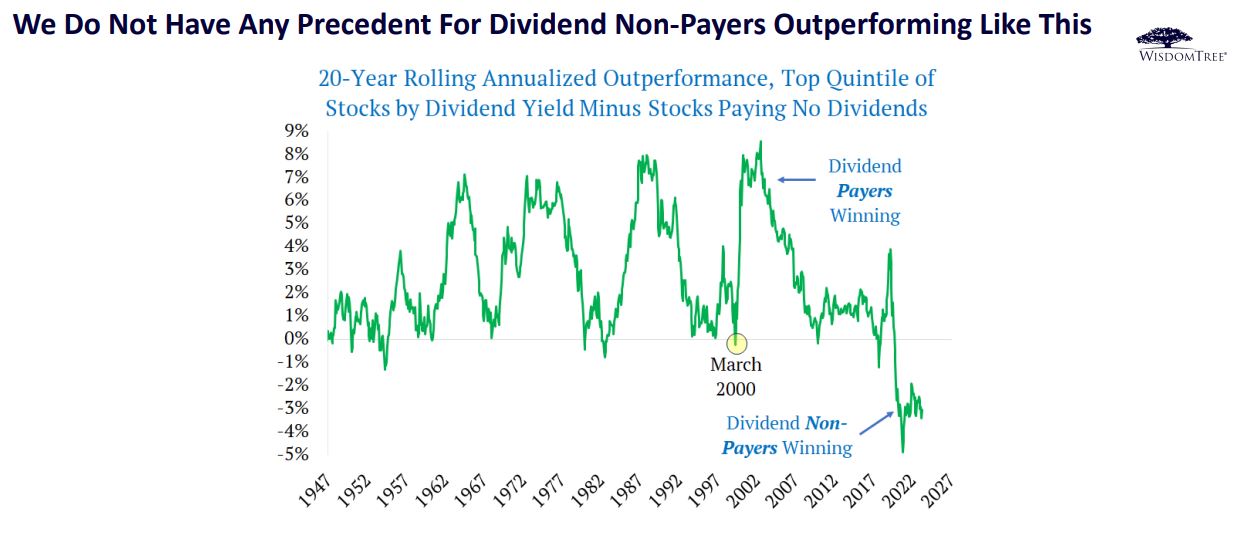

Do Dividend Payers Outperform?

In 2024, more than 75% of S&P 500 stocks pay a dividend of some...

In 2024, more than 75% of S&P 500 stocks pay a dividend of some...

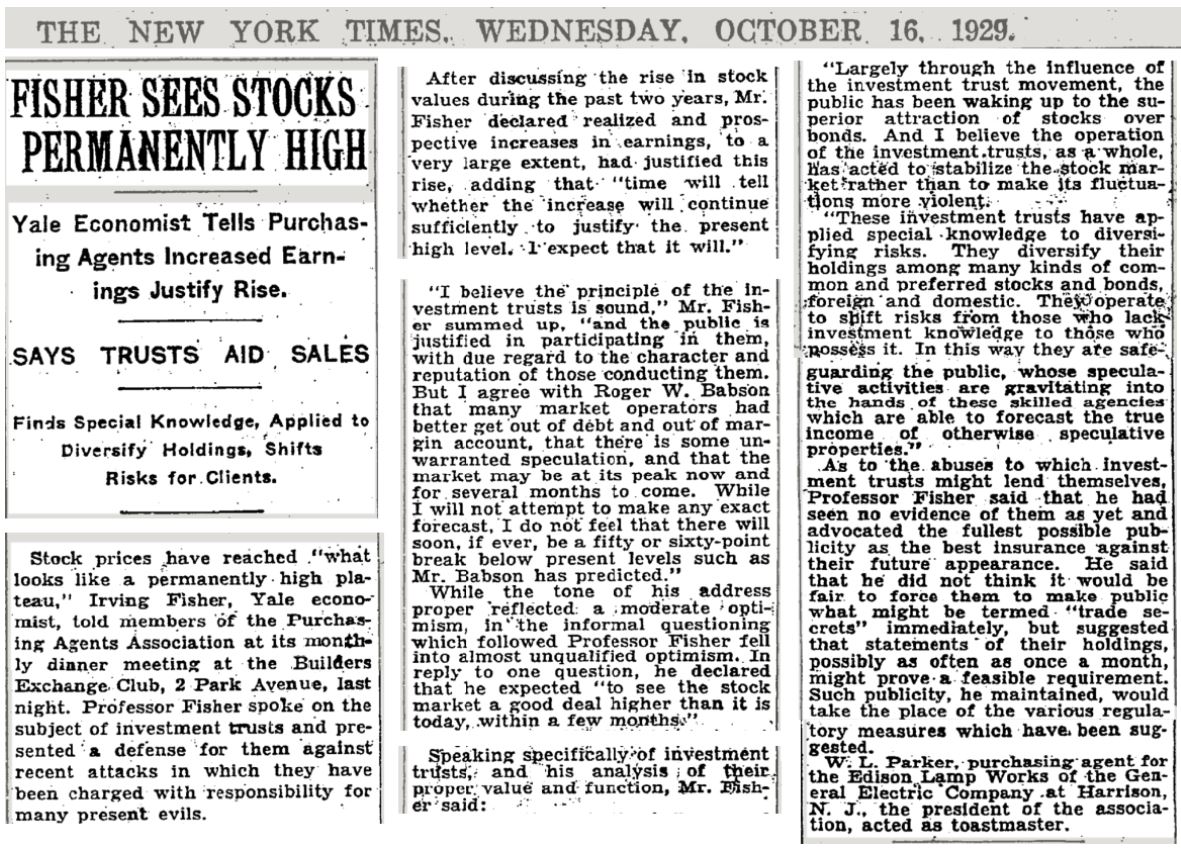

Yale economist Irving Fisher, October 15th 1929: “Stock prices have reached what looks like...