Recently we’ve seen signs of softening in the housing market due to the increase in interest rates to combat inflation. The concerns around a future recession often bring about concerns of declining asset prices, from stocks to bonds and real estate.

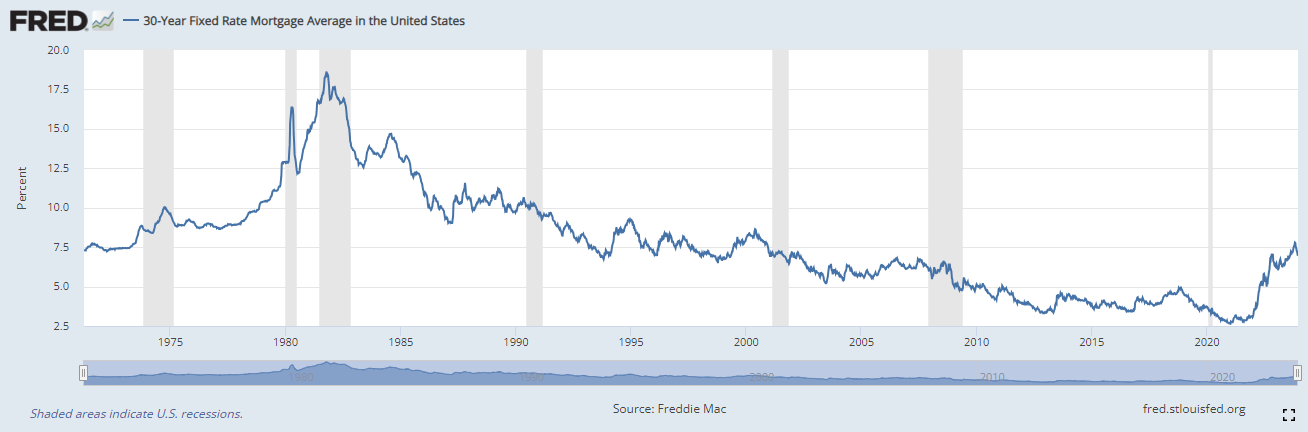

In the case of home prices, historically one of the biggest drivers of real estate values has always been the cost of financing. The higher the cost to borrow, the less the borrower can qualify for in lending. When looking at current financing costs, the average 30-year loan as of December 14th, 2024, is being issued at 6.95% according to the St. Louis Federal Reserve. To many younger readers, this may seem like an extremely high cost of borrowing. However, looking at the historical chart above, we can see that since the end of World War 2, the cost of borrowing has historically been above 7%, and in some cases much higher, peaking in September of 1981 at a whopping 18.27% average rate.

In fact, it is a relatively recent phenomenon that mortgage rates have been as low as they have been, which began with very aggressive Federal Reserve policy following the year 2000 technology crash, and then later amplified by the financial crisis. This was very recently followed by 2022 and 2023, which was one of the most aggressive series of actions by the Federal Reserve, increasing short-term lending numerous times from 0%, to 5.50%. While rates in the early 1980’s were much higher, the speed at which rates increased this time was much quicker.

Ultimately, does this mean doom for the housing market? Not necessarily. While it’s reasonable to assume this will impact the residential housing market negatively, there are other variables to consider.

After two decades of declining rates, a July 2023 report by Redfin found that currently in the United States:

91.8% of homeowners have locked in a mortgage rate below 6%.

82.4% of homeowners have locked in a mortgage rate below 5%.

62% of homeowners have locked in a mortgage rate below 4%.

23.5% of homeowners have locked in a mortgage rate below 3%.

When taking this into consideration, you can see why a substantial number of Americans would be hesitant to sell their homes if they are locked into such a low rate. Never forget that prices are set by the intersection of supply and demand. If a large number of people remain hesitant to sell due to their rate locks, that means the supply that would otherwise have hit the market is being suppressed.

As a homeowner, this helps anchor some stability in the equity of your home. However, as a younger couple, this may limit your ability to afford a home, as prices have not declined in accordance with the pace of interest rate increases, as normally would have been the case.

Does this mean that home values are invulnerable in the current environment? Certainly not. There are many variables that impact prices.

Should inflation re-accelerate, the Federal Reserve could be forced to further raise rates well above current expectations. If so, there would eventually be a point at which lending rates overwhelmed current prices.

If there were a severe enough recession, there could be a large enough spike in unemployment that leads to a substantial increase in loan defaults, thereby forcing more supply into the market.

While it’s impossible to predict short-term prices, it seems that the housing market may maintain some short-term support.

Commercial real estate seems to be somewhat more of a potential concern. Aside from the impact of higher interest rates, we still see some very high vacancy rates in the commercial real estate market, particularly in major cities with office space. The post covid world has seen much more of the workforce revert to working from home permanently.

In 2023 we have already seen some very high-profile defaults. PIMCO’s Columbia Property Trust defaulted on $1.7 billion of debt backed by a portfolio of US office space. Brookfield incurred a $750 million default on two large office towers in Los Angeles. RXR properties defaulted on a $240 million loan on a 33-story office tower in Manhattan. Additionally, other high-profile developers have liquidated properties at deep discounts in recent months.

Whether or not the concerns around commercial real estate begin to spread into other areas of the overall economy remain to be seen. However, like any other asset, expansion and contraction in prices are cyclical.

When making a real estate investment, it’s wise to still take a longer-term approach. In 2009, there was not a single prediction we can think of that would have suggested the Federal Reserve would hold rates at near zero for more than a decade. At the start of 2020, you would be hard pressed to find anyone that would have predicted the Federal Reserve would have set the Fed funds rate at 5.50%. As a result, we would suggest that any financial commitment to a property be a longer-term commitment, as trying to predict short-term real estate values or Federal Reserve policy with any degree of precision is as unrealistic as timing the stock market.

Filed under: Articles

Comments: Comments Off on Interest Rates and Real Estate: What Can You Expect?