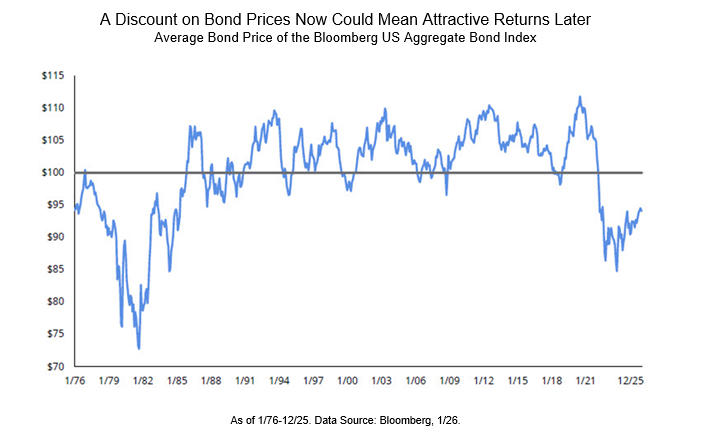

The Bloomberg US Aggregate Bond Index tracks a broad swath of the U.S. investment-grade taxable bond market, including Treasuries, government-related issues, corporate bonds, mortgage-backed securities (MBS), and asset-backed securities. Bond prices move inversely to yields. When interest rates rise sharply (as they did from 2022 into 2023), existing bonds with lower coupons become less attractive, pushing prices down. Looking at the chart above courtesy of Hartford, we can observe the following:

- The chart shows the index’s average price oscillating around or above par ($100) for much of the 1990s through 2020s low-rate era, often trading at premiums.

- Significant dips below par occurred during high-inflation/rising-rate periods (late 1970s–early 1980s, early 1990s, and post-2021).

- The recent drop to levels around $90 or lower in 2024 into early 2025 marked one of the deepest discounts in decades, echoing the early 1980s when rates were much higher.

This discount reflects higher prevailing yields after the Fed’s aggressive hiking cycle, with the index’s yield-to-worst hovering around 4.3%–4.5% in late 2025/early 2026 (compared to sub-2% levels in the late 2010s/early 2020s).

Why Discounts Signal Attractive Future Returns

When bonds trade at a discount:

- Investors buy them for less than par but still receive full par value at maturity (assuming no default, which is rare in investment-grade bonds).

- This built-in price appreciation adds to total return, alongside coupon payments.

- Higher starting yields provide a stronger income cushion against volatility.

Historical patterns support this:

- Periods when the Agg’s average price fell well below par (e.g., early 1980s, post-2008 dips) often preceded strong multi-year bond returns as rates eventually peaked and fell.

- The rebound from 2022’s historic drawdown (-13% in that year) has been solid, with the index delivering around 7.3% total return in 2025, its strongest annual performance in five years, fueled by falling yields and tightening spreads.

By early 2026, the average price appears to have recovered somewhat into the mid-$90s, reflecting the 2025 rally. Yet the index remains below historical premium levels, suggesting room for further gains if rates ease or stabilize.

Current Market Position (as of Early 2026)

- The Bloomberg US Aggregate has posted positive momentum, with trailing returns around 5–6% over the past year in many proxies.

- Duration currently sits near 6 years, with yields around 4.3%, and the market cap has grown substantially.

- Broader fixed income has benefited from disinflation, Fed policy shifts, and economic softening without recession.

However, some risks remain. Renewed inflation could push yields higher again, pressuring prices short-term. Still, the higher income buffer today, versus the prior low-yield era makes bonds more resilient to rate volatility.

Outlook: Opportunity in the Current Environment

The chart’s message holds relevance: buying bonds when discounted often rewards patient investors with compelling total returns over medium to long-term horizons. With yields still elevated relative to the 2010s and the index not yet back to chronic premium territory, core bond allocations offer diversification, income, and potential capital gains, especially in portfolios balancing equities.

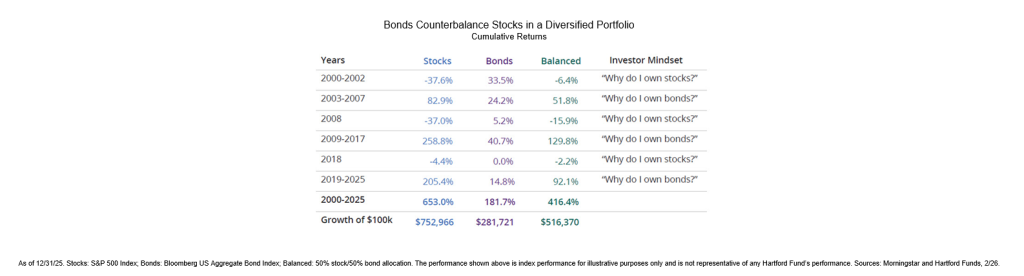

Looking at data below also courtesy of Hartford, we can see that using a balanced portfolio, bonds have served as an excellent ballast to equities in times of volatility.

For long-term investors, this setup echoes classic fixed-income opportunities: higher starting yields + discount to par = attractive prospective returns, provided defaults stay low and inflation remains contained.

It’s always important consider your risk tolerance, time horizon, and portfolio diversification, as bonds aren’t necessarily risk-free. However, the current discount environment positions them favorably compared to recent low-yield years.

About the Author

Joseph M. Favorito, CFP® is a Certified Financial Planner® as well as the founder and managing partner at Landmark Wealth Management, LLC, a fee-only SEC registered investment advisory firm. He specializes in helping individuals and families develop comprehensive financial strategies to achieve their long-term goals.