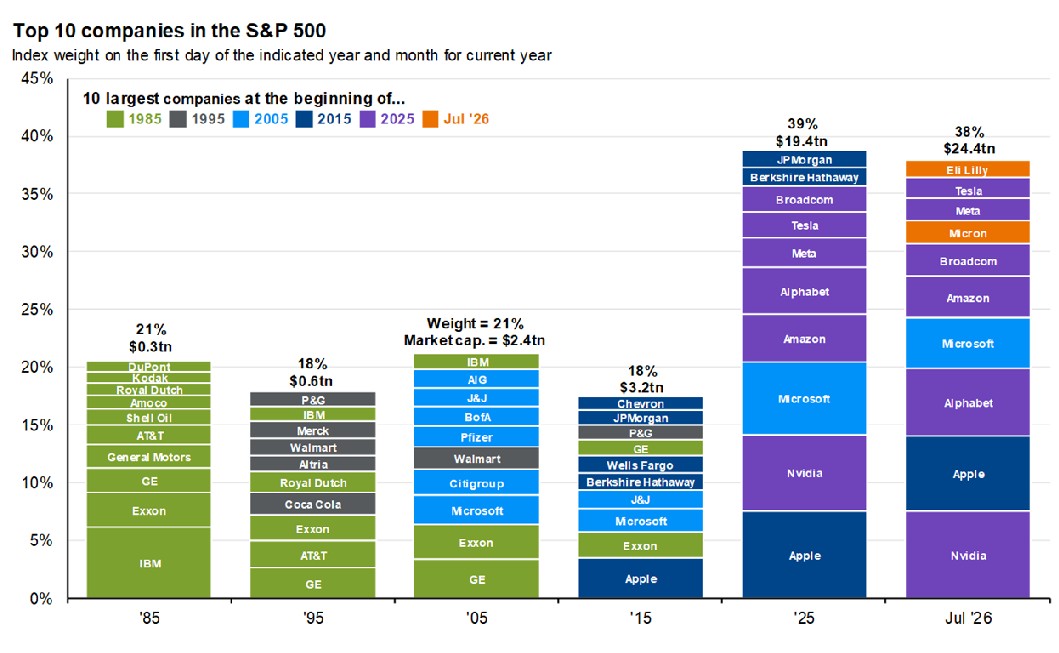

The composition of the S&P 500 has undergone a dramatic transformation over the past four decades. What was once a diversified group of industrial, energy, and consumer staples giants has become heavily concentrated in a handful of technology and growth-oriented companies. A new visualization provided by JP Morgan tracking the top 10 companies by index weight at the start of key years illustrates this shift powerfully from just 18-21% combined weight in earlier decades to a staggering 38-39% in 2025 and July 2026.

The Data at a Glance

According to the chart:

- 1985: Top 10 accounted for 21% of the S&P 500 ($0.3 trillion market cap). Dominated by industrial names like DuPont, Kodak, Royal Dutch, Amoco, Shell, AT&T, General Motors, GE, Exxon, and IBM.

- 1995: Concentration eased slightly to 18% ($0.6 trillion).

- 2005: Back to 21% ($2.4 trillion), still featuring a mix of traditional giants including IBM, P&G, AIG, J&J, Bank of America, Pfizer, Walmart, Citigroup, Microsoft, Exxon, and GE.

- 2015: 18% ($3.2 trillion) Apple had entered the top ranks alongside Exxon, Berkshire Hathaway, and others.

- 2025: Explosive jump to 39% ($19.4 trillion).

- July 2026: 38% ($24.4 trillion).

This represents one of the highest levels of market concentration in modern market history.

From Smokestack America to the Magnificent Tech Era

In the 1980s and 1990s, the S&P 500 reflected the U.S. industrial economy. Companies like GE, Exxon, and AT&T were the anchors. Market leadership was spread across sectors like energy, manufacturing, consumer goods, and telecom.

By the mid-2000s, financials and healthcare began rising, but the real inflection point came after 2015. The rise of smartphones, cloud computing, digital advertising, and more recently artificial intelligence (AI) propelled a new cohort of winners:

- Nvidia, Apple, Microsoft, Alphabet (Google), Amazon, Meta, and Broadcom now dominate the upper ranks.

- In July 2026, the top positions include Eli Lilly, Tesla, Meta, Micron, Broadcom, Amazon, Microsoft, Alphabet, Apple, and Nvidia.

This “Magnificent Seven” effect has been fueled by explosive earnings growth, network effects, platform economics, and massive capital investment in AI infrastructure.

Why Market Concentration Matters in 2026

- Higher Risk, Higher Reward When a small number of stocks drive the majority of index returns, the S&P 500 becomes less diversified. A slowdown in big tech or AI spending could trigger outsized volatility across the broader market.

- Valuation Implications Many of these leader’s trade at premium multiples justified by superior growth rates. However, any disappointment in earnings or regulatory scrutiny (antitrust, data privacy) can lead to sharp corrections that ripple through 401(k)s and indices.

- Sector Rotation Opportunities The concentration has left many “old economy” sectors such as financials, energy, industrials, and small-caps relatively undervalued. Investors are increasingly exploring equal-weighted S&P 500 strategies or value-oriented ETFs to reduce single-stock risk.

- Historical Context While current levels are elevated, they are not entirely unprecedented. The Nifty Fifty era of the early 1970s saw similar concentration in blue-chip growth names before a painful reset. Today’s environment is supported by stronger fundamentals in software and semiconductors compared to past cycles.

What This Means for Investors

- Passive investors in market-cap weighted S&P 500 funds are effectively making a heavy bet on a small group of tech and AI leaders.

- Active managers and stock pickers have underperformed in recent years due to this dynamic, but dispersion may create opportunities going forward.

- Long-term perspective: The companies driving today’s concentration have delivered remarkable innovation and shareholder value. The challenge is balancing participation in that growth without ignoring concentration risk.

Looking Ahead

As of July 2026, the S&P 500’s top 10 continues to command more than $24 trillion in combined market capitalization and almost 40% of index weight. Whether this concentration persists depends on the continued dominance of AI, cloud, and semiconductor demand, alongside macroeconomic factors like interest rates and regulation.

For investors, staying informed on the evolving makeup of the S&P 500 is more important than ever. Diversification, periodic rebalancing, and understanding the drivers behind market leaders remain key principles, even in an era where a few names move the entire market. Otherwise, investors may find themselves with a risk profile that is inconsistent with their risk tolerance.

About the Author

Joseph M. Favorito, CFP® is a Certified Financial Planner® as well as the founder and managing partner at Landmark Wealth Management, LLC, a fee-only SEC registered investment advisory firm. He specializes in helping individuals and families develop comprehensive financial strategies to achieve their long-term goals.