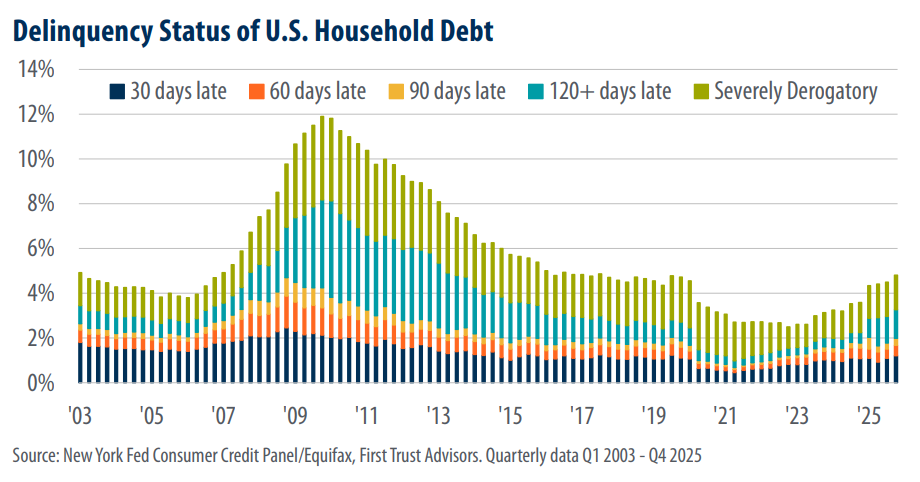

The latest figures on U.S. household debt paint a picture of rising delinquencies. Looking at the above chart courtesy of First Trust, according to the New York Federal Reserve’s Consumer Credit Panel, compiled with data from Equifax, aggregate delinquency rates for household debt rose to 4.8% in the fourth quarter of 2025. This marks an increase from 4.5% in the previous quarter and represents the highest level since late 2019, just before the COVID-19 pandemic disrupted global economies.

The data, spanning from Q1 2003 to Q4 2025, reveals stark historical patterns. Delinquency rates, defined as debt that’s at least 30 days past due, peaked dramatically during the 2008-2009 financial crisis, reaching around 12% as homeowners grappled with mortgage defaults and job losses. Rates then steadily declined through the 2010s, bottoming out in the low 3% range by 2021 amid stimulus measures and economic recovery. However, the post-pandemic years have seen a gradual uptick, accelerating in recent quarters.

Breaking it down by severity:

- 30 days late: This category, representing newly delinquent accounts, has driven much of the recent surge.

- 60 days late and 90 days late: These mid-stage delinquencies have shown modest increases.

- 120+ days late: Now at 1.3%, this matches the highest level since 2016, signaling persistent struggles for some borrowers.

- Severely derogatory: This includes accounts in collections or charged off, adding to the overall strain.

A key culprit in this rise? Student loans. Delinquency rates for student debt jumped sharply to 16.4% from 14.4% in Q3 2025, highlighting the ongoing burden of education costs amid inflation and wage stagnation. Other debt categories, such as credit cards, auto loans, and mortgages, also saw modest upticks, but student loans stand out as the primary accelerator.

This trend raises questions about broader economic health. With interest rates remaining elevated and consumer spending under pressure, households may be stretching their budgets thin. The resumption of student loan payments after pandemic-era forbearance has likely exacerbated the issue for younger borrowers, who often carry the bulk of this debt. Meanwhile, inflationary pressures on essentials like housing and food could be pushing more families toward delinquency in other areas.

Looking ahead, these figures could signal potential headwinds for consumer-driven growth, which accounts for about 70% of U.S. GDP. Lenders might tighten credit standards, making it harder for delinquent borrowers to refinance or access new loans. On a positive note, unemployment remains relatively low as of early 2026, which could help mitigate a full-blown crisis.

For consumers, the takeaway is clear: Monitor your debt closely, prioritize payments on high-interest accounts, and seek assistance from financial professionals if needed. As the data shows, delinquencies can snowball quickly, impacting credit scores and long-term financial stability.

This snapshot from the New York Fed underscores the fragility of household finances in a recovering yet volatile economy. Staying informed, and proactive will be key to navigate 2026 and beyond.

About the Author

Joseph M. Favorito, CFP® is a Certified Financial Planner® as well as the founder and managing partner at Landmark Wealth Management, LLC, a fee-only SEC registered investment advisory firm. He specializes in helping individuals and families develop comprehensive financial strategies to achieve their long-term goals.