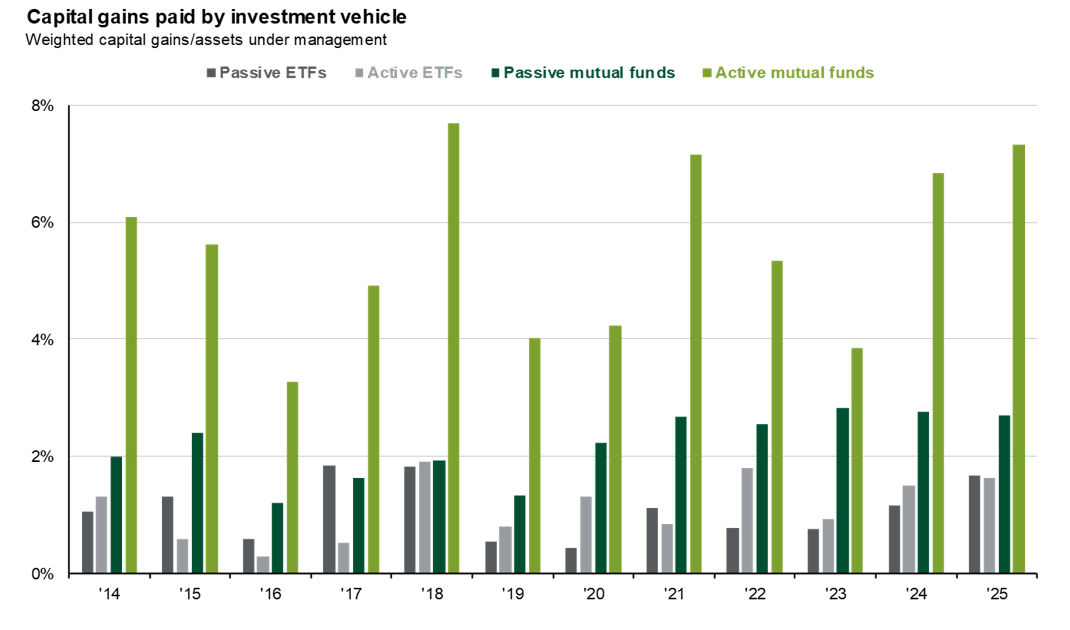

One of the most overlooked advantages of exchange-traded funds (ETFs) is their structural tax efficiency. The chart above makes this point clearly: ETFs, especially passive ETFs, consistently distribute far lower capital gains relative to assets under management than mutual funds, particularly active mutual funds.

This isn’t a one-year anomaly. It’s a persistent structural difference that can materially impact long-term after-tax returns.

What the Chart Shows

Across the full time series (2014–2025), a few patterns stand out:

- Passive ETFs: Consistently the lowest capital gains distributions, generally under 1.5%

- Active ETFs: Slightly higher, but still relatively tax-efficient

- Passive mutual funds: Moderate distributions, often in the 2–3% range

- Active mutual funds: By far the highest, frequently between 4% and 8%

In some years, like 2018, 2021, and 2025, active mutual funds distributed 3–5x more capital gains than passive ETFs.

That gap translates directly into higher tax bills for investors holding those funds in taxable accounts.

Why ETFs Have Lower Capital Gains

The tax advantage of ETFs isn’t about better stock picking, it’s about structure.

- The “In-Kind Redemption” Mechanism

ETFs use a unique process called in-kind creation and redemption:

- When investors sell ETF shares, they typically sell them on the open market, not back to the fund

- Large institutional players (authorized participants) handle redemptions

- Instead of selling securities to raise cash, the ETF transfers low-cost-basis shares out of the fund

Result:

The ETF avoids realizing capital gains internally.

Mutual funds, on the other hand:

- Must sell securities for cash when investors redeem shares

- This triggers realized gains, which are then distributed to all shareholders

- Lower Portfolio Turnover

Most ETFs, especially passive ones track an index:

- Minimal trading

- Fewer realized gains

Active mutual funds:

- Frequently buy and sell securities

- Generate ongoing taxable events

This difference compounds over time.

- Investor Behavior Matters

Mutual funds often experience:

- Large inflows near market peaks

- Outflows during downturns

This forces managers to:

- Sell holdings at inopportune times

- Distribute gains, even to investors who just bought in

ETF investors don’t trigger the same forced selling dynamic.

Why This Matters for After-Tax Returns

Taxes are one of the biggest drags on real investment performance, especially for high-income investors.

Let’s simplify the impact:

- A fund distributing 6% in capital gains annually

- Taxed at 20% federal capital gains rate (ignoring state taxes)

That’s a 1.2% annual tax drag

Compare that to:

- An ETF distributing 1%

That’s just 0.2% tax drag

Over time, that difference compounds significantly

A 1% annual advantage in after-tax return over 20–30 years can mean tens of percentage points in cumulative wealth difference.

Active vs Passive: The Tax Reality

The chart reinforces a critical point:

- The tax issue isn’t just mutual funds vs ETFs

- It’s also active vs passive management

Worst case (tax-wise):

- Active mutual funds

- High turnover + forced selling = large taxable distributions

Best case:

- Passive ETFs

- Low turnover + in-kind redemption = minimal taxable distributions

When Mutual Funds Still Make Sense

To be fair, mutual funds aren’t obsolete. They can still be appropriate in:

- Tax-advantaged accounts (IRAs, 401(k)s)

- Certain niche strategies not easily replicated in ETF form

- Institutional or retirement plan structures

But in taxable brokerage accounts, the data overwhelmingly favors ETFs.

Key Takeaways for Investors

- ETFs consistently distribute lower capital gains, improving after-tax returns

- The advantage is structural, not dependent on market conditions

- Active mutual funds are the least tax-efficient vehicle in most cases

- Over long periods, tax efficiency can be just as important as performance

Bottom Line

The chart above highlights a simple but powerful truth:

It’s not just what you earn, it’s what you keep.

ETFs give investors a structural edge by minimizing taxable events, allowing more capital to remain invested and compounding over time.

For investors focused on tax-aware portfolio construction, ETFs aren’t just convenient, they’re often the more intelligent choice.

About the Author

Joseph M. Favorito, CFP® is a Certified Financial Planner® as well as the founder and managing partner at Landmark Wealth Management, LLC, a fee-only SEC registered investment advisory firm. He specializes in helping individuals and families develop comprehensive financial strategies to achieve their long-term goals.