Investors with highly concentrated stock positions, often from equity compensation, business sales, or long-term holdings, face a difficult tradeoff: diversify and trigger taxes, or hold and accept risk. One increasingly sophisticated solution is the 130/30 strategy, which can simultaneously enhance tax loss harvesting opportunities and help gradually diversify concentrated holdings.

This article breaks down how a 130/30 strategy works, why it’s effective for tax management, and how it can be applied in real-world portfolio construction.

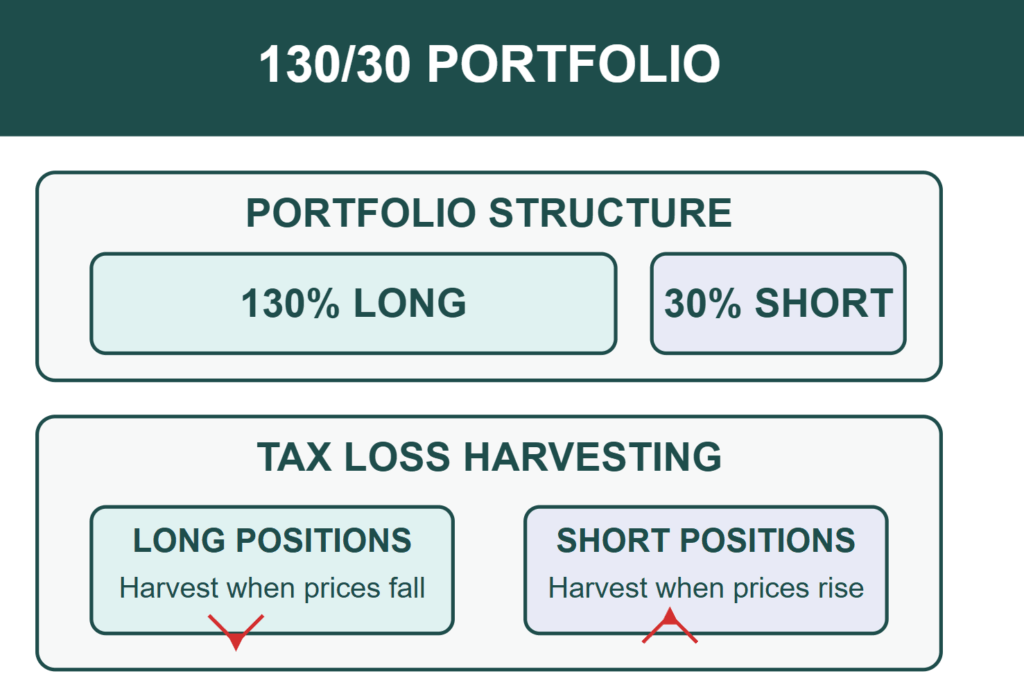

What Is a 130/30 Strategy?

A 130/30 strategy is an extension of traditional long-only investing. Instead of simply allocating 100% of capital to long positions, the portfolio manager:

- Goes 130% long (buys securities expected to outperform)

- Goes 30% short (sells borrowed securities expected to underperform)

The proceeds from the short sales fund the additional long exposure, keeping the net market exposure at 100%.

Key Characteristics:

- Maintains equity-like market exposure

- Introduces active long/short positioning

- Enhances tax management flexibility

- Provides additional sources of return (alpha)

Why Concentrated Stock Positions Are a Problem

Holding a large position in a single stock can create:

- Idiosyncratic risk (company-specific exposure)

- Tax constraints (large embedded capital gains)

- Emotional bias (attachment to a legacy holding)

Selling outright may trigger substantial capital gains taxes, especially for long-term appreciated assets. This is where a 130/30 strategy becomes particularly valuable.

How a 130/30 Strategy Helps Diversify Without Immediate Liquidation

Instead of selling the concentrated position outright, a 130/30 structure allows investors to:

- Maintain the Core Position

The concentrated stock can remain part of the portfolio, avoiding immediate tax realization.

- Overlay Active Long/Short Positions

The manager builds:

- Long positions in diversified equities

- Short positions in overvalued or correlated securities

This effectively dilutes the concentration risk without requiring a full liquidation.

- Reduce Effective Exposure

Even if the concentrated stock remains, the broader portfolio reduces its relative weight and risk contribution.

The Tax Loss Harvesting Advantage

The most powerful feature of a 130/30 strategy is its ability to systematically generate tax losses.

How It Works:

- Short Positions Create Natural Loss Opportunities

Short positions frequently produce realized losses due to market volatility and active trading.

- These losses can be harvested throughout the year

- They are often short-term losses, which are more valuable for tax offset purposes

- High Turnover = More Harvesting Opportunities

Unlike passive portfolios, a 130/30 strategy typically involves:

- Frequent rebalancing

- Active security selection

- Continuous replacement of positions

This leads to a steady stream of realized gains and losses, increasing the probability of harvesting losses.

- Offsetting Gains from Concentrated Positions

Harvested losses can be used to offset:

- Gains from partial sales of the concentrated stock

- Gains generated within the long portfolio

- Up to $3,000 of ordinary income annually (with carryforward benefits)

Accelerating Diversification Through Tax Efficiency

A well-structured 130/30 strategy allows for gradual diversification of a concentrated position in a tax-aware manner.

Step-by-Step Approach:

- Implement 130/30 Overlay

- Maintain concentrated stock

- Introduce long/short framework

- Harvest Losses from Short Book

- Capture losses as markets fluctuate

- Build a “tax loss bank”

- Strategically Sell Concentrated Shares

- Use harvested losses to offset gains

- Reduce tax impact of sales

- Reinvest Into Diversified Holdings

- Increase exposure to broader sectors

- Lower single-stock risk over time

Additional Benefits of a 130/30 Strategy

Enhanced Risk Management

- Reduces dependence on a single stock

- Allows hedging via short positions

Potential for Alpha Generation

- Gains from both long and short selections

- More tools than traditional long-only portfolios

Tax-Aware Portfolio Construction

- Continuous realization of losses

- Greater control over taxable events

Risks and Considerations

This isn’t a free lunch. A 130/30 strategy introduces complexity and risk:

Short Selling Risk

- Losses on shorts are theoretically unlimited

- Requires active monitoring

Higher Costs

- Trading costs

- Borrowing costs for short positions

- Potential management fees

Tax Complexity

- Short-term vs. long-term gains/losses

- Wash sale rules must be carefully managed

Manager Skill Matters

The success of a 130/30 strategy depends heavily on security selection and execution.

The ETF Approach

- Build the 130% Long Book with Sector ETFs

Instead of owning individual stocks, you allocate across sector ETFs that roughly mirror the S&P 500’s weights:

- Technology → Technology Select Sector SPDR Fund (XLK)

- Healthcare → Health Care Select Sector SPDR Fund (XLV)

- Financials → Financial Select Sector SPDR Fund (XLF)

- Consumer Discretionary → Consumer Discretionary Select Sector SPDR Fund (XLY)

- Industrials → Industrial Select Sector SPDR Fund (XLI)

- Energy → Energy Select Sector SPDR Fund (XLE)

- etc.

You scale the allocation so the total exposure equals 130% of your capital, approximating the index at the sector level.

- Short 30% of the Broad Market

Then you short a broad S&P 500 ETF like:

- SPDR S&P 500 ETF Trust (SPY)

This creates:

- 130% long (sector ETFs)

- –30% short (S&P 500)

- Net = 100% market exposure

What This Actually Does (Economically)

You’ve essentially created:

A “portable alpha / tax overlay” on top of the S&P 500

Because:

- The long basket = S&P 500 (sector replication)

- The short position = S&P 500

So, the market exposure essentially cancels out, leaving:

- Small Relative Sector Tilts

Minor differences in sector weights and ETF tracking create modest active exposure.

- A High-Turnover Overlay Layer

This is where the tax alpha comes from.

Why This Structure Is Powerful for Tax Loss Harvesting

- Sector ETFs Create More Loss Opportunities

Different sectors move differently:

- Tech may be down while energy is up

- Healthcare may lag while financials rally

This dispersion allows you to:

- Harvest losses in one sector ETF

- Replace it with a similar (but not identical) exposure

- Avoiding wash sales while maintaining market exposure

- The Short Side Adds Additional Loss Generation

The short position in SPDR S&P 500 ETF Trust (SPY):

- Is marked-to-market

- Can be tactically covered/re-established

- Often produces short-term gains/losses

This increases the frequency of realizable tax events, especially short-term losses.

- You Maintain Market Exposure While Harvesting

Unlike selling a concentrated position outright:

- You stay invested in equities

- You avoid timing risk

- You continuously generate harvestable losses

How This Helps a Concentrated Stock Position

If you also hold a large single-stock position:

- The 130/30 overlay runs alongside it

- You accumulate tax losses from the ETF + short book

- You use those losses to:

- Offset gains from gradually selling the concentrated stock

- Reduce tax drag over multiple years

Key Advantages of This Approach

- Simple implementation (liquid ETFs)

- Highly scalable

- Efficient tax loss generation

- Maintains full market exposure

- Reduces single-stock risk over time

Risks / Watchouts

- Tracking error vs. the S&P 500

- Short borrowing costs / dividend expense on the short

- Wash sale rule management

- Requires active monitoring to be effective

Bottom Line

Using sector ETFs to build the 130% long side and shorting the S&P 500 ETF is a practical way to:

- Replicate market exposure

- Introduce controlled active variation

- Maximize tax loss harvesting opportunities

- Create a tax-efficient path to diversify concentrated holdings

Who should Consider the 130/30 Strategy?

This strategy is best suited for:

- High-net-worth investors with large embedded gains

- Individuals with stock-based compensation (RSUs, options)

- Business owners post-liquidity event

- Investors seeking advanced tax optimization strategies

Final Thoughts

A 130/30 strategy can be a powerful tool for investors dealing with concentrated stock positions. By combining active long/short investing with systematic tax loss harvesting, it creates a pathway to:

- Reduce risk

- Improve tax efficiency

- Gradually diversify without triggering large upfront tax liabilities

The 130/30 strategy can work as a great method to diversify away a concentrated position for investors who are willing to slowly reduce their concentration and accept the short-term risk associated with their concentrated holding. It’s important to understand that a 130/30 approach does not limit the short-term risk while you still hold this concentration. Investors with greater concerns about downside protection should consider other risk mitigation strategies, such as an options collar, which is explained here:

Investors interested in the 130/30 approach should understand that this requires careful implementation, ongoing management, and a clear understanding of both investment and tax implications.

About the Author

Joseph M. Favorito, CFP® is a Certified Financial Planner® as well as the founder and managing partner at Landmark Wealth Management, LLC, a fee-only SEC registered investment advisory firm. He specializes in helping individuals and families develop comprehensive financial strategies to achieve their long-term goals.