One of the most fundamental concepts in fixed income investing is that bond prices and interest rates have an inverse relationship. When interest rates rise, bond prices fall. When interest rates fall, bond prices rise. Understanding this dynamic is essential for investors, especially in changing rate environments like the one we’ve seen in recent years.

The Core Concept: Inverse Relationship Between Bonds and Rates

At its simplest, a bond is a loan. When you purchase a bond, you’re lending money to an issuer (like a corporation or government) in exchange for periodic interest payments and the return of principal at maturity.

The key factor is this: existing bonds are locked into their original interest rates, while new bonds are issued at current market rates.

What Happens When Interest Rates Rise?

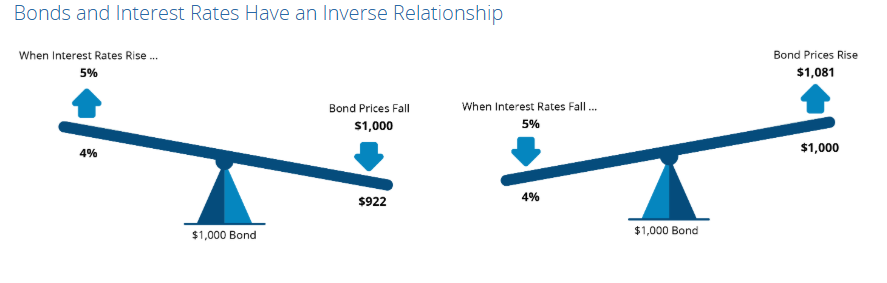

- A bond originally issued with a 4% interest rate is priced at $1,000

- Market interest rates rise to 5%

- New bonds now offer better yields (5% vs. 4%)

Because of this, your 4% bond becomes less attractive. Investors won’t pay full price for a lower-yielding bond when higher-yielding alternatives exist.

Result: The bond price drops.

What Happens When Interest Rates Fall?

- A bond originally yielding 4% is priced at $1,000

- Market rates drop to 3%

- Your bond now offers a higher yield than newly issued bonds

This makes your bond more valuable in the secondary market.

Result: The bond price rises.

Why This Happens: Present Value and Discounting

Bond pricing is based on the concept of present value. Future interest payments (cash flows) are discounted back to today using current interest rates.

- When rates rise, future payments are discounted more heavily → lower bond prices

- When rates fall, future payments are discounted less → higher bond prices

This mathematical relationship is the backbone of bond valuation.

Duration: The Sensitivity Factor

Not all bonds react equally to interest rate changes. This is where duration comes into play.

- Short-term bonds: Less sensitive to rate changes

- Long-term bonds: More sensitive to rate changes

For example:

- A 2-year bond might decline slightly when rates rise

- A 30-year bond could experience significant price swings

This is why duration is a critical risk metric for bond investors.

Real-World Implications for Investors

- Rising Rate Environment

When rates are increasing:

- Bond prices decline

- Existing bond portfolios may lose value temporarily

- New bonds become more attractive due to higher yields

- Falling Rate Environment

When rates are decreasing:

- Bond prices rise

- Existing bonds gain value

- Income from new bonds decreases

Strategic Takeaways

- Diversification matters: Holding bonds of varying maturities can help manage interest rate risk

- Focus on income vs. price: If you hold a bond to maturity, price fluctuations may matter less

- Active management can help: Adjusting duration exposure based on rate expectations can improve outcomes

Why This Matters Right Now

In today’s market, where interest rate policy and inflation are constantly shifting, understanding the relationship between bonds and interest rates remains very important. Investors who grasp this dynamic are better equipped to:

- Manage portfolio risk

- Take advantage of pricing opportunities

- Avoid emotional decision-making during market volatility

Final Thoughts

The visual above simplifies a complex concept into an intuitive idea: rates up-bond prices down, rates down-bond prices up. Other variables, such as credit quality and taxation can also impact the value of fixed income in addition to the relationship with interest rates. However, while the math behind this relationship can get more intricate, the principle remains consistent across all fixed income markets.

If you’re allocating to bonds, whether for income, stability, or diversification, this relationship should always be in the front of your mind.

About the Author

Joseph M. Favorito, CFP® is a Certified Financial Planner® as well as the founder and managing partner at Landmark Wealth Management, LLC, a fee-only SEC registered investment advisory firm. He specializes in helping individuals and families develop comprehensive financial strategies to achieve their long-term goals.