The Bond Market: How Attractive is Fixed Income Today?

Looking at the bond market today, we can see that bond prices still haven’t fully recovered from the unprecedented decline of 2022. While 2022 is not that far behind us, let’s remember how unprecedented the decline actually was.

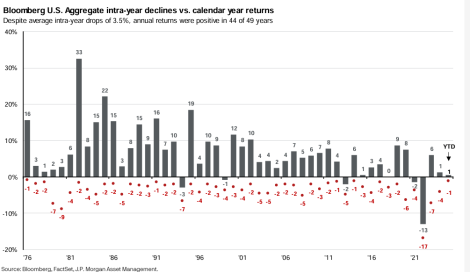

Over the last century the bond market has seen an average intra-year decline of approximately -3.5%, with the bond market turning positive approximately 92% of the time. This data shows that while bonds may not demonstrate the same long-term returns of stocks, they have always served as a good ballast to the inherent volatility of the stock market.

As we look at 2022, we saw an intra-year decline of approximately -17% with a final decline of -13% in the US Aggregate Bond Index. One would have to go back to the year 1787 to find a year that bad in the returns of US Bonds.

Since 2022, bond prices have stabilized as the Fed has reversed course on its aggressive rate hiking cycle, and bond prices have recovered somewhat. But what we can see from the data above is that bonds in general are still trading at a discount.

In order to correctly understand this, it’s important to understand how a bond is priced and where the return comes from. When you buy a bond, you are essentially loaning money to a government agency, or a company. They issue that bond at a stated interest rate, which is usually fixed, but not always. At a certain point in time that bond will mature, and you will receive back your principal, plus the interest payments annually while you wait. This is not unlike the process of buying a CD at the bank. However, a CD has FDIC insurance, whereas a bond is backed by the issuer, which in the case of government bonds can be the US government.

When a bond is first issued, it’s issued at what is called par value, which is either $100, $1,000 or $5,000. If par is $100 and you hold the bond until it matures, then you will receive back your par value of $100 regardless of how much it fluctuates prior to maturity. This also assumes that the issuer doesn’t default on the debt, which can happen with a corporate bond, but is extremely rare in tax-free municipal bonds.

However, bonds trade publicly among investors-both individuals and institutions. When the Fed raises rates, the bond that you bought at an interest rate of 3% looks less attractive when new bonds are issued at 4%. Therefore, if you’d like to sell your bond before it matures, you must take whatever discounted price the market offers, otherwise you can hold it until maturity. The discount the market demands will depend on a confluence of factors, such as how much time is left before it matures, the credit quality of the issuer, and how much rates have changed since it was issued.

The reverse could also be true if rates have come down since the bond was issued, then the bond would trade above $100 at a premium.

Remember that even if you have no intention of selling your bond and would prefer to hold it to maturity, your statement must reflect the current market price.

When looking at a bond index, this is a mathematical formula that represents a group of bonds for broad representation of the bond market. There are indices of the overall taxable bond market, municipal tax-free bond market, or other more narrow indices that focus just on areas such as high yield bonds, or exclusively government bonds. These indices give you a representation of how well or poorly the overall bond market is doing at any point in time.

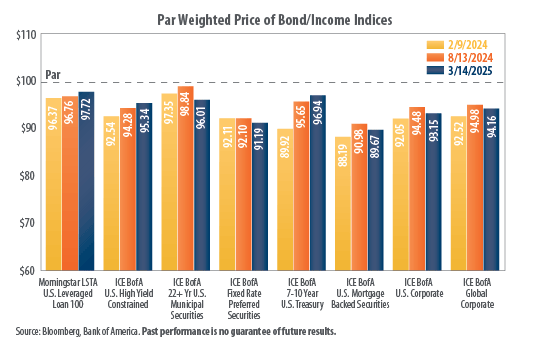

Looking at the data above courtesy of First Trust, we can see the trend since this time last year in many areas of the bond market. The data shows that bond prices have recovered in most areas since last year with the exception of long-term municipal bonds, and preferred securities which are not really bonds, but rather a hybrid of fixed income and stocks.

However, while there is a general improvement in the overall price of the bond market, we can see that the markets as a whole are still trading well below their par value. As an example, US mortgage-backed bonds are still trading close to 90 cents on the dollar. Other areas, such as the 7-10 year US Treasuries are closer to 96 cents on the dollar, and global corporate debt is closer to 94 cents on the dollar.

What this means is that as you buy into those areas, you are paying a discount. If you bought a 7-10 year treasury at 96 cents on the dollar, you will receive the full 100 cents at maturity when the 7-10 year has come due.

Many investors don’t buy individual bonds due to diversification concerns, nor do we. However, as we look at the current fixed income landscape, we can see that even after a solid recovery in bonds in 2023 and 2024, the overall bond market is still actively priced at a discount. This does not mean there is no room for further downside. Regardless of the circumstances, there is typically always a place for some degree of fixed income in most portfolios. But looking at the circumstances today, the bond market looks very well positioned for an asset class that typically has been very low volatility.