Over the years, one common choice individuals are faced with is how to receive their pension benefit when it is offered to them at retirement. There are more numerous options routinely available, such as a single life payment, joint life payment or even more common in recent years, the lump sum option. Let’s first start by pointing out that for individuals who are employees of a government agency, a lump sum option is typically not a choice you will be offered.

The lump sum option has become more common for those in the private sector that have worked for large multinational corporations, and even some mid-sized businesses. This is largely due to the longer than expected life expectancies we are facing, as well as other demographic changes that can impact the actuarial projections of a pension fund. It is very difficult to predict in a pension fund what these legacy costs will be due to a variety of reasons. Companies may have a smaller number of employees in the future contributing to the fund. They may have slower than expected business cycles that force layoffs and reduce staff. As a result, there is and will continue to be more of a push towards defined contribution plans (401k/profit sharing) in the future. The largest challenge is the substantial increase in life expectancies since many of these pension funds were initiated many decades ago.

Let’s first address the lump sum option. In many of the cases, the lump sum option is the more prudent choice. Pension funds are using the same actuarial data to make projections about life expectancy to determine their liabilities as an insurance company that sells an immediate fixed annuity. An immediate fixed annuity bought privately has the same characteristics to the individual as a private pension benefit once the receipt of income begins. The distribution rate is typically very similar. However, in some cases the entirety of the pension benefit offered as an income is not needed at the moment the individual retires.

Let’s imagine a 65 year old retiree who is being offered $60,000 per year, or a lump sum of $1,000,000. What if the retiree after examining their financial needs, determines they only need about $40,000 per year based on their current lifestyle and other income sources? The individual could simply opt to take the entire $1,000,000, roll it to an IRA on a non-taxable basis, and then choose to buy an immediate fixed annuity by shopping the best payment with multiple insurance carriers. Except, in order to achieve the desired income, they would likely only have to utilize approximately $670,000 at a 6% distribution rate, which would generate an income in the range of $40,000 annually. This would then permit the investor to keep the additional $330,000 in their IRA on a tax deferred basis to keep growing until the income was needed in the future, or to be left to their heirs as beneficiaries. The key is ultimately the flexibility. Please note that these income assumptions are close to current norms, but are not specific to any one insurer or annuity offering.

Solvency is also a key issue. If you are a participant of a private sector pension fund, the only real guarantee you have if a pension fund is taken into receivership is through the Pension Benefit Guarantee Corporation (PBGC). However, PBGC only secures a portion of these pension funds under a formula that is rather complex, and can greatly limit the benefit of someone that would have been entitled to a sizeable pension. Pension funds can and do go bankrupt. It happens more often than most workers realize, and some are substantially underfunded. On the contrary, your 401k, while subject to the same market risk on investments that the pension fund is also subject to, remains 100% yours once you have become vested. At a maximum that is likely to be six years of service with your employer. The difference is a pension fund is a liability of the corporation, whereas a personal account is a segregated asset, and not a liability of your employer, therefore not subject to the claims of their creditors.

The next common sense question is “What happens if I annuitize money from a pension lump sum and then the insurance company goes under?” This is an important consideration, and requires some homework to be done. In many states, there is a state guarantee fund on benefits issued to the purchaser of an insurance product in the event of a default. As an example, New York State has the Life Insurance Company Guaranty Corporation of New York, which currently guarantees benefits of 100% up to $500,000.00 per individual.

So in the event of pension replacement, or any form of an insurance product, it may be prudent to limit the purchase to no more than $500,000 in the State of N.Y. If necessary, you can purchase more than one product from multiple insurance carriers to coordinate benefits. In the case of annuity payments there will typically be more than one company offering a similar payment option. Since insurance is regulated at the state level, you would need to inquire with your insurance commissioner’s office as to what guarantees, if any, exist. It should also be noted that many licensed insurance agents do not mention this backup fund, as they are prohibited from utilizing it as a sales incentive. The responsibility to inquire about any state guarantees rests upon the consumer.

Furthermore, with a pension fund from an employer there may be an option for a survivor benefit to the spouse at a reduced rate. However, many pension funds offer no continuing benefit to children or other non-spousal beneficiaries. So in the event that you choose to retire after 30 years of service with a joint survivor benefit, and then you and your spouse pass away relatively young, there may be nothing left to your heirs. The amount that you either contributed to the pension fund, or that which was contributed on your behalf for your service, simply becomes a forfeiture reallocation. This basically means the pension fund keeps your money, and it reduces the burden of liability they must pay to other families in the future. Should you opt to privately annuitize money in an immediate fixed annuity, insurers virtually always offer multiple guarantee options, such as a 20 year period certain guarantee. Such an option insures that someone of your choosing will receive a benefit equal to the amount of money funded, and it will not be lost.

What about cases in which someone is not offered a lump sum, but only a joint survivor benefit, or what is sometimes called a pop-up option? This is rather common among civil service employees. These should be examined closely, as there is usually more than one formula available. While there are no universal answers that apply to all, a survivor benefit of some type often makes the most sense for couples.

In many cases, an insurance agent will show you an illustration of how you can purchase life insurance on the pension recipient at a cost that is less than the amount of reduced income one might realize by taking the joint benefit. The challenge in such a scenario is that it often requires a substantial amount of insurance to replace the loss of a pension. This usually requires term insurance to be issued on an individual that will receive a large pension benefit, because it is the least expensive. While term coverage makes excellent sense for a young couple, it can be risky for couples closing in on retirement benefits. If you are 65 (assuming you are insurable), a term policy will typically not cover you past age 80. So what happens if the pension recipient dies at age 81, and the survivor has neither the life insurance, nor the pension, and lives to age 95? The alternative is to utilize permanent life insurance such as whole life, universal life, or variable life policy. However, that will greatly drive up the cost of the annual premiums, often making it a poor choice, and possibly unaffordable.

When examining the cost of insuring the individual benefit versus the joint survivor options being proposed, you should try and think of the reduced annual benefit as the insurance premium. When examining it from that perspective, you are essentially purchasing the equivalent of a level term insurance policy that has no term limit. It will last your life expectancy.

As an example: If the $60,000 pension is reduced to $54,000 in order to capture the joint benefit for a spouse, the reduction should be compared to the cost of a term policy. The amount needed to replace a $60,000 fixed annual income for a 65 year old is approximately $1,000,000 (6% annual distribution rate). The cost to purchase a $1,000,000 term insurance policy for 10-15 years may possibility be less than $6,000 annually, if the individual receives favorable underwriting due to excellent health. However, at the end of the 15 years, the survivor is left with no benefit guarantee, and possibly a number of years remaining in retirement. By taking, the survivor benefit, the $6,000 annual difference becomes the equivalent of a lifetime of level term insurance.

It is always important to note that each situation is unique, and there is no “one size fits all” in financial planning. Determining how to handle ones pension options is one of the larger financial decisions a person will make in their lifetime. In many cases, utilizing a lump sum strategy instead of an employer’s annual payment, and annuitizing all or part of the benefit as a pension replacement makes the most sense. Keep in mind that not all annuity products are the same. Many are loaded with expensive and unnecessary “bells and whistles” like features. It is advisable to seek a second opinion from an independent financial professional on what options make the most sense, rather than simply take the word of a commissioned sales agent. It can be prudent to discuss these issues with your tax advisor and/or a fee-only financial professional that does not sell insurance products for some unbiased advice.

Filed under: Articles

Comments: Comments Off on How To Handle Your Pension Options

There are few things people dislike more than having to pay taxes. Investors are no different in that regard, and perhaps even more so as it pertains to capital gains taxes. When an individual goes to work, they know at the end of their work day that they will typically be paid based on specific formula of hourly wages or salary. Investors often commit dollars to a specific opportunity with no guarantee of any return whatsoever. In fact, the risk of a loss of some type is almost always a threat. As a result, any opportunity to enhance the probability of success is paramount. Tax efficiency is a key component of a well thought out investment plan. Tax Loss Harvesting is one of the most important aspects of a tax efficient investment plan.

Capital gains taxes are levied at an investor’s ordinary income tax rate should they hold an investment for less than one year. In the event that an investment is held for more than one year, capital gain rates can be levied at as much as 20%, as well as additional capital gain taxes levied at the state level. Furthermore, another 3.8% tax on net investment income (which includes capital gains) may be assessed on individuals with an adjusted gross income over $125,000 ($250,000 for joint filers) due to legislation initiated with the Affordable Care Act.

When an investor loses money on a capital investment, they may report the loss on their income tax return as an adjustment against their ordinary income (wages/salary). Presuming they have no capital gains in the year of the tax filing, they are permitted to utilize only $3,000.00, and carry the remaining amount forward into future tax years using $3,000.00 annually. So if you bought a stock or lost money on an investment property, it wouldn’t matter if the loss is in excess of $100,000.00. The total loss would take more than 33 years to realize!

However, the IRS does permit the use of an entire capital loss to be used on a dollar for dollar offset against a capital gain in a given tax year. So, the same $100,000.00 loss can be used to wipe out a $100,000.00 gain in a single year, netting a zero tax liability.

When it comes to the active management of an investment portfolio, this is where things begin to get creative.

The IRS has a rule known as a wash sale rule.

The rules effectively state that a wash sale occurs when you sell or trade securities at a loss and within 30 days before or after the sale you:

Buy substantially identical securities, or

Acquire substantially identical securities in a fully taxable trade, or

Acquire a contract or option to buy substantially identical securities.

If you were to buy a stock, and then subsequently sell the stock for a loss, and then repurchase it within the restricted time frame referenced above, the loss will be disqualified. The reason is the IRS does not want investors to sell investments and immediately buy them back the same day in order to capture a loss against something they still really own all the while. New and more advanced technologies now require brokerage firms to track cost basis in great detail which is transferred with an investor’s account from firm to firm, and then report gains and losses to the IRS on the form 1099

The term “substantially identical securities” would clearly mean that you can’t sell stock in IBM, and then re-buy IBM within the window of restriction. It would also prohibit the purchase of options in which IBM was the underlying security. Furthermore, should an investor sell a Vanguard S&P 500 index fund, then immediately purchase a Fidelity S&P 500 index fund, the same would be true, as the underlying investments pertain to exactly the same investment components in the same proportion. Now let’s imagine that you purchased an investment in an S&P 500 Index ETF, and the market subsequently declined. In order to capture the loss, you opted to purchase a position with the sale of the proceeds into an ETF that tracks the Russell 1000 index. In this case, your loss is in fact permitted. The reason is while you are purchasing another index which is highly correlated with a great deal of overlap in underlying holdings, they are not precisely the same.

What about traditional Mutual Funds?

Actively managed mutual funds offer a similar benefit. In the sale of one mutual fund in order to buy another mutual fund that has a manager with a similar strategy and core holdings, the loss is permitted. In both of these examples the positions are substantially similar and highly correlated, but not substantially identical.

Why does this matter so much?

A key part of a sound long term investment plan is to actively rebalance a portfolio during the year back to an appropriate level of risk. In a year in which stocks have done well and bonds have done poorly, you should be trimming some of the profits from your stock market exposure, and adding those profits into your bond market exposure. In years where the opposite has happened, you do the inverse. This process of rebalancing forces a portfolio to constantly sell high and buy low. However, when done in a non-retirement account (IRA/401k) that is not tax sheltered, this can begin to present tax problems.

When utilizing proper Tax Loss Harvesting techniques, the tax liability can be mitigated if not eliminated. Imagine that you had a poor year in the stock market, and wanted to sell some of your bond holdings in order to put more money into your stock holdings. What if the new money was supposed to go into the S&P 500 ETF, which has now declined by $10,000.00 since the original purchase? You can simply sell the entire position, capture the tax loss, and use the proceeds plus the new money from the sale of the bond holdings to purchase the Russell 1000 ETF. In doing so, you have rebalanced your portfolio back to the originally desired asset allocation. Simultaneously, you have captured a tax loss that can be utilized against the sale of the bond holdings where you took the profit and realized a capital gain, allowing one to cancel the other, possibly resulting in a ZERO tax liability, or even a deduction.

This technique becomes increasingly important for investors that buy actively managed mutual funds outside of a tax sheltered retirement account. Actively managed funds often payout capital gain distributions to shareholders of a fund following a positive, or in some cases negative year in relation to the trading that took place. This is essentially a payout of a cash distribution in a specific amount of dollars, while then simultaneously reducing the value of the funds price equal to the amount of the distribution. In some cases a new investor may have bought a fund close to the end of the year, having never participated in the prior gain. Yet, they will still be affected by a distribution the fund pays to existing shareholders. Such a situation is the worst of all scenarios, as it is can essentially be a tax liability without ever having realized the gain. Not many investors wish to pay tax on someone else’s gain.

Bond Funds

Bond Funds present a particularly interesting opportunity, because they derive most of their return from the dividend/interest income they produce. While they have no stated maturity date, the underlying bonds held in the fund do. Imagine an investor who buys a bond fund in their portfolio for diversification, but does not need the income at this point in time. So as a result, they opt to re-invest all their monthly dividend income.

Let’s look at an example using the average cost per share methodology for tax purposes.

An account set for reinvestment of dividends and interest, buys Mutual Fund XYZ which pays $40 a month of interest. In this example also assume an initial purchase of $10,000 and no change to the net asset value of the investment at the end of the period:

Date:

Purchases:

Cumulative Cost Basis:

January

$10,000

$10,000

February

$40

$10,040

March

$40

$10,080

April

$40

$10,120

May

$40

$10,160

June

$40

$10,200

July

$40

$10,240

August

$40

$10,280

September

$40

$10,320

October

$40

$10,360

November

$40

$10,400

December

$40

$10,440

January

$40

$10,480

In this example, your initial $10,000 investment would now be worth $10,480 which is a 4.80% gain. Now, let’s say in this example, due to market fluctuation of Bond Fund XYZ, at the end of the year it was only worth $10,200. This would reflect as a loss of -2.67% (due to the cost basis being $10,480 minus a current value of $10,200), when in reality it is an actual gain of +2.0% ($10,000 now worth $10,200).

Let’s assume that rather than reinvesting the interest payment each month, you had the interest payment go into your money market account. The cost basis would stay at the original $10,000, you would have collected $480 dollars of interest, and you could still recognize a taxable loss if the mutual fund was sold at a price of less than $10,000.

The reason this is a loss with the IRS in the case of the reinvested dividends, is the dividends you received which drive the return of the investment were not obligated to be reinvested. However, because you did reinvest them, you altered your cost basis every month. In many cases, what is a loss on paper may actually be a gain. Now, using a similar strategy as referenced earlier, you can sell XYZ bond fund # 1, and buy ABC bond fund # 2, which are very similar, and captures a loss even when there is really a positive net return.

The use of harvesting losses can offset a capital gain whether realized in the year it was captured, or a future capital gain. There is no disadvantage to harvesting losses, because they can be carried forward for future years without expiration. This should be done at every opportunity that will not trigger excessive trading fees.

In a real life example, in late 2007 we dealt with a client who invested $1,000,000.00 just before the market began to decline precipitating the financial crisis. Through proper tax loss harvesting, the client was able to harvest more than $300,000.00 in tax loss carry forwards. By late 2010, the client had a portfolio that had more than fully recovered back his original value if $1,000,000.00, plus some nominal small gains. The following year, he was able to sell a rental property that he and his wife had for many years been attempting to sell, which generated a taxable gain of $250,000.00. As a result of the proper active ongoing approach to tax loss harvesting, and a disciplined commitment to long term investing, the client realized a tax liability of ZERO, while maintaining their investment allocation for longer term growth.

In the words of Robert Kiyosaki, “It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.”

Filed under: Articles

Comments: Comments Off on Tax Loss Harvesting – How To Limit Your Tax Liability

Market valuation metrics are important in setting expectations for returns and for providing us a guide for where we have been. Valuation metrics attempt to quantify (basically assign a number we can use for comparisons) how over or under valued a market might be. Let’s start by discussing these points:

The stock market is considered a leading indicator.

An overvalued market can become more overvalued.

An overvalued market can grow its way to fair value.

An overvalue market can have a correction.

We will then discuss our current market valuation metrics.

Stock Market is Leading Indicator

The stock market is one of the better leading indicators for the economy. According to Conference-board.org

The ten components of The Conference Board Leading Economic Index® for the U.S. include:

Average weekly hours, manufacturing

Average weekly initial claims for unemployment insurance

Manufacturers’ new orders, consumer goods and materials

ISM® Index of New Orders

Manufacturers’ new orders, nondefense capital goods excluding aircraft orders

Building permits, new private housing units

Stock prices, 500 common stocks

Leading Credit Index™

Interest rate spread, 10-year Treasury bonds less federal funds

Average consumer expectations for business conditions

As you can see, the stock prices for 500 common stocks provide us more information about the economy. Therefore, there are times the stock market is overvalued and that is an indicator the economy may accelerate (and justify the higher valuation).

Stock Market Can Become More Overvalued

Just because the stock market is slightly overvalued does not meant that it cannot become more overvalued. Further, if an investor says the market is overvalued and goes to cash, the market can continue to go up. If the market continues to go up, it would not be unusual for the underlying fundamentals to improve. When the “overvalued” market corrects, it may not drop down to the value the investor went to cash at because the fundamental underlying improved from that moment in time.

It’s difficult to explain but let’s say the price of a stock is 20 and earnings are 1. That is a 20 P/E. Let’s say a 15 P/E is fairly valued so the price should in theory should be 15. An investor then “sells high” because he thinks it should only be worth $15 because a 15 P/E is the fair value. The price doubles to 40 and the earnings go to 1.75. The stock has become even more overvalued at a 26 P/E. The investor stays in cash due to the stock becoming even more overvalued. Now let’s say the stock corrects and price drops to $25 and the earnings stay at 1.75. The investor see value in the P/E being 14.29 and buys the stock again. So he sold at an overvalued 20 P/E and bought it back at a 14.29 P/E, he had to make money correct? Not exactly, he sold at $20 and bought it back at $25. He is $5 worse off.

The moral of the story, you can lose money by “selling” an overvalued market and waiting for it to become a “better deal”.

An Overvalue Market Can Grow Its Way to Fairly Value

We will again use the P/E ratio and let’s remember the stock market is a leading indicator. If we have an overvalued market, prices can grow less than earning and end up fairly valued. Let’s take the stock in the previous example. If we buy it for $20 when the earning are $1 dollar, we have a 20 P/E. If the price goes to $25 and earnings grow at a faster rate to 1.75, we now have a fairly value stock with a 14.29 P/E.

An Overvalued Market Can Have a Correction

This last point is the one everyone fears and why they might sell when they think the market is overvalued. The perfect example is the dot com bubble. Valuations were at historically rich values and the market corrected by dropping prices. The danger with this reason is that it’s very difficult to know when it will predict a correction in price.

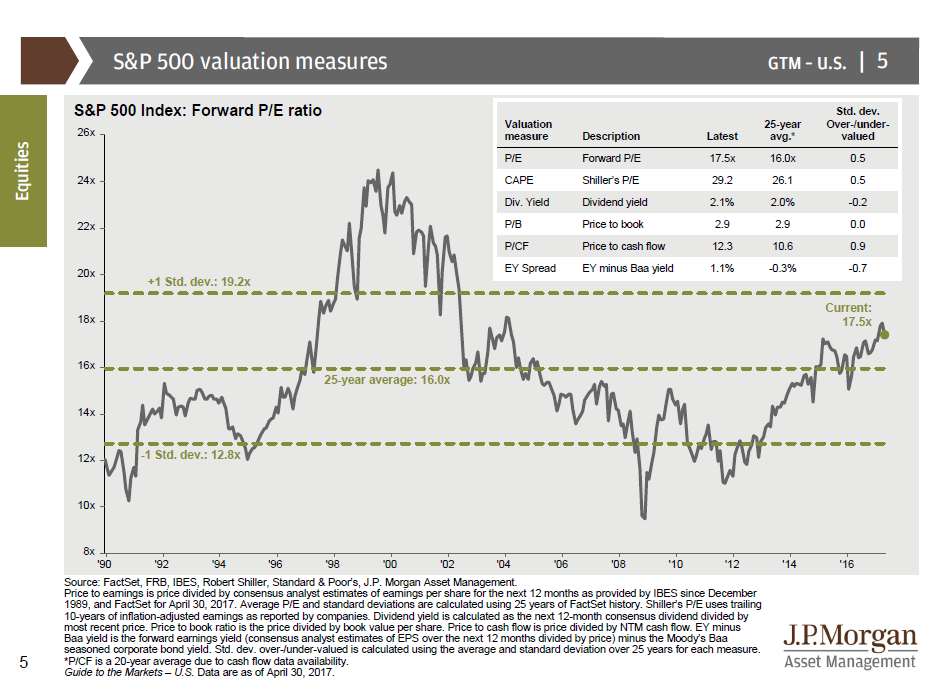

We have a variety of valuation metrics based on the S&P 500. The third column is “Std Dev.”. We

expect the value to be between 1 and -1, 66% of the time.

Metrics Signaling Over-Valued

P/E – This measure is simply the price of the S&P500 divided by the projected earnings. Currently, this measure says the market is slightly overvalued as a 0.5

CAPE – This measure is the cyclically adjusted P/E or Shiller’s P/E. This measure takes the average of the past 10 years of earnings. Currently, it also indicates the market may be slightly overvalued at 0.5

P/CF – Price to Cash Flow metric is the price divided by the cash flow of the company. The metric is currently at 0.9 which signifies an overvalued market

Fair Value

P/B – The price of the stock dividend by the “book value” or the value of the stock held on the

accounting books of the company based on historical accounting data. Currently, its standard deviation

is 0.0 indicating Fair Value.

Metrics Indicating Undervalued

Dividend Yield – This measure is the dividend of the stock divided by the price. At a -.02, the dividend

yield is indicating a slightly undervalued market.

EY Spread – This measure takes the earnings yield of stocks minus the yield on Baa corporate bonds.

The current standard deviation of -0.7 indicated an undervalued market.

The Take Away

So we reviewed how even an overvalued market can become fairly valued a variety of ways and we also reviewed what our current metrics are telling us about the S&P500. The next question is, “Is the market fairly valued”? With the current metrics, you can make an argument for overvalued, fairly valued, and undervalued. My opinion? I do not feel the current metrics are strong enough to form a strong enough opinion worth acting on. Given the wealth of information out there and how implementing what might sound like a great strategy on what you read in Baron’s magazine or hear don CNBC, its important to partner up with an expert like Brian Cohen at Landmark Wealth Management LLC.

It’s time to improve your 401(k) by ditching your Target Date Fund and utilizing some other lesser known tools in your 401(k).

Everyone is familiar with 401(k) and 403(b) plan by now. They have essentially replaced defined-benefit plans in the American retirement landscape. Most people take a set-it and forget it attitude towards these accounts, picking some funds and then ignoring it for years until they either switch jobs or are getting close to retirement. This is the wrong attitude to take with such an important account. This article will show you some things you can do to repair and improve your 401(k), not only through the investment selection but also with some other features that you may not have even heard of.

Target Date Funds – Are they any good?

Target Date Funds have been the go to investment for most 401(k) participants since the early 2000’s. This is mostly because they are the default investment option for most retirement plans. Basically, you are automatically invested in them unless you say otherwise. The concept is that your portfolio will automatically adjust over time as you grow closer to retirement – shifting from stocks to bonds. They simplify investing down to one single criteria, your age. They theory being that you are more conservative as you get older therefore bonds, typically thought of as a more conservative investment, are a more appropriate asset for your portfolio. In general, this theory holds true but there are so many other variables to consider besides your age that in real life, the Target Date fund allocation is rarely the “best” allocation for you.

Besides your age, you should be considering your risk profile, cash flow needs, income/expenses, current net worth, and other financial goals. Tweaking any one of these could lead to a very different recommended portfolio. If the Target Date Fund gets your allocation wrong you are either taking on more risk than you should be or leaving money on the table. For example, someone who is one year out from retirement may have a portfolio that is nearly all bonds if using a Target Date Fund. In reality, this soon-to-be retiree may greatly benefit from a higher allocation to stocks, improving their overall financial position and may be very well be comfortable taking on the additional risk.

As well, the amount and type of bonds held within the target date portfolio can vary dramatically from one fund to the next even though they are “targeting” the same investment year. As an example, I’ll compare two well-known fund manager’s 2030 Target Date Funds. First, the Vanguard 2030 Target Retirement Fund (VTHRX). This fund has a 27% allocation to bonds at the time of this article’s writing (remember the allocation changes over time). And of that allocation the bonds have a “Medium” quality rating and a “Medium” Interest Rate Sensitivity Rating according to Morningstar and seen in the below style box. They take a moderate amount of risk.

The T. Rowe Price 2030 Retirement Fund (TRRCX) has only a 21% allocation to bonds and a low-quality bond rating and Medium Interest Rate Sensitivity. So not only is there less bonds but the bonds they hold take more risk than the Vanguard fund. Remember these two funds are targeting the exact same retirement year so in theory have the same goals. It just looks like they go about it in a different way. Which strategy and allocation is right for you?

For all their faults Target Date Funds are not all bad. Prior to the advent of Target Date Funds, many 401(k) plans had cash (or cash equivalent) as the default investment selection. This would lead many participants to dramatically underperform the markets overtime, hindering their chance at a successful retirement and requiring many more working years before quitting your job. The overall message is these funds are good but you can do better. See: Target Date Mutual Funds – Is it really that Easy?

To Roth or Not to Roth

Most 401(k)’s now have an option to contribute with after-tax dollars to what is called a Roth IRA. It combines the higher limits of a 401(k) with the after-tax deferral of a Roth IRA. The question is how do you choose between the Roth or Traditional 401(k)? There aren’t any clear cut answers but the decision comes down to your current tax situation and your expected future tax situation. If you are in a lower tax bracket now you might want to consider the Roth 401(k) as the value of the tax deduction from a Traditional 401(k) would be less. Then in the future, if you are in a higher tax bracket you can get your money out tax free. If on the other hand, you are in a high tax bracket now a Traditional 401(k) might be a better choice as you will receive a tax deduction at this higher rate. Then in retirement when your tax rate is lower you will be able to get the money out at a favorable tax rate. It is actually a good idea to have both a Roth Assets and a Pre-Tax Assets. This will allow you to be flexible about when and which account you draw money from. During retirement your tax brackets often fluctuate so using a dynamic approach to drawing retirement funds could save you a lot in taxes. This might mean contributing to a Roth 401(k) early in your career when you income is lower and then switching to pre-tax contributions as your income pushes you into higher tax brackets.

Some companies even allow their employees to make additional “after-tax” (not specifically Roth) contributions, up to $35k, to a 401(k). This means you can contribute a maximum of $53k to your 401(k) in any given year ($59k if over age 50). This allows you to essentially make “Super-Roth” contributions since the after-tax portion can be rolled over to a Roth IRA in the Future. See: Tools of the Rich and Why to Avoid Them.

Turn on Automatic Increases

If you’re not maximizing your 401(k) contributions yet there is a painless way to ensure you get there quickly. Many plans allow the option to set up an automatic increase in your salary deferral. Basically if you are currently contributing 10% of your salary you can set it up so that after one year it goes up to 12%, and then the next year 14%, until you get to the $18,000 maximum for 2017. By setting it up ahead of time the increases will go through without you even knowing it happened.

Think your Falling Behind Utilize the Catch-up Contribution

If you’ve just turned 50 and you still don’t think you have enough saved for retirement, the IRS allows for a catchup contribution to help fill that gap. In 2017, you can contribute an extra $6,000 to your 401(k) and it can be either pre-tax or after-tax dollars. If you are eligible, you can also add another $1,500 per year to your IRA or Roth IRA. This increases your total 401(k) contribution to $24,000 and $59,000 if making after-tax “Super Roth” contributions. This should help you fill in any leftover gaps in your retirement before it comes time to actually quit your job.

The big idea is to not just ignore your 401(k). With defined-benefit pensions becoming a thing of the past, it’s one of the most powerful tools you have in achieving a successful retirement. Some of the features mentioned above have not been around to that long so take a little time and review your employer plan.

About The Author

Phillip Christenson, CFA, is the co-owner of Phillip James Financial, an independent Fee-Only Financial Planning company located in Plymouth, MN. He helps individuals and families with wealth management, investments, tax planning, and tax preparation. He also writes on his own personal blog, here, about the markets, investments, and personal finance.

Filed under: Guest Articles

Comments: Comments Off on Let’s Fix your 401k

I rarely write opinion pieces. I’m not sure why to be honest, but I prefer to stick to facts, figures, and strategies. Opinion pieces are far more grey, rather than clear cut “dollars and cents” type stuff.

Last month the Department of Labor Fiduciary Rule was supposed to go into effect. I’m both infuriated and ecstatic all at the same time. I suppose I’m somewhat bipolar when it comes to the new fiduciary rule.

Why so emotional? The rule is great for investors, bad for brokers, and neutral to negative forc current fiduciaries. It’s a hot bed of “what ifs” and “what could be” when it comes to how financial advisors interact and guide their clients.

What Is A Fiduciary

The term “fiduciary” is at the heart of the matter. Just what is a “fiduciary”?

A fiduciary is someone who holds a special responsibility to act only in the best interests of someone else. Above all else, a fiduciary must put the best interests of the person receiving the advice, guidance, or services first and foremost no matter what!

Your doctor is a fiduciary. They must put your interests above their own. Your attorney and your accountant also hold a fiduciary responsibility. They must always act in your best interests regardless of their own personal financial gain or loss.

For example, your doctor must take action to ensure your health is their primary goal. This means they can’t recommend a procedure or prescription unless they can honestly say it’s the right thing for you. Even if one procedure or prescription pays them more money, they must do what’s right for you at all times.

The same goes with your attorney. They have an obligation to act in your best interests at all times. Your accountant is no different. They must provide advice and guidance which is ultimately in your personal best interests.

The underlying – and unwavering – theme here, is a fiduciary must do what’s right for you regardless of any compensation, perks, or benefits they receive. If investment product B is better than investment product A, but pays the advisor less, they must recommend the use investment product B.

If you’re unfamiliar with the concept of a “fiduciary advisor”, I bet this all comes as a shock to you! You’ve likely always assumed your investment advisor (or financial planner or whatever you want to call them) was providing guidance solely in your best interests. Unfortunately, this couldn’t be farther from the truth.

The reason this is such a hot button topic, is most financial advisors are held only to a “suitability standard”. What exactly is a “suitability standard”? It’s not much actually.

As industry pioneer Michael Kitces says (my own paraphrasing) “When you go buy a suit, the salesman will sell you one that fits. That’s a suitability standard. The fiduciary standard would prompt the salesman to make sure it looks good on you too!”

Do you want your suit to look good? Or just fit?

Until now, the financial industry has been held solely to a suitability standard. Any financial advisor or investment

manager must have reason to believe an investment or insurance product is simply “suitable”. They have no responsibility to make sure it’s the best solution for you.

In other words, the investment product must generally be a fit. It doesn’t have to be the best fit however.

This allows brokers and financial advisors to sell you products which may be OK, but pay them a lot more money than investments which may be best for your situation.

The scary part about the suitability standard, is anything can be “suitable” if it’s spun right. Any

reasonably intelligent broker or advisor can make a case for whatever product they’re hocking at

any moment in time.

The bar is set too low!

All financial advisors are currently held at a minimum to a “suitability standard”. The “fiduciary standard” is not a requirement (currently).

A pure fiduciary standard is simply something that elite advisors (like my friend Brian at Landmark Wealth Management) have embraced as “the right way to help clients succeed”.

But America’s retirement crisis overwhelming. People have to work longer, harder, and then retire with less.

You can double that for couples. The average couple would get about $2,600 a month then, which is more than half of most retirees income.

For 21% of married couples (and 43% of singles), Social Security payments make up over 90% of their income. The numbers are staggering, and scary.

No matter where your politics lie, the Obama Administration recognized this, and in my opinion was the first Presidency to do anything about the financial industry’s apathy towards investor success.

Enter The Fiduciary Rule

Let me start by explaining what the fiduciary rule is. Under the direction of the Obama Administration, the Department of Labor set out to provide parameters within which financial advisors could provide financial advice.

Why did they target advisors? Frankly, it’s our business to help people plan and prepare for a successful retirement. We hold an important power over the relative financial success our clients enjoy.

The problem is some financial advisors (brokers) are getting rich off other peoples struggles!

The biggest issue is the fees charged to investors. It’s far too common to see fees of 2% to 4% per year and more!

Many of those retirement account investments pay brokerage commissions of 3% to 10% as well. Those commissions aren’t free, they come out of your pocket somehow. The broker get’s rich, while you pay the price!

So the Fiduciary Rule was crafted to reduce the amount of excessive commission and outrageous fee products. Why? Because how a financial advisor gets paid directly leads to conflicts of interest and directly impacts your bottom line (negatively).

If they can recommend product A which pays them a 7% commission, or product B which pays them 1% per year, they may likely opt for the 10% commission EVEN if product B is more appropriate and better performing. That’s a major conflict of interest!

So the DOL Fiduciary Rule was drafted to remove those conflicts of interest. If the financial advisor still wants to use an investment product which may not be the most appropriate, it must comply with the BICE carvout.

What is BICE?

BICE is the “Best Interests Contract Exemption. The DOL views any financial advisor as giving advice for a fee as a fiduciary. If the financial advisor’s compensation is derived at all from commissions, they’re engaging in a prohibited transaction.

Essentially, all retirement accounts (IRA’s 401k’s etc.) must be on a fee arrangement, NOT a commission arrangement. If they’re on a commission arrangement at all, they must follow certain requirements.

First, the advisor must have a contract with the investor. That contract must acknowledge their fiduciary responsibility. This opens the financial advisor – and their employer – to a greater level of litigation.

This is the main reason brokers and their firms hate the DOL Fiduciary Rule. It’s highly likely they’ll get sued much more often than prior. It also means they’ll earn less, while you keep more!

Second, the financial advisor must be able to articulate why a certain product is the best alternative for the investor. Most importantly, the financial advisor must document the various options for the client, and note why their option is the best solution and in the best interests of the investor.

This means when a client leaves an employer, the advisor must be able to clearly articulate why rolling that plan over to an IRA is the best solution.

The Fiduciary Rule Is Watered Down

Simply to get this rule to pass, it had to be so watered down it nearly becomes worthless. First, the rule ONLY applies to retirement accounts. This means your IRA’s and 401k plans etc. fall under the fiduciary rule.

Your regular brokerage accounts, investment accounts, insurance policies, etc. do not fall under the rule. It’s “business as usual” for those investors, and those parts of an investors portfolio.

The BICE exemption is another hang up. It allows for some creativity in explaining why product A is better than product B. It’s a good start, but again, any financial advisor skilled in the art of investment management and financial planning can make a case for one solution over another.

I suspect we’ll see some highly creative arguments as to why an indexed annuity is a better alternative for an investor than leaving the rollover in a 401k plan at lower costs.

Would You Really Want A Financial Advisor FORCED into doing the right thing?

My biggest question for investors is just that. If your financial advisor had to be forced into doing the right thing by you – why would you want to work with them? Wouldn’t you prefer someone like Brian at Landmark or myself (I’m a CEFEX certified fee only fiduciary advisor in Las Vegas)? All NAPFA financial advisors agree in writing to a fiduciary standard as well!

We’ve embraced our fiduciary responsibility for years and years! We weren’t forced into doing the right thing by our clients.

I don’t know about you, but to me the answer is clear. I’d rather have a firm who has always been a fiduciary versus one who was required to change the way they do business because of a new law.

In the end…

Regardless, the DOL fiduciary rule is a good thing. It’s a step in the right direction for investors. It’s certainly no silver bullet, and it appears the Trump Administration is going to delay it and water it down even further. Nonetheless, it’s a good start.

The irony in this is why aren’t financial advisors held to the highest fiduciary standard anyway? Shouldn’t the person who helps you manage, grow, and protect your wealth do what’s right by you first and foremost?

The brokerage world has fought the fiduciary rule for years now. They hate it! They hate it because it’s going to force their financial advisors into doing the right thing:

#1, if your financial advisor is held to a fiduciary standard, their paycheck will likely suffer relative to the commissions they were earning prior.

#2, they’re opening themselves up to a much greater level of liability. Lawsuits will start flying, and next thing you know you’ll see a lot more brokerage world types on tv as defendants in lawsuits.

Find yourself a quality fiduciary financial advisor from the beginning. Find one who wasn’t forced to do the right thing, like my friend Brian! You’ll thank yourself down the road!

About The Author

Greg Phelps, CFP®, CLU®, AIF®, AAMS® is the president of Redrock Wealth Management

in Las Vegas. He’s been in practice 22 years, and has extensive experience

with the brokerage world. He’s also an author, a speaker, and writes for his financial

and investment advice blog RetireWire.

Filed under: Guest Articles

Comments: Comments Off on The Reality Of The DOL Fiduciary Rule

One of the more confusing taxes to grasp for the average American is the gift tax. Despite what many people think, although you can give an unlimited amount of assets to a charitable organization, you are effectively limited to that which you can gift to your own family and friends. A gift in the eyes of the IRS is considered to be “any transfer either directly or indirectly where full consideration is not received in return”.

When gifting assets to someone other than a charity you have an annual exclusion, which in the year 2017 is $14,000.00 per individual, but not in the aggregate. This means you can give $14,000.00 per year to as many people as you like, as can your spouse. So in the event that your child is getting married, and you and your spouse wish to give them a sizeable wedding gift, you may each gift $14,000.00, for a total of $28,000.00. You may also each gift $14,000.00 to your new in-law for a total theoretical wedding gift of $56,000.00. This limit is a per calendar tax year limit, so a $14,000.00 gift in December would not preclude you from giving another gift in January. Should you actually exceed the $14,000.00 in a calendar year, the amount of excess would mean that you should file IRS form 709 for a gift tax return. There are some exceptions this rule though. Among them are:

Tuition or medical expenses you pay directly to a medical or educational institution for someone.

Gifts to your spouse. (Which are unlimited)

Gifts to a political organization for its use.

Gifts to charities

However, if the gift in excess of the annual limit does not fall under such an exception, that still does not necessarily mean you actually pay a gift tax. Here is where things often get a bit confusing. Each individual has a lifetime exemption in the aggregate of $5,490,000.00 for the tax year 2017. So even with the filing of a gift tax return, there is no actual tax due until you exceed the $5,490,000.00 lifetime cap. In the case of a married couple, this amounts to a total gift tax exemption of $10,980,000.00.

When there is a gift in excess of these amounts, the tax is typically due by the donor. This tax on transfers is essentially determined by what is called a “unified credit”. The unified credit is the amount that either reduces or eliminates the tax owed to the lifetime exemption of $5,490,000.00.

It should also be noted that an outright gift or transfer to a trust in which an unrelated person is the beneficiary that is more than 37.5 years younger than the donor, or to a related person more than one generation younger (such as a grandchild) can be subject to what is called the Generational Skipping Transfer Tax (GSTT). However, in recent years legislative changes have unified the exemption for the GSTT at the same $5,490,000.00 for the tax year 2017.

It should be further noted that many of the exclusions and exemptions are set to be adjusted for inflation in future years, barring any further legislative changes.

Many of these numbers may sound like quite a bit of money. In reality it is a sizeable amount in the way of assets when compared to the average American’s net worth. However in many cases the value of an estate’s assets that might be gifted can be misleading. Perhaps an individual has a family business in which the assets that make up the business may be real estate that is vital to the operation of the business. Yet, the business may produce profits on an annual basis of a substantially smaller dollar value. In such cases, if the assets, or at least a portion thereof, are not properly transferred prior to death, surviving family members could be forced to sell the family business just to pay the taxes due on the estate’s value. There are some deductions and business valuation methods that can be used for closely-held family businesses that aid in mitigating the impact such a situation for tax purposes. However, that is not the only substitute for a proper estate plan.

In other cases a family may have a home of sizeable value while simultaneously having a relatively limited liquid net worth. In such cases this presents an opportunity to re-title property through gifting the title of the home via a trust. This can also serve to protect an individual’s assets within their estate that they would prefer to leave to their family by protecting them from numerous other potential liabilities/creditors. This may be particularly beneficial in areas of health care planning as it removes an asset from the taxable estate should a need for long-term care assistance arise.

The most important thing in the process of evaluating the impact of the gift tax is to essentially maximize the amount allowable for gift-tax purposes without impairing your ability to generate income for yourself during retirement. As a result, real estate, such as your primary residence, which typically does not provide an income, is often one of the more common assets to be gifted into an irrevocable trust. This can also be done with numerous income-producing assets in which the right to any income generated is retained. The benefit of using such an approach can permit an individual or couple to maximize their gift tax exemption as well as protect assets from creditors for multiple generations.

The topic of gifting is an important part of estate planning, which is in general is a very complex one. There can be a number of twists and turns in an individual’s personal estate plan that should encompass the totality of their financial condition, as well as their personal family dynamics. While many of the current exemptions and exclusions are now at thresholds that are much more flexible for the average American taxpayer, it’s always prudent to seek the counsel of an attorney with expertise in this field while working in concert with your financial planner and tax advisor.

Filed under: Articles

Comments: Comments Off on How To Understand The Gift Tax

The bond market is the largest public securities market in the world, and substantially larger than the stock market. When investors allocate assets in their investment portfolios, oftentimes those in higher tax brackets will opt to utilize municipal securities for the added tax benefits.

What are municipal bonds?

A muni bond, like any other bond or fixed income investment is a debt instrument. You as the investor loan your money to the issuer for a stated period of time at a specific interest rate. The single biggest difference with the muni market is the potential for tax free income. A municipal bond is generally issued as a debt instrument offered by a State, City, County or Local Municipality. The assets collected are used to finance things such as schools, highways, bridges, and various other projects that require funding. They may also be financing the general budget of a municipality.

Generally speaking, income derived from a municipal bond is free from Federal income taxes. Should you live in a state or city that assesses an income tax, if the bond was issued by a municipality in the state you reside in for income tax purposes, it will typically be exempt from State/City income tax as well. If you reside in a state that does not levy an income tax, the Federal exemption on the income applies regardless of which state you purchase the issue from.

General Obligation vs Revenue Bonds

Muni bonds break down into two broad categories with many sub-categories. The first of which is the general obligation bond, which is exactly what it states. The issue is not financed by any single project of the municipality. Rather it is funded by the full faith and credit of the municipality and its ability to meet its general obligations.

The revenue bond is a bit different. In general they are subject to the ability of a specific project or a specific agency of that municipality. For example, should you purchase a bond that was designed to cover the financing of a new bridge, and the bridge collapsed, the ability for you to redeem your funds will potentially be in jeopardy, as the tolls are no longer being collected. However under such a circumstance the state or city may still be in excellent fiscal condition with no impairment to its ability to repay its other debt obligations. It is for this reason revenue bonds are typically viewed as carrying more risk, which in turn can carry more of an income to compensate for the added risk.

In the case of municipal bonds, there can be other avenues of added protection that you may want when buying an issue. One such feature is insurance. Unlike the Federal government, a municipality cannot simply create more money when there is a budget shortfall whenever it sees fit to do so. It is certainly not impossible for a local municipality to go bankrupt. While this is a fairly rare occurrence, it has happened. The bond issuer can issue these debt instruments with an added layer of insurance against a default by a private insurer. There are a relatively small number of companies that specialize in this type of insurance.

It should be noted that a bankruptcy in a local municipality does not meet the same definition of an individual bankruptcy and does not usually mean a total loss to the investor. Rather in such instances, the schedule of interest and principal payments may be renegotiated along with the issues duration. Typically a municipality would have to file under the Chapter 9 bankruptcy rules.

Another aspect to consider when buying a muni bond is a sinking fund protection. A sinking fund is a separate pool of dollars that are set aside for the purpose of the municipality to retire its debt. This can provide an added layer of protection against the possibility of default.

There are some added tax concerns that too few investors often realize. In some instances when a revenue bond is purchased, if the bond is issued for certain types of projects that are not considered to be issued for public purposes such as the financing of a new football stadium, the interest may be an added liability in the dreaded Alternative Minimum Tax calculation. When buying the bond, you can inquire about this in advance as to whether or not he bond will be exempted from AMT. Furthermore, tax free income derived from municipal securities is an add back for the purpose of calculating Modified Adjusted Gross Income (MAGI), which may impact various aspects of an income tax return.

Unlike US treasury issues, most muni bonds typically have what is known as a callable feature. This permits the issuer to retire the debt sooner than expected and return to you your principal at specific points in time should the issuer deem it favorable to do so. This can alter your expected return from what you originally anticipated. When buying a muni bond it is important to obtain two separate quotes. One is yield to maturity, which indicates a rate of return should the bond be held the full duration. The other is yield to call, which indicates a potential return if the issue is retired early.

The bond market in general is a large and fairly complex investment arena with many twists and turns. You need to be keenly aware of the potential markups by the broker-dealer, which can be quite significant. In addition, an investor needs to be aware of issues trading with what is known as accrued interest in the secondary market. You should understand whether or not you are buying an issue at a premium or a discount. The municipal market can be a bit more complex in terms of its liquidity risks as well as potential tax implications. In general, the average investor is much more likely best suited to be using active fund managers and/or ETF securities to participate in the fixed income markets. These vehicles provide greater liquidity, as well as potential investment expertise.

In what may be a very challenging environment for interest rate sensitive securities in the future, as well as questionable areas of sound credit, and an active fund manager may be well worth it. The recent crisis related to Puerto Rico bonds is a very good example of how many active managers were able to avert the liability well in advance. Municipals, like most fixed income instruments are subject to both interest rate and credit risk. While interest rates remain close to record lows, it is still important to diversify portfolio holdings and lower the correlation of assets you own to ensure they are not always moving in perfect tandem. Fixed income investing is still an important component to achieving this outcome. Ultimately, one’s tax status will determine the benefits of using tax free municipal securities. As such, it is typically prudent your consult your tax advisor, as well as your financial advisor.

Filed under: Articles

Comments: Comments Off on How To Understand Municipal Securities

In recent years we have seen unprecedented actions by global central banks to influence economic events and create monetary stimulus. Here in the Unites States, the Federal Reserve has held interest rates well below historical norms through both conventional and unconventional methods. There can be a number of unintended consequences with any actions that distort markets.

One such consequence is those living on fixed income or positioning a portion of their investments in fixed-income assets are receiving significantly lower yields on their invested assets. Many investors are left searching for different solutions to offset this lack of cash flow, and are often pushed into asset classes which are more aggressive and risky than something they might ordinarily purchase. As of May 2016, the 10-year US Treasury continues to hover in a trading range below 2%. This has created some opportunities in the market for floating-rate securities in recent years.

Floating Rate Notes are secured bank loans made to non-investment grade companies. Ordinarily, anything below investment grade would simply be characterized as “High Yield Bonds, Junk Debt or Junk Bonds”. Yet, there are some significant differences between traditional High Yield Bonds vs Floating-Rate Notes. High Yield Bonds can serve as a hedge against a rising interest rate environment, as they tend to move with the stock market and look more attractive in a strengthening economic environment. When rates are falling, High Yield tends to decline, as their anticipated default risk rises in a weakening economic environment. While this tends to be somewhat true with Floating Rate Notes, they are quite a bit different in terms of risk. With Floating Rate Notes, banks loan money to these below investment grade companies…but secure the loan with collateral in the company. They are issued as senior debt in the capital structure. That means in the event of a restructuring, the holder of these notes would be paid off first as they take priority over other debt holders.

A typical High Yield bond is issued with a maturity of 10 years, whereas the average maturity of a Floating Rate Note at issuance is five to seven years. Since the Floating Rate Notes are callable, they have an actual average maturity of less than three years. This is because the payment is usually compromised of some amortization and required payments from the borrower’s excess cash flow. In the current interest rate environment the shorter maturities may look attractive to a number of investors who are concerned about the negative impact on fixed-income from rising rates, should that ever occur.

Floating Rate Notes are also “Floating” as implied in the name. This means that as rates rise, the issue itself begins to pay a higher interest payment, unlike a traditional High Yield Bond which is issued with a fixed rate. The reason for this is that they are bank loans. They are offered with a spread over the London Interbank Offered Rate, also known as LIBOR. So as rates rise…the LIBOR plus the spread increasing…this will increase the rate of payment. This offers an investor an additional hedge against rising rates.

Ultimately, Floating Rate Bank Notes are the only fixed income asset class that has virtually no direct interest rate risk. This is actually a negative when rates are decreasing because the capital appreciation that traditional investment grade bonds would realize is not available. Yet with interest rates at historical lows, it’s hard to argue that the investment-grade bond market offers a great deal of room for market appreciation. That does not mean that in the short term the ten-year US Treasury won’t potentially see 1%, or maybe lower. Rising rates have been predicted incorrectly for nearly a decade now. However, the longer term trend in rates may in fact be higher, even if that takes several years.

While Floating Rate Notes generally don’t have a direct interest rate risk, this does not mean they are riskless. In reality, there is no such thing as a risk free investment. With Floating Rate Notes, an investor is still buying below investment grade debt. This means that while they are still higher in the capital structure, they are not without default risk. Additionally, they can pose some liquidity risk to investors that resembles what can happen in the High Yield bond market. If you were to look at a trend line in the price volatility of Floating-Rate Notes, you’d find they have been fairly consistent and impervious to rate changes like any other ultra-short duration debt instrument. Yet during the market panic of 2008 their prices declined substantially due to their credit risk in a credit market crisis. This was temporary in nature as much of the market panic and price action was unwarranted, and prices eventually normalized. However, if you as an investor owned them at that point in time, the decline was shocking and rather scary. As such the ultra-short duration on these instruments does not imply that they are a substitute for cash or money-market instruments.

Where they may be advantageous to the average investor is as a hedge against the potential for rising interest rates by supplementing a traditional fixed income allocation. The interest payments tend to be in excess of current investment-grade offerings and so can generate a greater current cash flow. They also offer an investor the opportunity to ease into the High Yield space with less overall volatility.

Bank Loans are technically not securities, so investors cannot purchase them directly as this is still a private market. However, the average investor can participate in this market through the mutual fund world or through a private portfolio manager who specialized in bank loans. There are a multitude of mutual funds that offer access to this marketplace, yet it is of paramount importance that these issues are used in an appropriate manner. They should not be construed as a sole option for a fixed income allocation for the average investor. Instead, they should be utilized as something that compliments more traditional fixed income holdings.

Filed under: Articles

Comments: Comments Off on Understanding Floating-rate Securities

Whether or not you should convert to a ROTH IRA, like most financial questions is dependent on the circumstance. First it’s important to distinguish between a contribution and a conversion.

A contribution to a ROTH is a not tax-deductible addition from a savings source that is not part of a current retirement plan. This is non-deductible because the gains on the ROTH IRA are income tax free at distribution, whereas a traditional IRA contribution may be deductible against your current adjusted gross income, and yet taxed upon withdrawal.

When examining a conversion to a ROTH, you are considering the possibility of taking an existing retirement account (IRA/401k etc) and paying the taxes on all or some of the funds in order to convert to a now tax-free ROTH account.

The contribution to a ROTH is limited based on your adjusted gross income. The phasing out of eligibility based on income differs from single filers to married couples. However a conversion to a ROTH no longer has an income limitation associated with eligibility. If you are willing to pay the taxes on dollars that are currently tax-sheltered, there are no restrictions on the dollar amount of the conversion. It should be noted that while there are caps on ROTH IRA contributions, that is not the case with ROTH 401k’s sponsored via an employer plan.

The answer as to whether or not to convert to a ROTH is often, “No,” but that is not always the case.

The reason it is not always prudent is the effect of the withdrawal of your assets up front to meet the current tax liability must be weighed against the tax free benefit. For example…let’s assume that you are age 50 and have $200,000 in a traditional IRA. Converting the lump sum amount would likely move you into a relatively high tax bracket when adding in any other income sources. If you assume a 28% hypothetical rate after deductions, the calculation would look something like this:

A traditional IRA earning an average return of 8% would have compounded to approximately $634,433.00 by age 65.

The ROTH IRA conversion would cost you at 28%, a tax liability of $56,000.00

The remaining investable assets of $144,000 are then compounded at the same 8% rate equaling approximately $456,792.00 by age 65.

The lost 56k has a future value at the same rate of return of $177,641. This is worth a difference of about $7,000.00 per year in pre-tax income for a 65 year old retiree who uses a 4% spending strategy. This is exactly at the point in which you may now need the income…potentially in a lower tax bracket in retirement, thus negating much of the tax-free benefits.

If you were at a lower tax rate in retirement, say 15%, and used a 4% withdrawal rate at age 65. The results from an income perspective are as follows:

The $634,433 would generate $25,377 annually. After tax, you would net $21,570 per year.

The ROTH IRA which would have compounded to $456,792. Using the same 4% withdrawal rate, you would net tax free income of $18,271.

Some might look at these projections and assume that they will pay the taxes from another source, which is advisable should you choose to convert. However you are still depleting a sizeable amount of working investment capital from somewhere up front.

Does this mean we should never convert to a ROTH? No. It does not.

In many cases an individual may have substantial resources to secure their income in retirement, and not need the ROTH IRA for income after converting. In such cases, the asset may simply be inherited by beneficiaries who themselves may be in a higher tax bracket when they receive the income. Additionally, the conversion to the ROTH eliminates the need to take required minimum distributions, thus compounding the tax-free shelter for those who are not in need of income for a much longer period.

In some cases, it may make perfect sense. One clear-cut example would be circumstances in which you have a traditional 401k plan with an after-tax portion that is segregated. There are still a number of retirees, or soon to be retirees that have retirement plans that were established prior to 1987. Many of these participants have a portion of their plan that was contributed to on an after-tax basis. When doing a rollover of your plan after leaving your employer, you can convert the after tax portion directly to a ROTH with ZERO income tax liability since it was already taxed. However, if you roll the entire plan into a traditional IRA and comingle the funds, you will not be able to do this in the future. It is generally not a good idea to comingle pre-tax and after tax dollars regardless of the intent to convert to a ROTH IRA. However, the conversion in that scenario is a fairly simple determination.

Another common scenario is that of those on tax-free disability pensions. If you are a retired police officer or firefighter who was hurt in the line of duty, you are likely receiving a disability pension that is tax free. If that is the case you may have more tax deductions from things like mortgage interest and property taxes than you have in taxable income. Perhaps the combined deductions are equal to a hypothetical $20,000. Remember that you are not required to convert the entire balance at once. Partial conversions of cash or securities can be processed each year. That means in this scenario you have at least a 20k cushion to convert each year with once again a ZERO tax liability. After several years you may find that you’ve converted the entire balance to a tax free account.

There are several other possible scenarios where this type of a conversion makes sense. One is a young person whom is in an extremely low tax rate and will pay no taxes anyway because their account balance is too small and will not generate much taxable income upon conversion.

Generally in cases where it makes sense to convert to a ROTH, it rarely makes sense to convert a sizeable balance at one time. It is usually a good idea to work with your CPA and financial planner towards the end of the year to run a mock tax return and get a better idea of just how much can be converted without creating a substantial tax liability. If this is not done carefully you can trigger numerous problems. Among them is potentially triggering an Alternative Minimum Tax (AMT) liability from the increased income.

In general, an important consideration is when you will need the funds. If you’re assuming the tax liability up front and you are willing to do that, you should make sure that you will not need the proceeds anytime soon. Because of the amount of tax liability you may incur, it tends to make more sense when you can justify growing the funds for a longer period of time. Clients who have no real need for their IRA have a stronger argument for a conversion. Most importantly, you need to address this on a year-by-year basis. You may be in a position that a conversion makes sense this year, but next year your tax status changes and it is no longer advisable. Don’t rush to convert solely on the basis of assumed higher tax rates in the future. Many feel rates will go up, and may be correct. But the tax code is complex and may not necessarily be higher for you. It may also increase and be yet again reduced. There are not many absolutes in financial planning. Each circumstance must be evaluated on its own merits.

Filed under: Articles

Comments: Comments Off on Should I Convert To A ROTH IRA?

One of the most important issues for small, closely held businesses is that of business continuity. This can be a concern in the face of a variety of obstacles. One of the most important areas of concern is related to a business interruption in the face of a partnership. Creating a new business entity with a partner, or even acquiring a partner within and existing business, can come with a host of challenges. One of the first areas of concern should be addressing a proper buy-sell agreement.

Imagine owning a partnership interest with a colleague who passes away. While the two of you may have worked well together, his/her portion of the business interest ownership is likely to pass to his surviving family members, depending on the terms of his estate plan. Yet, is it prudent to now take on their spouse or children as your new partner? More often than not if they haven’t been actively participating in the daily operations of the business, they’re not qualified to work with you on a daily basis. They will likely become an economic liability to you…the surviving owner who is now responsible for the day-to-day operations without the same assistance.

A buy-sell agreement is a legal contract between partners which specifies the terms under which one partner, or their inheriting family members, would be essentially bought out of an ownership interest. These agreements are commonly funded with life insurance policies held by each partner on the life of the other. The terms of the agreement dictate the amount of coverage that needs to be in force to properly reimburse the surviving inheriting family members for the appropriate business valuation.

There are several potential triggering events that can cause a buy-sell agreement to activate either a mandatory or optional buyout of a business partner. One obvious example of such an event is the death of a partner. Another such event could be a newly incurred disability of a partner. Should the partner be unable to perform the daily functions of their business operations, they may have a personal disability policy for themselves. While that may suffice to help reimburse them for their daily living expenses, it does little for you, the alternate partner, who must now assume the greater responsibility. Holding a disability policy on your partner can be a method to fund a buyout of the disabled partner’s equity.

There are also other possible triggering events that are not as easily addressed. In some cases a partner may be forced into the unfortunate circumstance of a divorce. In such cases, you as a business partner are often be invariably drawn into the equation. The divorcing spouse of your partner may want to continue to maintain their ownership interest in the business entity even though they had little to nothing to do with its daily operations. While this cannot be addressed by funding the agreement with a life insurance policy, it is important to have such terms and the corresponding triggering events addressed in the initial buy-sell agreement.

Retirement is also a potential triggering event that should be addressed. In many cases two partners may have a substantial difference in age, or simply differing opinions on when they might like to retire. The terms of such a decision should also be carefully spelled out within the buy-sell agreement. Planning to address these issues in advance is imperative, as it allows for the proper funding of such an event ahead of time.

In some cases there may be multiple partners which can further complicate things. This is typically addressed by what is called a cross-purchase agreement. This is fundamentally the same principle, but addresses the terms of each partner, as well as how the proper insurance is funded.

A very important component in all of these agreements is setting a proper business valuation. In some cases this is a specific fixed dollar value, and in some cases it is a formula to determine proper valuation. Some agreements may use either the book value method, discounted cash flow method, sales multiple valuation or capitalization of earnings method. What’s important is that these buy-sell agreements be addressed and updated from time to time if necessary. While the terms may have been acceptable based on the methodology at the time, the insurance coverage over time may no longer be sufficient to cover the deceased owner’s current equity. As the business grows in economic value, the amount of corresponding insurance may need to increase. This often makes term insurance policies difficult to use as a mechanism to fund such agreements, as they require increasing amounts of insurance to be met with updated medical examinations.

A proper succession plan is often a complicated matter, and depends on a number of factors that are specific to the dynamic of the specific business, its partners and their individual roles within the organization. This is an important component of a properly structured estate plan for the small business owner who is involved in a partnership. It is always advisable that business partners sit down together with an attorney who has expertise in the area of business succession planning to decide collective objectives, and articulate them in a binding contract that meets the needs of all those involved in a fair and equitable manner.

Filed under: Articles

Comments: Comments Off on Buy-Sell Agreements: The Basics